The Fed's Dilemma: How Tariffs Could Derail Rate Hikes and Create Opportunities in Bonds

The Federal Reserve finds itself in a precarious "purgatory" of its own making, torn between curbing tariff-driven inflation and avoiding a growth slowdown that could trigger a recession. With tariffs reshaping global trade and domestic prices, the Fed's path forward is clouded by uncertainty—a scenario that could fuel a rally in fixed-income markets. For investors, this policy gridlock presents a rare opportunity to reallocate portfolios toward duration and high-quality debt, as monetary ambiguity becomes a tailwind for bonds.

The Fed's Crossroads: Tariffs Complicate Rate Decisions

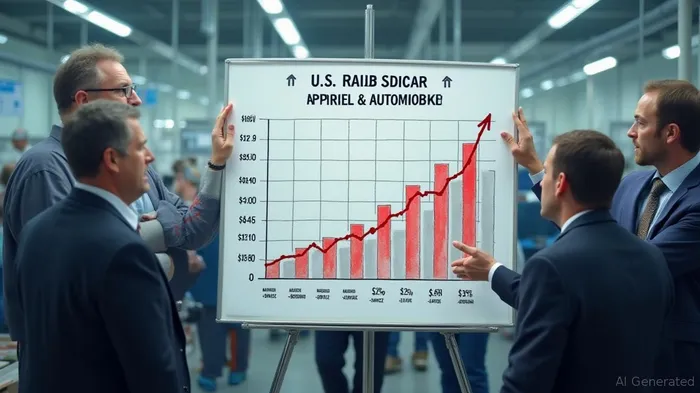

The U.S. tariff regime, now at its highest level since 1901, has injected chaos into the Fed's inflation-fighting calculus. Recent data shows that tariffs have already pushed consumer prices higher: apparel costs surged 65% in the short term, while motor vehicles rose 12% (see  ). While the Fed's preferred inflation measure, the PCE price index, remains at 2.1%, tariff-induced costs could push the Core CPI to 4% by mid-2025. Yet, these price hikes are likely temporary, as businesses adjust supply chains and demand softens.

). While the Fed's preferred inflation measure, the PCE price index, remains at 2.1%, tariff-induced costs could push the Core CPI to 4% by mid-2025. Yet, these price hikes are likely temporary, as businesses adjust supply chains and demand softens.

The Fed faces a paradox: raising rates to preempt inflation risks choking off growth, while pausing hikes risks letting inflation spiral. This uncertainty is reflected in the latest “dot plot,” which shows a median expectation of one to two rate cuts by year-end—a stark contrast to earlier hawkish projections. . The central bank's “wait-and-see” approach is creating a prolonged period of policy ambiguity, which historically has favored bonds over equities.

Bond Market Dynamics: Duration and Quality Win

The Fed's hesitation is already reshaping fixed-income markets. The 10-year Treasury yield has fallen from 4.5% to 3.8% since January 2025, driven by expectations of slower rate hikes (see ). This compression of yields is a direct reflection of investors pricing in lower terminal rates. Meanwhile, corporate bond spreads—the extra yield over Treasuries—have narrowed slightly for investment-grade debt but widened for high-yield issuers, signaling a flight to quality (see ).

This divergence underscores a key investing thesis: duration and high-quality debt are the safest bets in this environment. Longer-dated Treasuries and investment-grade corporates offer insulation against both inflation and growth risks. For example, the iShares 20+ Year Treasury Bond ETF (TLT) has outperformed the S&P 500 by 8% year-to-date, while the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD) has held up better than cyclical stocks amid slowing manufacturing data.

Historical Precedents: When Policy Gridlock Boosted Bonds

History offers a playbook for navigating Fed purgatory. In the late 1990s, the Fed delayed rate hikes amid trade wars and tech-sector volatility, leading to a 30% rally in 10-year Treasuries. Similarly, during the 2010–2011 European debt crisis, prolonged uncertainty about Fed policy saw bond yields drop even as equity markets stagnated.

Today's parallels are stark: tariff-driven inflation is temporary but disruptive, while the Fed's options are constrained by global supply chain fragility. A prolonged pause in rate hikes—or outright cuts—could push the 10-year yield below 3%, a level not seen since 2021. For bond investors, this means extending duration without overexposure to credit risk.

Investment Strategy: Allocate to Duration and Quality

- Duration Over Cash: Shift toward long-dated Treasuries (e.g., TLT) and intermediate-term bonds (e.g., IEF) to capture yield declines.

- Quality Over Yield: Favor investment-grade corporates (LQD) over high-yield bonds (HYG), as defaults rise in a slowing economy.

- Diversify Globally: Consider developed-market sovereign bonds (e.g., BNDX), which benefit from dollar weakness and global rate cuts.

- Monitor Tariff Policy: Track tariff revisions and trade negotiations—any escalation could accelerate the Fed's pivot to easing.

Risks and Conclusions

The Fed's dilemma is far from resolved. If tariffs are fully implemented, a 3.1% GDP contraction could force aggressive rate cuts, supercharging bonds. Conversely, a sudden inflation spike might force hikes, penalizing long-duration assets. However, the base case—prolonged ambiguity—leans strongly in favor of fixed income.

In this environment, investors should treat bonds not as a temporary haven but as a core portfolio pillar. As Fed Chair Powell acknowledges, “later and correct” may be the mantra for central banks—and investors—alike. The Fed's purgatory is here to stay. Seize it.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet