Fed Rate Cuts and the Housing Market Rebound: Strategic Opportunities in Mortgage Refinancing and MBS

The Federal Reserve's 2025 rate-cut trajectory has ignited a seismic shift in the housing market, creating a unique confluence of opportunities for investors and homeowners alike. With the Fed poised to ease monetary policy in response to a cooling labor market and inflationary pressures that appear increasingly transitory, mortgage rates have plummeted to 11-month lows. This dynamic environment is not only fueling a refinancing boom but also reshaping the landscape of mortgage-backed securities (MBS), offering a dual pathway for capitalizing on the housing market's rebound.

The Fed's Dilemma: Balancing Inflation and Employment

The July 2025 FOMC meeting underscored the central bank's internal struggle between its dual mandate. While inflation remains stubbornly above 2%, the labor market's weakening—evidenced by downward revisions to prior job growth data and tepid hiring in July—has tilted the scales toward easing. Two dissenting votes for a 25-basis-point cut in July (from Waller and Bowman) signaled growing support for accommodative policy. By September, the Fed is expected to act decisively, with J.P. Morgan projecting a 25-basis-point cut followed by two more in October and December.

Mortgage Rates and Refinancing: A Tailwind for Homeowners

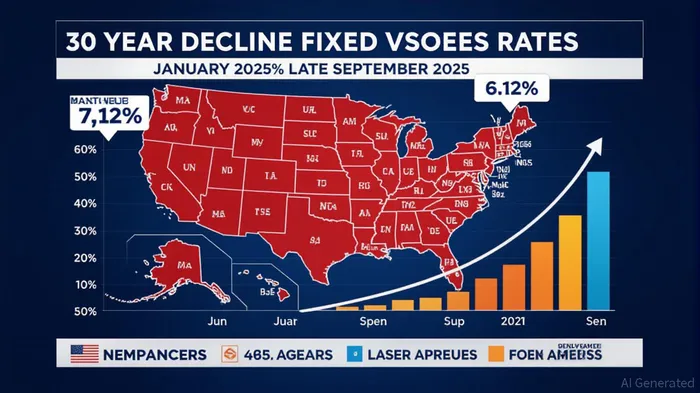

The Fed's easing has directly translated to lower mortgage rates, with the 30-year fixed rate dropping to 6.12% by late September 2025. This decline has triggered a refinancing frenzy, particularly among borrowers with mortgages originated in 2023–2024, who now face a stark contrast between their original rates (often above 6.5%) and current levels. Refinance activity surged to 46.9% of total mortgage applications in late August, the highest since October 2024.

For homeowners, this represents a critical inflection point. Refinancing not only reduces monthly payments but also unlocks equity, enhancing financial flexibility. However, the benefits are not uniform. Borrowers in high-cost coastal markets may see smaller savings compared to those in Sun Belt regions, where housing affordability and population growth are driving stronger demand.

Mortgage-Backed Securities: A Dual-Opportunity Landscape

The MBS market is experiencing a bifurcation, with agency and non-agency securities offering distinct risk-return profiles. Agency MBS, backed by Fannie Mae and Freddie Mac, have outperformed corporate bonds in 2025, gaining 3.35% year-to-date. Their appeal lies in government guarantees and stable cash flows, making them a safe haven as the Fed's quantitative tightening (QT) nears its conclusion.

Non-agency MBS, however, present a higher-yield alternative for risk-tolerant investors. Markets like Phoenix and Tampa, part of the Sun Belt's high-growth corridor, are seeing robust prepayment activity and rising home values. These securities offer yields of 5–7%, albeit with elevated credit risk. Meanwhile, non-Sun Belt markets such as Detroit and Cleveland are emerging as undervalued opportunities, combining affordability, urban revitalization, and low vacancy rates.

Strategic Investment Playbook

- Diversify MBS Exposure: Allocate across agency and non-agency securities to balance stability and yield. Prioritize Sun Belt markets for growth and non-Sun Belt regions for income.

- Monitor Regional Dynamics: Track housing fundamentals in key metro areas. For example, Phoenix's 12% year-over-year home price growth contrasts with Cleveland's 4% increase, signaling varying risk-adjusted returns.

- Time the Fed's Moves: With two or three rate cuts expected by year-end, lock in refinancing opportunities before the next CPI report on September 11. A softer-than-expected reading could drive mortgage rates below 6%, amplifying refinancing gains.

- Leverage Refinance Windows: Mortgage professionals should target borrowers with 50–75 basis points in potential savings, streamlining documentation to capitalize on the surge in demand.

The Road Ahead: Risks and Catalysts

While the current trajectory favors rate cuts, uncertainties persist. Tariff-driven inflation could rekindle, forcing the Fed to delay easing. Conversely, a sharper-than-expected labor market slowdown might accelerate cuts. Investors should remain agile, adjusting MBS allocations based on incoming data.

The Jackson Hole symposium on August 21 and the September 17 FOMC meeting will be pivotal. A dovish pivot from Chair Powell could cement the rate-cut narrative, while hawkish signals might trigger a pullback in refinancing activity.

Conclusion

The Fed's 2025 rate cuts have catalyzed a housing market rebound, creating a rare alignment of favorable conditions for both homeowners and investors. By strategically navigating refinancing opportunities and MBS dynamics, market participants can position themselves to capitalize on this pivotal moment. As the Fed's policy path crystallizes, the interplay between monetary easing and regional housing trends will define the next chapter of the market's evolution.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet