Fed's 'Hawkish Cut' on the Way, but Powell May Strike a Cautious Tone — What to Expect

The Fed's final policy showdown of 2025 is about to take the stage. The central bank is widely expected to deliver another 25-basis-point cut and unveil fresh dot-plot projections and economic forecasts on Wednesday. Even though Chair Jerome Powell has downplayed the need for additional easing—arguing that policy is already sufficiently accommodative—the government shutdown, economic soft patches, and a cooling labor market are pushing the Fed toward a preemptive move. Still, this insurance cut could come at the expense of future easing, which makes Powell's press-conference commentary the true market catalyst. The countdown to his departure may have begun, but one Powell remark still moves trillions.

Expectations are fully priced in. According to FedWatch, there's an 88% probability the Fed delivers a 25-basis-point cut—its third consecutive reduction. If so, the target range would fall to 3.5%–3.75%, exactly in line with the median projection from the previous dot plot.

But internal divisions at the Fed remain sharp. Some officials support cutting to buffer further labor-market deterioration, while others argue policy has already gone far enough and that additional easing risks reigniting inflation. With the November shutdown freezing official economic releases, the latest labor and inflation data still reflect September conditions. Nonfarm payrolls rose 119,000—far above the 50,000 consensus—while the unemployment rate climbed to 4.4%, the highest since October 2021. Core PCE, the Fed's preferred inflation gauge, increased 2.8% year over year—well above the 2% target.

It's also worth noting that the Fed already cut rates in September and October and will halt balance-sheet runoff starting in December. But because of the shutdown—and the lagged impact of policy—none of these moves have fully appeared in the data. Layer on another cut now, and the economic and policy outlook becomes even murkier.

That's exactly why 'hawkish cut' has become the buzzword for this meeting. In market terms, it means: yes, they cut—but don't expect another one anytime soon.

"The likeliest outcome is a kind of hawkish cut where they cut, but the statement and the press conference suggest that they may be done cutting for now," said Bill English, the Fed's former director of monetary affairs and now a Yale professor.

The statement may revive language from last December about assessing "the extent and timing of additional adjustments," effectively raising the bar for further easing and tying it directly to incoming data. Historically, that phrasing has signaled a policy pause—suggesting December's cut could mark the final step in this risk-management easing cycle.

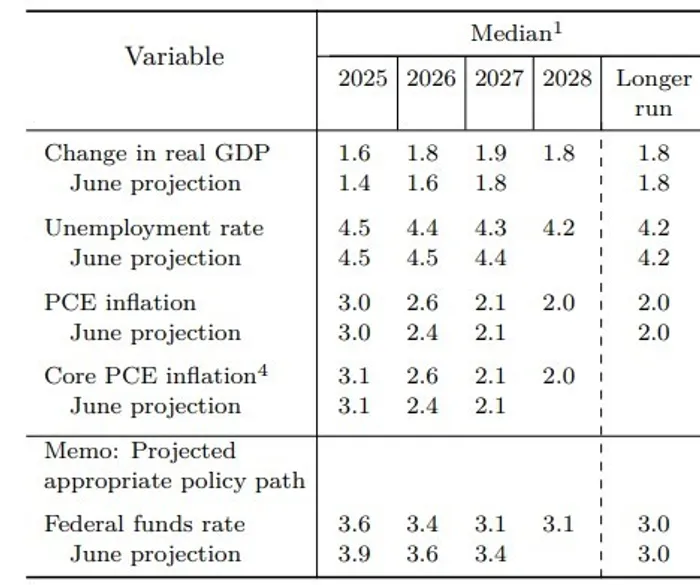

The Fed will release new economic projections, though major changes are unlikely. Growth for this year could see a modest upward revision (from 1.6%), unemployment may hold steady or tick higher (from 4.5%), while inflation (PCE and core PCE) and the rate outlook are expected to remain largely unchanged.

The real focus is the dot plot, covering expectations for next year and the longer run. Back in September, Fed officials penciled in only one cut for 2026, with the longer-run rate anchored at 3%. That leaves ample room for downside risks without forcing the Fed to shift prematurely. And with easing still working its way through the system—and inflation and jobs moving toward balance—the committee is increasingly data-dependent.

A spoonful of sugar and a slap on the wrist—that's Powell's trademark balancing act. Missing data, untested easing, and an uncertain inflation path mean the Fed isn't in a rush to cut. But rising unemployment and complications from the shutdown justify a preventive step—even as officials worry about losing control of the inflation narrative. It's a genuine policy dilemma.

"Inflation is not back to 2%, so they're going to need to keep policy somewhat restrictive if they are going to put downward pressure on inflation," former Cleveland Fed President Loretta Mester said Tuesday on CNBC. "Right now, inflation is clearly above the goal, and it's not just tariff-driven."

Still, Mester sees Wednesday's cut as a done deal. "I think they're going to follow through with that last cut," she said. "I do hope they signal that the economy has reached a point where policy is in a good place and that they're going to slow down the pace of cuts, because I am more concerned about inflation risks and stickiness."

Beyond rates and the dot plot, the committee may hint at its next steps on balance-sheet management. The Fed already announced in October that it would halt quantitative tightening. But with ongoing pressures in the overnight funding markets, some investors expect a shift back toward bond purchases—though not at a scale resembling full-blown quantitative easing.

While Powell still dominates the FOMC for now, his term ends in May. Trump-favored frontrunner Kevin Hassett has been loudly shaping the narrative—adding more uncertainty to next year's policy trajectory. Hassett has argued that rates have "plenty of room to fall," signaling closer alignment with Trump's stance. Powell will almost certainly be asked about succession, though it may not yet factor into the rate debate. Even so, 2026 could bring a dramatic policy reset.

Crypto market researcher and content strategist with 3 years of experience in digital asset analysis and market commentary. Skilled at transforming complex blockchain data and trading signals into clear, actionable insights for investors. Experienced in covering Bitcoin, Ethereum, and emerging ecosystems including DeFi, Layer2, and AI-related projects. Passionate about bridging professional market research with accessible storytelling to empower readers and investors in the fast-evolving crypto landscape.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet