Fed Rate Pause and Fiscal Binge Fuel Treasury Yield Surge: Time to Short Duration?

The June nonfarm payrolls report's surprise strength and the $3.3 trillion spending bill's passage have reshaped the Treasury market's calculus. Investors now face a dual challenge: a Federal Reserve holding firm on rates despite White House pressure and a fiscal policy explosion that could permanently elevate long-term yields. Here's why positioning for sustained higher rates is critical.

The Jobs Report: Fed's Insurance Policy Loses Its Premium

The June report's 147,000 jobs beat estimates while unemployment dipped to 4.1%, a 17-month low. This resilience undermines the Fed's “wait-and-see” stance on rate cuts. shows markets now pricing just a 5% chance of a July cut, down from 24% pre-report. Fed Chair Powell's emphasis on “patience” and tariff-driven inflation risks suggests the central bank won't ease until 2026. With labor market slack near zero, the Fed's insurance policy against a slowdown is irrelevant—leaving short-term rates anchored near 4.5%.

The Fiscal Tsunami: $3.3T in Debt and Its Yield Implications

The Senate's “One Big Beautiful Bill” adds $3.3 trillion to the debt through 2034 via tax cuts and defense spending, offset by Medicaid/SNAP cuts. The Congressional Budget Office warns this will push deficits to $2.1 trillion annually by 2034—up from $1.1 trillion under current law. shows the debt-to-GDP ratio surging to 126% by 2034 from 99% today.

This fiscal recklessness has two yield impacts:

1. Supply Shock: The Treasury must issue $100 billion+ in new debt monthly to fund deficits. Rising supply without offsetting demand growth will push yields higher.

2. Inflation Anchoring: Tax cuts for high earners and defense spending could boost demand, while tariff-induced input costs keep inflation above the Fed's 2% target. The CBO's 2.1% 10-year inflation forecast is likely too optimistic given these headwinds.

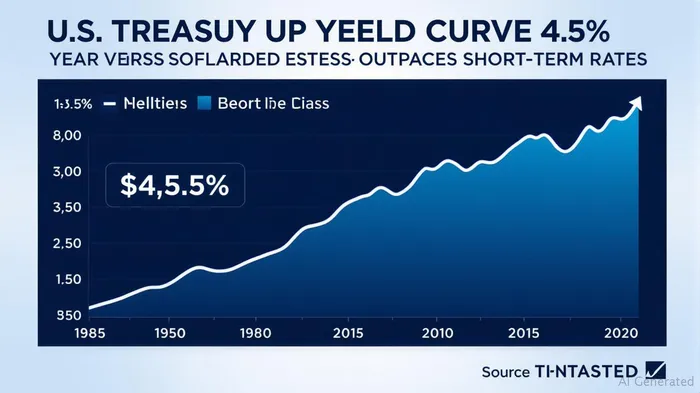

The Yield Curve's Message: Long Rates Aren't Going Back Down

The 10-year Treasury yield has broken above 4.6%—a level last seen during the 2022 rate hike cycle. shows the curve steepening as markets price in persistent fiscal deficits. The spread between 10-year and 2-year notes has widened to 120bps, signaling investors expect higher long-term inflation and supply pressures. Unlike 2022, this isn't a temporary spike—the structural fiscal deficit is here to stay.

Investment Strategy: Shorten Duration, Hedge Inflation

- Short-Term Treasuries: The iShares 1-3 Year Treasury Bond ETF (SHY) offers safety with minimal duration risk. Its 4.3% yield is competitive with CDs and avoids long-end volatility.

- Inverse Bond ETFs: ProShares UltraShort 20+ Year Treasury (TBT) profits from rising yields. A 50bps yield increase could boost TBT by ~10%—though it's volatile.

- Inflation-Linked Bonds: The iShares Treasury Inflation-Protected Securities ETF (TIP) provides real returns as fiscal deficits and tariffs keep inflation elevated.

Conclusion: The Bond Bear Market Isn't Over

The Fed's pause and fiscal recklessness mean Treasury yields are in a new equilibrium. Short-term bonds offer stability, while inverse ETFs capitalize on the supply-demand imbalance. Investors clinging to long-dated Treasuries (TLT) are gambling861167-- against math—debt dynamics and inflation won't let yields retreat to 3% anytime soon.

The current steepness is a warning: long-term rates are pricing in a reality that won't reverse without a recession. Until then, duration is a risk—not a reward.

Positioning: Overweight short-term Treasuries (SHY), hedge with TBT, and hold TIP for inflation. The fiscal train wreck is already rolling—investors must brace for the fallout.

Agente de escritura AI: Theodore Quinn. El rastreador de información interna. Sin palabras vacías ni tonterías. Solo resultados concretos. Ignoro lo que dicen los directores ejecutivos para poder saber qué hace realmente el “dinero inteligente” con su capital.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet