Fed's Tightening Crossroads: How Mortgage Rates Are Reshaping Housing Markets and MBS Opportunities

The Federal Reserve's prolonged era of restrictive monetary policy has left its indelible mark on the U.S. housing market. Mortgage rates, now hovering near 6.8%, have become a double-edged sword: they've cooled demand for homeownership but created fertile ground for strategic real estate and fixed-income investments. For investors navigating this landscape, understanding the Fed's policy calculus—and its ripple effects—is critical to spotting opportunities in mortgage-backed securities (MBS) and real estate.

The Fed's Tightrope Walk

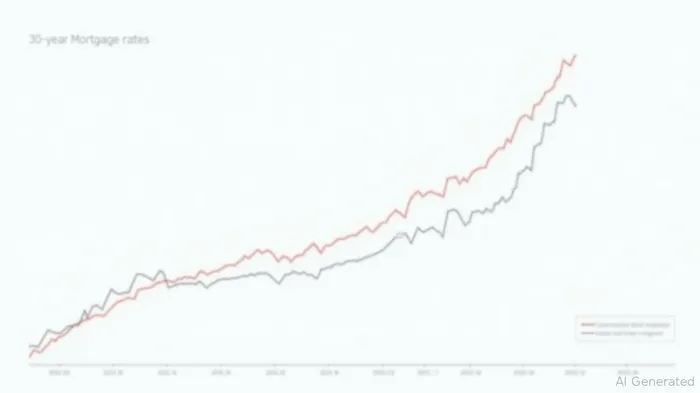

Since 2023, the Fed has walked a precarious line between taming inflation and avoiding an economic slowdown. After hiking the federal funds rate to a 20-year high of 4.5% in 2023, it began modest cuts in 2024, trimming rates by 1% to reach 4.25%-4.5% by early 2025. Yet, the policy remains “restrictive,” with the Fed holding rates steady through mid-2025 as it weighs persistent inflation (core PCE at 2.8%) against slowing GDP growth (1.7% in 2025).

This caution has kept mortgage rates elevated. The average 30-year fixed-rate mortgage stood at 6.84% in June 2025, down only slightly from its 2022 peak of 7.04%.

The Squeeze on Homebuyers

The mathMATH-- for prospective buyers is stark. Consider a median-priced home of $417,000: at 6.8%, the monthly payment soars to $2,788—a 40% jump from the pandemic-era 3% rate. This has slowed sales, with the median time on the market rising to 50 days in early 2025. First-time buyers, in particular, face a steep climb: their share of purchases fell to just 29% in 2024, down from 40% in 2019.

Yet, the market isn't collapsing. Higher prices (up $100,000 since 2020) and limited inventory mean many sellers hold out for better terms. The result? A bifurcated market: affordability is a crisis for marginal buyers, but core markets with strong job growth—like tech hubs—remain resilient.

MBS: The Hidden Opportunity in Fed Uncertainty

While homeowners struggle, mortgage-backed securities are emerging as a relative bargain. Agency RMBS—bonds backed by government-guaranteed mortgages—now offer spreads over Treasuries wider than corporate bonds, a rare dislocation not seen in over 20 years.

The catalyst? Reduced demand from traditional buyers. The Fed's balance sheet runoff, which has shrunk its MBS holdings by $534.5 billion since 2022, and the fallout from 2023's regional bank failures have left fewer buyers to absorb supply. Meanwhile, geopolitical risks—like President Trump's tariff policies, which threaten to reignite inflation—have kept yields elevated.

For investors, this creates two avenues:

1. Agency RMBS: Their explicit government backing makes them a safe haven. The widening spread versus corporates suggests they're undervalued.

2. Non-Agency RMBS (NA RMBS): These securities, tied to riskier mortgages like subprime or jumbo loans, offer even steeper discounts. If rates dip—say, to the mid-6% range by year-end—prepayment risks turn into rewards, as borrowers refinance, boosting investor returns.

Risks and the Fed's Next Move

The Fed's next steps will determine outcomes. By mid-2025, the June FOMC meeting offered no immediate cuts, but markets priced in two 25-basis-point reductions by year-end. If realized, these cuts would steepen the yield curve, lifting MBS prices. However, risks linger:

- Tariff-Driven Inflation: Escalating trade tensions could force the Fed to pause or reverse cuts.

- Labor Market Resilience: A stronger-than-expected jobs report (e.g., May's 139,000 net new jobs) could keep inflation elevated.

Strategic Playbook for Investors

- Ladder MBS Exposure: Use ETFs like iShares Mortgage Real Estate Bond ETF (REM) to diversify across maturities and sectors.

- Focus on NA RMBS: Consider ETFs like BlackRock's BINC, which targets higher-yielding MBS and collateralized loan obligations (CLOs).

- Monitor Prepayment Metrics: Track refinancing activity; a drop in rates could trigger a wave of prepayments, boosting yields on discounted MBS.

Conclusion: The Fed's Policy Crossroads

The Fed's dilemma—containing inflation without choking growth—has turned mortgage markets into a battleground of competing forces. For investors, the dislocations in MBS pricing and the Fed's eventual pivot toward rate cuts present a compelling entry point. While homeowners brace for affordability headwinds, the MBS market offers a way to profit from the Fed's “higher for longer” policy. As Chair Powell noted, “the data will guide us”—and that data, for now, points to opportunities in fixed income's overlooked corner.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet