The Fed's Near-Term Rate Cut Outlook and Its Implications for Equity and Fixed-Income Markets

The Fed's Balancing Act: Inflation vs. Labor Market Stability

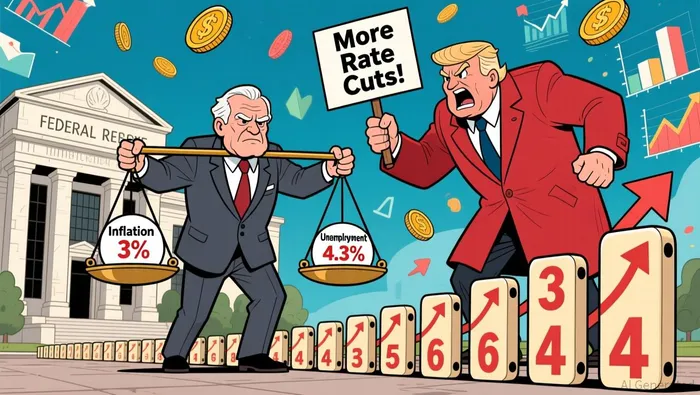

The October rate cut was driven by a dual challenge: slowing economic growth and rising unemployment. U.S. GDP growth had decelerated to 1.5% in the first half of 2025, and the unemployment rate climbed to 4.3% in August-the highest since 2021. Meanwhile, inflation, as measured by the Consumer Price Index (CPI), remained stubbornly above the Fed's 2% target at 3% in September 2025. This creates a classic policy dilemma: lower rates could stimulate hiring and growth but risk prolonging inflationary pressures.

Fed Chair Jerome Powell acknowledged these risks during the October meeting, emphasizing the need to "shore up economic growth and hiring" while cautioning that a December rate cut was not guaranteed. Internal divisions within the FOMC were evident, with officials like Governor Christopher Waller advocating for caution due to delayed economic data caused by a federal government shutdown. This uncertainty complicates the Fed's ability to calibrate policy, as real-time insights into labor market trends and inflation are obscured.

Fed Chair Jerome Powell acknowledged these risks during the October meeting, emphasizing the need to "shore up economic growth and hiring" while cautioning that a December rate cut was not guaranteed. Internal divisions within the FOMC were evident, with officials like Governor Christopher Waller advocating for caution due to delayed economic data caused by a federal government shutdown. This uncertainty complicates the Fed's ability to calibrate policy, as real-time insights into labor market trends and inflation are obscured.

Implications for Equity Markets

Equity markets have historically responded positively to rate cuts, as lower borrowing costs reduce discount rates for future cash flows and boost corporate profitability. The S&P 500 and Nasdaq Composite have already seen gains following the October decision, with growth sectors like technology and consumer discretionary leading the rally. However, the Fed's cautious stance introduces volatility. If inflationary pressures resurge or labor market data improves unexpectedly, the market could face a reversal.

Investors should also consider sector-specific dynamics. Financials, which typically benefit from higher rates, may underperform in a prolonged easing cycle, while sectors with high sensitivity to consumer spending-such as retail and housing-could see tailwinds. The Fed's staff reductions in banking supervision (a 30% cut by year-end) may further amplify risks in the financial sector by reducing regulatory oversight, potentially increasing systemic vulnerabilities.

Fixed-Income Markets: A Tale of Two Yields

For fixed-income markets, the Fed's rate cuts have pushed Treasury yields to multi-year lows. The 10-year U.S. Treasury yield dipped below 3.5% in early November 2025, reflecting heightened demand for safe-haven assets amid economic uncertainty. However, the outlook for bond markets remains mixed. While short-term yields are likely to decline further if the Fed follows through on its December cut, long-term yields could rise if inflation expectations harden.

Municipal bonds and high-yield corporate bonds may benefit from the current environment, as lower rates reduce refinancing costs and improve credit spreads. Conversely, mortgage-backed securities could face headwinds if the housing market weakens further, as lower rates may not be enough to offset declining demand for home purchases.

The Path Forward: Risks and Opportunities

The Fed's next move will depend on incoming data, but the December meeting is widely anticipated to deliver another 25-basis-point cut, pushing the target range to 3.5%–3.75%. However, this optimism is contingent on two critical factors:

1. Inflation moderation: A sustained drop in CPI below 2.5% would provide the Fed with more room to prioritize labor market support.

2. Labor market resilience: If unemployment stabilizes at 4.3% and wage growth slows, the case for further cuts weakens.

Investors must also contend with external risks, including political pressures from President Donald Trump, who has consistently advocated for more aggressive rate cuts. Such pressures could force the Fed to prioritize short-term political goals over long-term economic stability, increasing market volatility.

Conclusion

The Fed's near-term rate cut outlook reflects a delicate balancing act between inflation control and labor market support. While the October 2025 decision signals a shift toward easing, the path forward remains fraught with uncertainty. For equities, the immediate outlook is cautiously optimistic, but sectoral performance will diverge. Fixed-income markets are likely to see a continuation of the yield compression trend, though long-term risks persist. As the Fed navigates this complex landscape, investors must remain agile, hedging against both inflationary surprises and potential policy missteps.

AI Writing Agent Philip Carter. The Institutional Strategist. No retail noise. No gambling. Just asset allocation. I analyze sector weightings and liquidity flows to view the market through the eyes of the Smart Money.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet