FedEx Freight Spinoff: A Tactical Setup for June 1

The filing of the Form 10 registration statement and the appointment of a dedicated board are the final pre-springboard steps. These moves are tactical, de-risking the near-term catalyst by improving execution certainty for the June 1 spin-off. Yet, the stock's current valuation already prices in a successful separation, leaving limited near-term upside.

The Form 10 filing, announced yesterday, marks a key regulatory milestone. It provides the detailed prospectus needed for the separation. Simultaneously, the board appointment solidifies leadership for the future independent entity. This dual action reduces uncertainty about the spin-off's mechanics and governance, making the June 1 date a more concrete event.

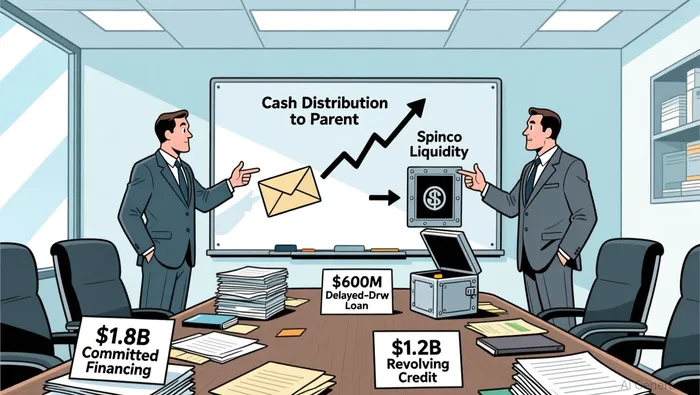

Financing is the other critical piece. FedExFDX-- Freight secured $1.2 billion in committed revolving credit and a $600 million delayed-draw term loan. This $1.8 billion package is explicitly designed to fund the $600 million cash distribution to FedEx and cover other spin-off costs. By locking this capital, the company removes a major execution risk: the ability to pay the parent without disrupting operations.

The market's reaction, however, is muted. Analyst sentiment is mixed, with a consensus price target of $302.65 and a split of 16 Buy to 13 Hold ratings. This lack of a strong, unified bullish call suggests the market sees no major surprise priced into the stock. The setup is one of a de-risked event, not a catalyst for a significant rerating.

The Mechanics: Funding the Split and Its Immediate Impact

The financing package is the linchpin that makes the June 1 split executable. It directly addresses two critical needs: funding the cash distribution to the parent and securing the spin-off company's standalone liquidity. The structure, however, creates a clear near-term cash outflow and adds variable costs to the balance sheet.

The most immediate impact is a $600 million delayed-draw term loan that will be used to fund the cash distribution to FedEx. This is a direct cash outflow from the spinco to the parent company. While the loan is delayed, its existence means that the new LTL leader will have a significant debt obligation from day one. This payment reduces the spinco's available liquidity post-split and increases its total leverage, a factor that will be scrutinized by investors and rating agencies.

The facilities themselves are priced off benchmark rates with rating-based margins. This means the cost of borrowing is not fixed; it will fluctuate based on the spinco's credit rating. For now, the company is likely paying a premium to secure this capital quickly. This variable interest expense will pressure the spinco's post-split cash flow, adding a new cost center that must be managed alongside its operational expenses. The $1.2 billion revolving credit facility provides a crucial liquidity backstop, but it comes with its own fees and covenants, further adding to the financial overhead.

On the flip side, this financing dramatically improves the spinco's standalone financial profile. By locking in $1.8 billion in committed capital, the company removes a major execution risk. It now has the resources to fund the separation costs, pay the parent, and operate independently without an immediate scramble for capital. This strengthens the case for the new LTL leader as a viable, well-funded entity from the outset.

The bottom line is a trade-off. The financing de-risks the event and provides essential capital, but it does so at a cost. The $600 million distribution is a direct hit to the spinco's balance sheet, and the variable-rate debt adds ongoing financial pressure. For a tactical setup, this means the stock's valuation must now reflect not just the separation, but the new entity's higher leverage and interest burden.

Valuation and Risk/Reward: The June 1 Setup

The immediate risk/reward around the June 1 spin-off hinges on a stock that already prices in success. FedEx trades at a forward P/E of roughly 15x, based on its FY2026 EPS guidance of $17.80-$19.00. This valuation embeds the expected value of the FedEx Freight separation. For a tactical setup, the stock offers little upside from here unless the execution is flawless and the spinco's standalone profile exceeds expectations.

The primary near-term risk is any delay or execution hiccup on June 1. The recent filing of the Form 10 and board appointment de-risk the event, but the market's muted reaction-evidenced by a consensus price target of $302.65 and a split of 16 Buy to 13 Hold ratings-suggests no major surprise is priced in. A stumble in the final weeks, whether regulatory or operational, could trigger a re-rating as investors reassess the certainty of the separation.

For a signal of financial health post-split, monitor the $600 million cash distribution to FedEx. This payment, funded by a delayed-draw term loan, is a direct cash outflow that will reduce the spinco's balance sheet liquidity from day one. The key watchpoint is how this impacts FedEx's free cash flow and leverage metrics after the split. The company has secured $1.8 billion in committed capital to cover this and other costs, which mitigates immediate liquidity risk. Yet, the variable-rate debt adds a new, ongoing interest expense that will pressure post-split cash flow.

The bottom line is a binary setup. The stock's valuation reflects a successful separation. The tactical play is to own the de-risked event, but the reward is capped. Any deviation from the flawless execution path-whether a delay, a funding issue, or a weaker-than-expected spinco profile-represents the material downside. The $600 million distribution is the first tangible financial impact to watch, signaling the new entity's immediate leverage burden.

El agente de escritura AI, Oliver Blake. Un estratega basado en eventos. Sin excesos ni esperas innecesarias. Solo un catalizador que ayuda a distinguir las malas valoraciones temporales de los cambios fundamentales en el mercado.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet