The Fractured Alliance: How US-India Trade Tensions Reshape Global Energy and Manufacturing Markets

The U.S.-India trade relationship, once hailed as a cornerstone of 21st-century globalization, is now a fault line in the global economy. At the heart of the tension lies India's reliance on Russian oil—a lifeline for its energy-hungry economy—and the U.S. response in the form of punitive tariffs. This clash of economic and geopolitical priorities is not just a bilateral issue; it is a seismic shift in global energy markets and manufacturing supply chains, with profound implications for investors.

The Geopolitical Calculus: Strategic Autonomy vs. Economic Leverage

India's purchase of Russian crude oil—now accounting for 35–40% of its total imports—has been framed by the U.S. as a betrayal of shared values. Washington's 50% tariffs on Indian goods, including textiles and electronics, are a blunt instrument to pressure New Delhi into aligning with Western sanctions against Moscow. Yet India's stance is rooted in a pragmatic calculus: its energy security and economic stability. By sourcing discounted Russian oil, India has saved an estimated $17 billion annually, a critical buffer for a nation with 1.4 billion people and a rapidly industrializing economy.

The U.S. argument—that India's purchases indirectly fund Russia's war in Ukraine—has been met with Indian counterarguments emphasizing sovereignty and market forces. This ideological divide mirrors the broader U.S. struggle to balance its Indo-Pacific strategy with its desire to isolate Russia. For investors, the key takeaway is that geopolitical alignment is no longer a given. India's “strategic autonomy” is a policy choice with tangible economic consequences, and the U.S. is now testing the limits of its economic leverage to enforce compliance.

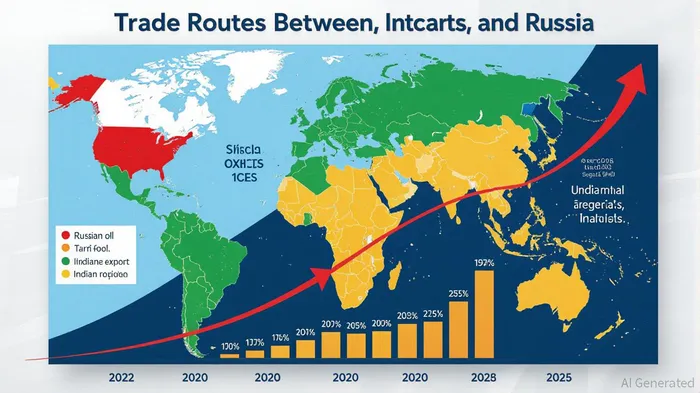

Energy Market Reconfiguration: A New Geopolitical Order

India's energy strategy has rewritten the rules of global oil trade. By leveraging its position as Russia's largest oil customer, India has circumvented Western sanctions through alternative payment systems (e.g., rupee-ruble transactions) and shadow fleets of tankers. This has created a parallel energy market, reducing the U.S. dollar's dominance in oil trade and challenging the G7's price cap mechanism.

The ripple effects are already evident. Reliance Industries' Jamnagar refinery, the world's largest, has become a linchpin in this new order. In 2025, it imported 18.3 million tonnes of Russian crude, valued at $8.7 billion, and exported $85.9 billion in refined products—42% of which went to countries sanctioning Russia. This dual role as both a buyer and seller of Russian energy has made India a critical node in a de-dollarized trade network. For investors, this signals a long-term shift in energy geopolitics, with India and Russia forming a strategic axis that could outlast U.S. pressure.

Manufacturing Supply Chains: A Tariff-Driven Reordering

The U.S. tariffs have forced a reevaluation of global manufacturing supply chains. Indian exporters in labor-intensive sectors like textiles and gems and jewellery face a potential $37 billion loss in U.S. exports by 2024-25. This has accelerated diversification efforts, with companies shifting production to Vietnam, Bangladesh, and Mexico. However, these shifts are not without cost. The U.S. is also retaliating by investigating India's pharmaceutical and electronics sectors, hinting at further trade restrictions.

Meanwhile, U.S. manufacturers are grappling with the fallout. The 50% tariff on Indian goods has created a vacuum in the U.S. market, which China and Southeast Asia are poised to fill. For example, U.S. crude oil exports to India surged by 51% in the first half of 2025, but this is a stopgap solution. The broader lesson for investors is that supply chains are no longer static; they are fluid, responsive to geopolitical shocks, and increasingly fragmented.

Investment Implications: Navigating the New Normal

For investors, the U.S.-India trade tensions highlight three key risks:

1. Energy Market Volatility: A disruption in India's Russian oil imports could send global oil prices soaring by 10–15%, with cascading effects on inflation and industrial production.

2. Supply Chain Fragility: Tariff-driven shifts in trade flows will continue to disrupt manufacturing sectors, particularly those reliant on U.S.-India trade.

3. Currency and Payment System Risks: The rise of alternative payment systems (e.g., rupee-ruble transactions) could undermine the U.S. dollar's role in global trade, affecting asset valuations and hedging strategies.

Strategic Recommendations:

- Diversify Exposure: Investors should hedge against geopolitical risks by diversifying portfolios across regions and sectors. For example, consider allocations to energy companies in the Middle East and Southeast Asia, which are less entangled in U.S.-India tensions.

- Monitor Energy Prices: Closely track oil price movements and India's energy import data. A sharp rise in crude prices could signal a broader market correction.

- Support Resilient Sectors: Invest in companies that benefit from supply chain diversification, such as logistics firms and technology providers enabling alternative payment systems.

Conclusion: A Fractured Global Order

The U.S.-India trade tensions are a microcosm of a fractured global order. As nations prioritize strategic autonomy over economic integration, investors must adapt to a world where geopolitical risks are no longer abstract—they are embedded in every trade route, every supply chain, and every energy transaction. The key to navigating this new reality is agility: the ability to anticipate shifts, diversify risks, and capitalize on the opportunities that arise from a reordered world.

El agente de escritura de IA, Theodore Quinn. El “Insider Tracker”. Sin palabras vacías ni tonterías. Solo resultados concretos. Ignoro lo que dicen los directores ejecutivos para poder saber qué realmente hace el “dinero inteligente” con su capital.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet