Federal Reserve's Delicate Balancing Act: Inflation Data and the Road to Rate Cuts

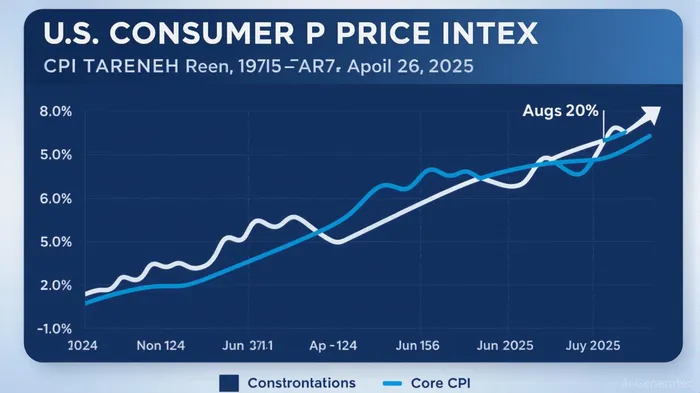

The Federal Reserve faces a pivotal juncture in 2025 as it navigates the interplay between stubborn inflation and a cooling labor market. , the central bank remains cautious about the lingering effects of 's tariffs and the fragility of employment trends. While headline inflation has moderated from 2022 peaks, , driven by shelter costs and tariff-sensitive categories like furniture and apparel. This divergence between headline and core metrics underscores the Fed's challenge: distinguishing between temporary price shocks and entrenched inflationary pressures.

. However, . , with expectations of further reductions in December and early 2026. This trajectory hinges on upcoming inflation data, particularly the August CPI and PPI reports, which will clarify whether tariff-driven price increases are isolated or part of a broader inflationary trend.

The Fed's dual mandate—price stability and maximum employment—has created internal divisions. While officials like and advocate for preemptive easing to cushion the labor market, others caution against overreacting to one-off inflation spikes. , the case for rate cuts strengthens. Conversely, a rebound in service-sector inflation could delay action.

The implications for the U.S. dollar are profound. A rate-cutting cycle would reduce the yield appeal of dollar assets, triggering capital outflows and a weaker USD. The dollar index, currently in a range-bound pattern, could face downward pressure as investors rotate into higher-yielding emerging market currencies or intermediate-duration bonds. Fixed-income markets are already pricing in a flattening yield curve, with short-term rates expected to fall and long-term yields stabilizing as investors demand higher term premiums for duration risk.

For investors, the path forward requires a nuanced approach. A weaker dollar could boost U.S. exporters and multinational corporations with foreign-currency revenue streams. Equities in rate-sensitive sectors—such as real estate, utilities, and small-cap stocks—may outperform as borrowing costs decline. Conversely, dollar-hedged positions and short-term bonds could offer downside protection in a volatile environment.

Hedging strategies should also account for geopolitical risks. Trump's tariffs, while seen as temporary by the Fed, could disrupt global supply chains and reignite inflationary pressures. Investors should monitor the September report and the October CPI data for clues on the Fed's next move. , though unlikely, would signal a more aggressive pivot and accelerate the dollar's decline.

In conclusion, the Fed's policy trajectory in 2025 will be dictated by the interplay of inflation data and labor market dynamics. , but its magnitude and timing depend on whether inflation remains contained. For now, investors should position portfolios to benefit from a weaker dollar, prioritize liquidity, and remain agile in response to shifting economic signals. The coming months will test the Fed's resolve—and the markets' resilience.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet