Fed's December Rate Cut Teeters on the Edge as Divisions Deepen

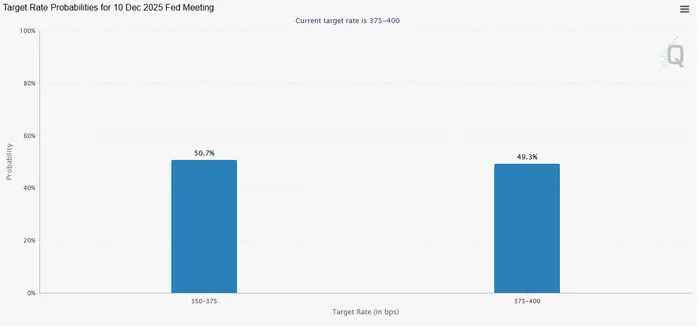

The Federal Reserve's path to another interest rate cut in December has turned from a grand slam dunk to a vague "maybe" upon the horizon, with odds dipping from more than 90% to around 50% amid vocal caution from key policymakers and a shroud of uncertainty from missing economic data.

As markets absorbed the shifting signals, Wall Street took a sharp hit on Thursday, underscoring the fragility of investor expectations in a resilient yet uneven economy. San Francisco Fed President Mary Daly, once a steadfast advocate for easing, now calls any decision "premature," while Minneapolis Fed President Neel Kashkari sits firmly on the fence, highlighting inflation still hovering around 3%—well above the Fed's 2% target.

This pivot reflects broader unease within the central bank, where initial enthusiasm for rate reductions has given way to a more guarded stance. Just weeks ago, futures markets priced in a near-certain cut; now, the probability hovers at 47%, a stark reversal that has rippled through equities and bonds alike.

Shifting Sentiments Among Fed Officials

A chorus of Fed voices has amplified doubts about further easing. Boston Fed President Susan Collins, who supported both of this year's rate cuts, set a "relatively high bar" for additional moves, citing the need for clear evidence of labor market weakness. Speaking at a bankers' conference, she emphasized that policy might need to remain on hold "for some time," especially with inflation data hampered by the recent government shutdown.

Collins' candor highlights the deepening rifts on the Federal Open Market Committee (FOMC). Fed Chair Jerome Powell had already telegraphed this tension two weeks ago, after the central bank trimmed rates to the 3.75%-4.00% range, warning that a December cut was "far from" guaranteed. The absence of fresh data, he likened to "driving in the fog"—a vivid metaphor for the caution urging policymakers to slow down.

Other officials echo this restraint. St. Louis Fed President Alberto Musalem insists monetary policy must "lean against" inflation, while Fed Vice Chair Philip Jefferson advocates proceeding slowly amid the data vacuum. Non-voters like Atlanta Fed President Raphael Bostic and Cleveland Fed President Beth Hammack have also leaned toward steady rates. Even Chicago Fed President Austan Goolsbee and Fed Governor Michael Barr could join the pause camp, according to analysts.

On the other side, a smaller faction pushes for action. Fed Governor Stephen Miran, on leave from the Trump administration's Council of Economic Advisers, dissented last month for a larger half-point cut, arguing inflation was cooling faster than recognized. Governors Michelle Bowman and Christopher Waller, both Trump appointees, continue to favor easing.

Kansas City Fed President Jeffrey Schmid, who opposed last month's cut due to persistent inflation, could lead dissents if rates are lowered again. Analysts at Evercore ISI warn that Powell's challenge in managing these divisions could lead to multiple dissents—potentially from Collins, Musalem, Schmid, and others—regardless of the outcome at the December 9-10 meeting.

Market Reactions and Fading Bets

The uncertainty has jolted financial markets. Short-term interest rate futures, the pulse of Fed expectations, have swung dramatically: from 67% odds earlier this week to around 50% now, down from over 90% just two weeks ago before Powell's surprise comments.

Stocks bore the brunt on Thursday. The Dow Jones Industrial Average plunged 797 points after touching a record high the day before, closing down about 1.7%. The S&P 500 shed 1.6%, the Nasdaq Composite dropped 2.3%, and the Russell 2000—tracking smaller firms—tumbled 2.9%. Tech stocks led the decline, with Dell Technologies falling 4.8%, Nvidia sliding 3.8%, and Palantir dropping 6.5%.

Despite the day's rout, major indices remain robust for 2025: the Dow, S&P, and Nasdaq are up double digits year-to-date, while the Russell has gained nearly 7%. But the fading rate-cut prospects have eroded some of that optimism, as investors recalibrate for a potentially hawkish Fed stance.

The Data Dilemma: Shutdown's Lingering Fog

Compounding the debate is the government shutdown's fallout, which has left critical data in limbo. The two most recent jobs reports and October's inflation figures are missing or incomplete. White House guidance suggests September's employment data might emerge post-reopening, but October's could be delayed indefinitely—and inflation metrics may never fully materialize due to uncollected inputs.

This void forces the Fed to rely on patchwork private-sector indicators, which paint a mixed picture. Payroll processor ADP reported U.S. firms shedding over 11,000 jobs weekly through late October, signaling pockets of labor market strain. Yet TLR Analytics' sales tax diffusion index shows strength, with receipts holding above 50% on a two-month average, suggesting no broad economic alarm.

Inflation data from private sources is scarcer but telling. Apollo chief economist Torsten Slok estimates that prices for 55% of Consumer Price Index items are rising faster than 3%, reinforcing arguments against hasty cuts. "This is the reason why it is difficult for the Fed to cut interest rates in December," Slok noted.

Kashkari captured the duality: some economic sectors thrive, while others, particularly in the labor market, show pressure. Daly, maintaining an open mind, awaits debate with colleagues, but her shift from supporting a third cut underscores how data gaps amplify caution.

Potential Dissents and FOMC Dynamics

The December meeting could expose the FOMC's fractures more vividly than last month's, which saw two dissents: Schmid against easing due to inflation, and Miran for a bolder cut. If rates hold steady, Miran might be joined by Waller and Bowman in protest. A cut could draw opposition from Schmid, Collins, Musalem, and possibly Goolsbee or Barr.

Evercore ISI's Krishna Guha flagged Collins' remarks as a red flag for Powell's leadership, heightening concerns over rate-path uncertainty. Fed governors Lisa Cook and Jefferson, along with Musalem and Goolsbee, have adopted cautious tones, tilting toward a pause or minimal quarter-point adjustment if any.

This internal tug-of-war reflects the Fed's dual mandate in a post-pandemic economy: taming inflation without derailing growth. With two cuts already delivered this year, the bar for a third has risen, especially as labor market stability persists despite isolated weaknesses.

Economic Indicators and Broader Implications

Private data offers no clear verdict. ADP's job cuts hint at softening, but strong sales tax receipts counterbalance that, indicating consumer resilience. Slok's inflation breakdown—over half of CPI components accelerating beyond 3%—bolsters the hold-steady camp, aligning with the Fed's 2% goal.

Looking ahead, a December pause could signal the end of the easing cycle, bolstering the dollar and pressuring risk assets further. Yet if data surprises to the downside, even reticent officials like Daly or Kashkari might pivot.

For investors, the message is clear: the Fed's once-predictable path has veered into uncharted territory. As Powell navigates this fog, markets will hang on every utterance, betting that clarity emerges before the year-end meeting. The outcome won't just shape borrowing costs—it could redefine the economic narrative for 2026.

Expert analysis on U.S. markets and macro trends, delivering clear perspectives behind major market moves.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet