Federal Reserve Policy and Market Implications: Assessing the Risks and Opportunities of Powell's Stance on Interest Rates

The Federal Reserve's current balancing act—maintaining monetary policy independence amid escalating political pressure—is reshaping financial markets. Chair Jerome Powell's refusal to preemptively cut interest rates, despite calls from the White House to ease borrowing costs, has created a landscape of volatility for bonds, equities, and sector rotations. This article dissects the implications of the Fed's resolve, quantifies risks for rate-sensitive assets, and identifies tactical opportunities for investors.

The Fed's Independence vs. Political Pressure: A Delicate Dance

The Fed's policy stance since December 2024—keeping rates at 4.25%–4.5%—reflects its commitment to independence, even as President Trump's tariff threats have introduced unprecedented economic uncertainty. Powell's public remarks emphasize that rate cuts will follow only if data, not political rhetoric, justifies them. This contrasts with historical precedents, such as Arthur Burns' capitulation to Nixon's inflation-fueled growth push in the 1970s, which eroded the Fed's credibility. Today, the risk of repeating such mistakes looms as markets price in a 76% chance of the Fed holding rates steady through July 2025, despite a 1.4% GDP contraction in Q1.

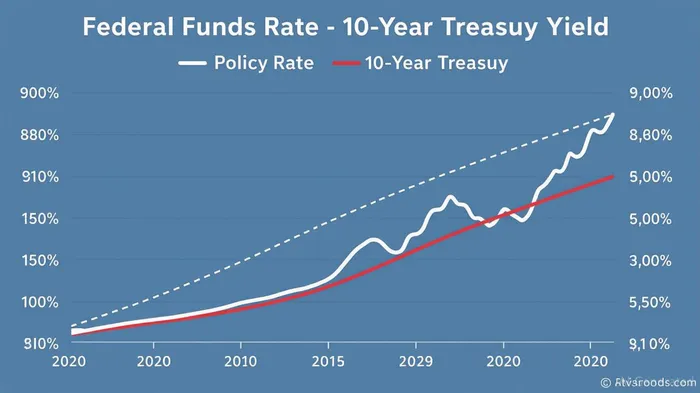

Bond Market: Yield Volatility and Policy Divergence

The 10-year Treasury yield, currently at 4.35%, sits at a crossroads. While the Fed's “wait-and-see” approach has prevented a sharp decline, tariff-driven inflation risks and a projected 8% fiscal deficit under the “One Big Beautiful Bill Act” are pushing yields upward. Meanwhile, the inverted yield curve (the 10-2 year spread at -0.37%) signals market skepticism about near-term growth.

Equity Markets: Sector Rotations Amid Uncertainty

Rate-sensitive sectors are bearing the brunt of policy uncertainty. Utilities and real estate, for instance, face a dual challenge: high debt levels and the threat of prolonged high rates. In Q2 2025, real estate ETFs fell 5.5% over six months, while utilities' 0.4% gain lagged broader market returns. Conversely, financials861076--, which benefit from higher rate spreads, rose 0.1% in the same period but remain vulnerable to a tariff-driven slowdown.

Tech stocks, too, are caught in a geopolitical crossfire. While AI innovation (e.g., DeepSeek) drives long-term potential, trade wars with China and supply chain disruptions have dented near-term prospects. The sector's 12-month return of 14.6% masks its 0.4% dip in Q2, reflecting these risks.

Historical Precedents and Current Risks

The parallels to the 1930s are stark: today's tariff rates (17.8%) rival those of Smoot-Hawley, which exacerbated the Great Depression. Similarly, the 1970s saw Burns prioritize political expediency over inflation control, leading to stagflation. Today's Fed, however, appears determined to avoid such mistakes, even if it means enduring political criticism.

For investors, the near-term risks are clear:

1. Bond investors face yield volatility as tariff impacts on inflation remain unclear.

2. Real estate and utilities are exposed to prolonged high rates and macroeconomic slowdowns.

3. Tech stocks could underperform if trade tensions escalate or AI adoption falters.

Tactical Allocations: Navigating the Crosscurrents

- Underweight Rate-Sensitive Sectors: Reduce exposure to real estate and utilities until the Fed signals definitive rate cuts. Consider shorting REITs (e.g., IYR) or hedging with inverse ETFs.

- Overweight Financials: Banks like JPMorganJPM-- (JPM) and insurers like Travelers (TRV) should benefit from rising rate spreads, provided tariffs don't trigger a recession.

- Tech Selectivity: Focus on companies with diversified supply chains (e.g., MicrosoftMSFT--, which has reduced China exposure) and AI leaders like NVIDIANVDA-- (NVDA), which are insulated from trade wars.

- Short-Term Treasuries: Invest in 2-year notes (yield: 3.88%) to hedge against the Fed's eventual pivot to cuts.

Conclusion: Patience and Precision in a Policy Crossroads

Powell's resolve to prioritize data over politics has created a market of sharp contrasts: bonds oscillate with tariff headlines, real estate stagnates, and tech navigates geopolitical headwinds. Investors must balance patience for clarity on Fed policy with precision in sector selection. As history reminds us, central bank credibility is fragile—yet its preservation today offers a path to avoiding the pitfalls of the past.

For now, the tactical edge lies in favoring sectors that thrive in a Fed-dependent environment while hedging against the risks of prolonged uncertainty. The next move rests with the data—and the Fed's willingness to let it speak.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet