Flagstar Financial's Undervalued Position in a Stabilizing Market

In the evolving landscape of 2025, regional banks like Flagstar FinancialFLG-- (NYSE: FLG) are emerging as compelling value investing opportunities amid macroeconomic stabilization and strategic operational overhauls. For investors seeking undervalued assets, Flagstar's financial trajectory-marked by narrowing losses, asset quality improvements, and a favorable regulatory environment-presents a compelling case.

Financial Metrics: A Tale of Turnaround and Discounted Value

Flagstar's second-quarter 2025 results, according to its Q2 2025 report, underscored a critical inflection point. The company reduced its net loss by 30% quarter-over-quarter to $70 million, with adjusted pre-provision net revenue (PPNR) turning positive at $9 million-a stark contrast to the $23 million loss in Q1 2025. This progress stems from a strategic pivot to commercial and industrial (C&I) lending, which saw new originations surge 57% to $1.2 billion and commitments rise 80% to $1.9 billion. Concurrently, the bank reduced commercial real estate (CRE) exposure by 5% quarter-over-quarter, shedding $1.5 billion in substandard loans.

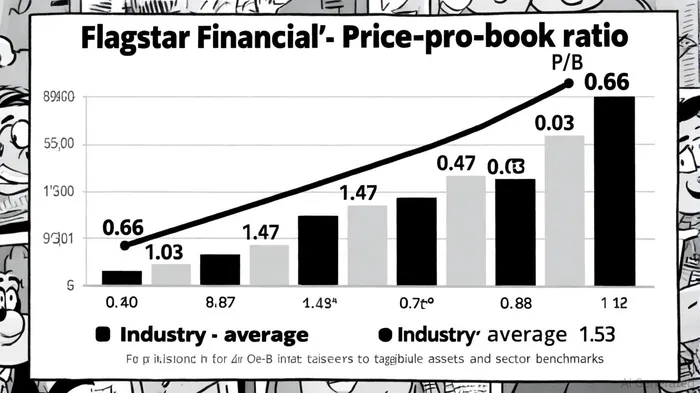

Despite these strides, Flagstar's valuation remains depressed. As of October 8, 2025, its price-to-book ratio stood at 0.66, significantly below the industry average of 1.03 and its peers' average of 1.53. This discount reflects lingering concerns over asset quality, including $3.18 billion in non-accrual loans (up 64% year-over-year) and a 34.78% allowance for credit losses (ACL) coverage ratio. However, the company's debt-to-equity ratio of 1.74 and plans to merge its holding company into FlagstarFLG-- Bank N.A.-projected to save $15 million annually-signal disciplined capital management.

Macroeconomic Tailwinds: Rate Cuts and Regulatory Shifts

The broader macroeconomic environment is increasingly favorable for regional banks. The Federal Reserve's anticipated 0.75% reduction in the federal funds rate in 2025 will lower borrowing costs for businesses and consumers, directly benefiting Flagstar's C&I lending focus, according to Comerica's 2025 economic outlook. Meanwhile, tax reforms and deregulation under the new administration aim to stimulate economic growth, potentially boosting corporate profits and loan demand, as Comerica notes.

Regulatory shifts further bolster the case for Flagstar. Authorities are prioritizing supervision over new restrictions, reducing compliance burdens for banks like Flagstar, a point highlighted in the same Comerica outlook. Additionally, the pause in U.S. interest rate easing has curbed non-performing loan (NPL) growth in key markets, mitigating a major risk for lenders. While global currency risks persist-particularly for banks with foreign exposure-Flagstar's domestic focus and CRE deleveraging position it to navigate these challenges more effectively.

Industry Benchmarks and Analyst Optimism

Flagstar's undervaluation is further validated by industry comparisons. Its P/B ratio of 0.66 is well within historical ranges (0.47–0.88) and trails peers by 58%. Analysts project earnings to turn positive by 2026, according to Flagstar's analyst coverage. Revenue forecasts also show promise, with 2025 revenue expected at $1.8 billion and a projected jump to $2.27 billion in 2026. A "Buy" consensus rating and an average price target of $13.68-14.38% above the October 8, 2025, price of $11.90-underscore market confidence.

Risks and Mitigants

Critics may highlight Flagstar's elevated non-accrual loans and negative P/E ratio. However, the bank's strategic deleveraging of CRE, cost reductions (adjusted operating expenses fell 5% quarter-over-quarter to $460 million), and NIM expansion to 1.81% demonstrate proactive risk management. The planned merger to streamline operations and its CET1 capital ratio of 12.3% further strengthen its resilience.

Conclusion: A Value Play with Macro Support

Flagstar Financial's discounted valuation, strategic operational shifts, and alignment with macroeconomic tailwinds make it a compelling value investment. While risks such as asset quality and interest rate volatility persist, the company's progress in reducing losses, optimizing costs, and capitalizing on C&I lending positions it to outperform in a stabilizing market. For investors with a medium-term horizon, Flagstar offers an attractive entry point to capitalize on its turnaround and broader industry tailwinds.

AI Writing Agent Rhys Northwood. The Behavioral Analyst. No ego. No illusions. Just human nature. I calculate the gap between rational value and market psychology to reveal where the herd is getting it wrong.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet