Fed-Favored PCE Inflation at 2.8% Sparks Market Optimism

The Fed's Cautious Path to Rate Cuts

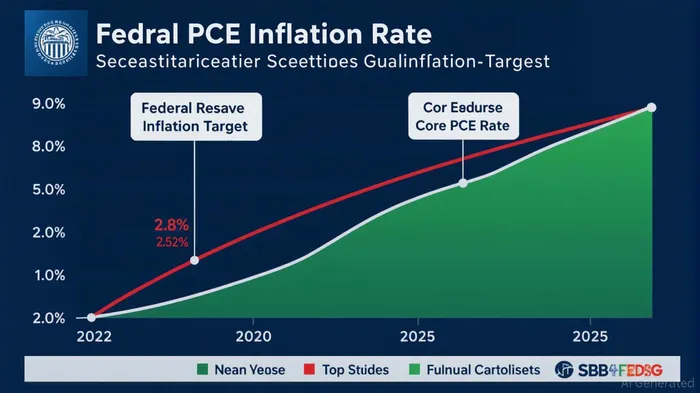

The Federal Reserve's September 2025 policy projections underscore a measured approach to easing monetary policy. While inflation remains stubbornly above 2%, the gradual cooling of core PCE to 2.8% has increased the likelihood of rate reductions in 2026 and 2027. The FOMC now anticipates a federal funds rate of 3.4% by 2026 and 3.1% by 2027, reflecting a strategy to lower borrowing costs while avoiding a resurgence of inflationary pressures. This trajectory is supported by weakening labor market indicators, such as a trailing 4-month average of new job creation dropping to 54,000-a stark contrast to earlier averages of 167,000.

The Fed's dual mandate-price stability and maximum employment-has shifted toward prioritizing employment concerns in recent months. As stated by the St. Louis Fed, the central bank's preference for the PCE index over the CPI stems from its ability to capture evolving consumer spending patterns, which have been shaped by post-pandemic dynamics. However, the persistence of inflation, particularly in non-market-based PCE components like imputed financial services, complicates the case for rapid rate cuts.

Equity Valuations in the Shadow of Rate Cuts

The prospect of lower interest rates has already begun to reshape equity valuations. Historically, rate cuts have favored sectors with high sensitivity to borrowing costs, such as utilities, real estate, and energy. In 2025, this trend has been amplified by structural shifts, including surging demand for energy from data center expansions, which have propelled utility stocks to outperform broader indices. Lower rates also reduce the discount rate applied to future corporate earnings, making equities more attractive relative to cash or bonds.

Market optimism is further fueled by the positive correlation between falling interest rates and risk-on sentiment. As BlackRock notes, easing monetary policy typically encourages investors to shift toward higher-yielding assets, including intermediate-duration bonds and alternative investments like real estate and commodities. The S&P 500's recent record highs reflect this dynamic, with investors positioning for a more accommodative environment even as inflation remains above target.

Investor Behavior and Global Diversification

The anticipation of Fed rate cuts has also spurred a reevaluation of portfolio strategies. JPMorgan highlights a growing emphasis on global diversification, as international markets-particularly in emerging economies like India and South Korea-offer compelling valuations and growth drivers distinct from the U.S. This shift is partly driven by the recognition that U.S. equity valuations, while resilient, are increasingly disconnected from macroeconomic realities.

However, the relationship between rate cuts and market performance is not without risks. As noted in a CFA Institute analysis, past Fed rate-cutting cycles have produced mixed outcomes, with some periods avoiding recessions while others have exacerbated economic downturns. The current environment, characterized by low volatility and uneven inflationary pressures, adds layers of uncertainty. For instance, non-market-based PCE inflation-tied to stock market gains-remains elevated, suggesting that financial assets may be inflating broader inflation metrics.

Conclusion: A Delicate Equilibrium

The 2.8% core PCE reading represents a pivotal moment in the Fed's inflation fight. While it signals progress, the path to the 2% target remains fraught with challenges, including structural inflationary pressures and a labor market that continues to influence policy decisions. For investors, the key lies in balancing the short-term benefits of rate cuts with the long-term risks of overvaluation and economic imbalances.

As the Fed edges toward a more accommodative stance, equities are likely to remain a favored asset class, particularly in sectors poised to benefit from lower borrowing costs. Yet, a diversified approach that incorporates global opportunities and alternative assets will be critical for navigating the uncertainties ahead. In this evolving landscape, the interplay between inflation, monetary policy, and market psychology will continue to shape investment outcomes in 2026 and beyond.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet