The Fractured Link: How the Fed's Rate Cuts Fail to Anchor Mortgage Rates—and What Investors Should Do About It

The Federal Reserve's monetary policy has long been a cornerstone of economic stability, yet its influence on mortgage rates is unraveling in ways that defy conventional wisdom. In 2025, as the Fed signals a cautious path of rate cuts, mortgage rates remain stubbornly high, hovering near 6.5%. This decoupling—between the Fed's short-term policy levers and the long-term borrowing costs that shape housing markets—exposes a critical flaw in the transmission mechanism of monetary policy. For investors, this breakdown demands a reevaluation of traditional correlations and a shift toward defensive strategies in real estate and fixed income.

The Transmission Mechanism in Crisis

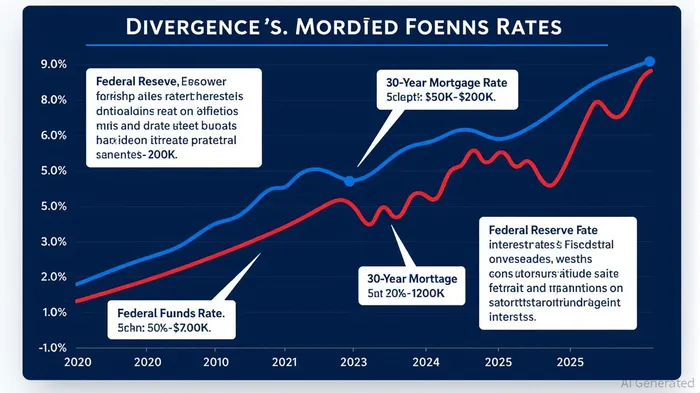

The Fed's benchmark rate, the federal funds rate, is designed to influence broader financial conditions. Historically, lower rates have spurred economic activity by reducing borrowing costs for consumers and businesses. However, mortgage rates, which are determined by the 10-year Treasury yield and market expectations of inflation, have diverged sharply from this logic.

Consider the data: in the first half of 2025, the Fed's target rate remained in a 4.25–4.50% range, while the 30-year mortgage rate averaged 6.84%. This gap reflects the dominance of bond market dynamics over central bank policy. The 10-year Treasury yield, which stood at 4.29% in June 2025, is shaped by a cocktail of factors—economic growth forecasts, inflation expectations, and fiscal policy risks—none of which are directly controlled by the Fed. When the Trump administration's tariff policies or geopolitical tensions threaten to reignite inflation, bond investors demand higher yields, pushing mortgage rates upward even as the Fed cuts rates.

This disconnection is not new. In 2024, a 50-basis-point rate cut by the Fed coincided with a surge in Treasury yields, as bond markets concluded the economy was stronger than the Fed feared. The lesson is clear: the bond market, not the Fed, now sets the tone for long-term rates.

Why Traditional Correlations No Longer Hold

The breakdown of the transmission mechanism stems from three structural shifts:

1. Inflation Anchors Eroding: Inflation expectations, once tightly anchored by the Fed's credibility, have become more volatile. Tariff-driven supply shocks and global energy markets now play a larger role in shaping inflation than domestic monetary policy.

2. Bond Market Dominance: The 10-year Treasury yield, a proxy for long-term risk-free returns, has become a more potent driver of mortgage rates than the Fed's short-term rate. This is because mortgage rates are inherently forward-looking, reflecting investors' views of future economic conditions.

3. Policy Uncertainty: The Fed's dual mandate—price stability and maximum employment—has created ambiguity in its policy path. When markets doubt the Fed's ability to balance these goals, they price in higher risk premiums, further decoupling mortgage rates from policy rates.

Defensive Strategies for a Fractured Market

Investors must now navigate a world where traditional correlations—such as the inverse relationship between Fed rate cuts and mortgage rates—no longer provide reliable guidance. Here are three actionable strategies:

1. Invest in Investment-Grade Commercial Mortgage Loans (IG CMLs)

Private commercial mortgage loans secured by cash-flowing real estate offer a compelling alternative to traditional fixed income. These loans, with loan-to-value ratios of 65% or less and amortization schedules of 5–20 years, provide structural advantages. They are senior in the capital stack, reducing default risk, and often include prepayment penalties that protect against refinancing risk.

Historically, IG CMLs have outperformed corporate bonds and CMBS in both total returns and risk-adjusted performance. From 2008 to 2022, their average realized loss was just 3 basis points, compared to 10 bps for corporate bonds. In a high-rate environment, these loans offer yields of 5–7%, with lower volatility than high-yield debt.

2. Hedge with Mortgage REITs (mREITs)

Mortgage REITs, particularly those focused on commercial real estate, can generate income while benefiting from rate normalization. For example, Blackstone Mortgage TrustBXMT-- (BXMT) demonstrated a 57.14% post-earnings resilience rate from 2022 to 2025, outperforming broader equity markets. mREITs leverage interest rate swaps and other hedging tools to mitigate refinancing risk, making them well-suited for a Fed easing cycle.

However, investors should prioritize mREITs with strong balance sheets and diversified portfolios. Commercial mREITs with exposure to multifamily and industrial properties—sectors with resilient demand—are particularly attractive.

3. Diversify Fixed Income with Inflation-Linked Bonds and Defensive Currencies

Traditional sovereign bonds now offer near-zero or negative yields, making them poor hedges. Instead, investors should consider long-duration inflation-linked bonds, which adjust for inflation and offer no effective lower bound on real yields. Defensive currencies like the U.S. dollar, Japanese yen, and Swiss franc also provide stability in volatile markets.

The Path Forward

The decoupling of Fed rate cuts and mortgage rates is not a temporary anomaly but a symptom of deeper structural shifts in global capital markets. Investors who cling to outdated correlations risk being blindsided by market volatility. By adopting defensive strategies in real estate and fixed income—leveraging the resilience of IG CMLs, the income potential of mREITs, and the flexibility of inflation-linked bonds—investors can navigate this fractured landscape with greater confidence.

The key takeaway is clear: in an era of policy uncertainty and bond market dominance, diversification and active management are no longer optional—they are imperative.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet