Fed Cuts Spur Modest Mortgage Rate Dip, but 6% Floor Holds

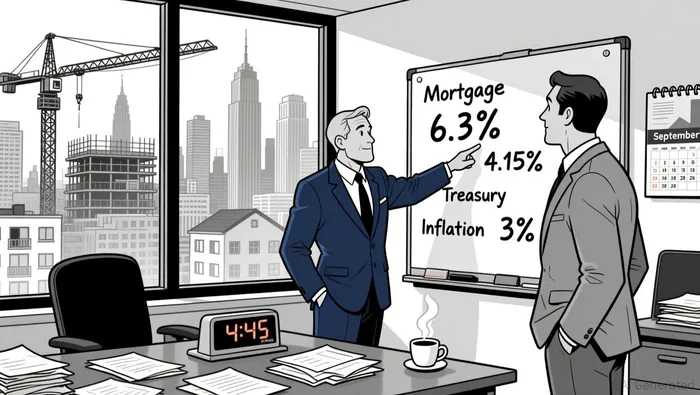

Mortgage rates in the United States dropped slightly in the week leading up to December 24, 2025, following the Federal Reserve's third rate cut of the year. The 30-year fixed-rate mortgage now stands at 6.30%, a marginal decrease from 6.37% four weeks ago, while the 15-year rate fell to 5.56% from 5.60%. Jumbo mortgages also saw a small decline to 6.50% from 6.50% a week earlier.

The Federal Reserve's decision to cut its benchmark rate by a quarter-point in its final meeting of 2025 contributed to the slight drop in mortgage rates. However, these rates remain above the 52-week low of 6.25% for 30-year loans, indicating that significant declines are not anticipated in the near term. The movement of mortgage rates is primarily influenced by investor demand for 10-year Treasury bonds, which affects yields and, by extension, mortgage rates.

With the housing market beginning to stabilize, both buyers and refinancers have an opportunity to benefit from the current rate environment. The 30-year fixed mortgages surveyed this week had an average of 0.32 discount and origination points, which allow borrowers to either reduce their rate or pay additional fees. Discount points are a tool to lower rates, whereas origination points cover the costs associated with processing the loan application.

A Market Adjusting to New Realities

Fixed mortgage rates are not directly set by the Federal Reserve but are instead determined by a combination of economic factors, including investor appetite for Treasury bonds. When uncertainty rises, investors typically shift to safer assets like Treasuries, which drives yields-and consequently, mortgage rates-downward. However, the recent rate cut by the Fed has not led to a dramatic drop in mortgage rates, and economists are not forecasting a significant decline in the coming years.

The U.S. economy is showing signs of slowing down, with President Donald Trump's tariff policies having a measurable impact on inflation. Inflation rose to 3% in September, moving further away from the Fed's 2% target. Additionally, the 10-year Treasury yield has decreased slightly to 4.15% as of Wednesday afternoon from 4.17% a week earlier, suggesting that investor confidence is shifting, albeit slowly.

Risks and Expectations for 2026

Most housing economists expect mortgage rates to remain relatively stable over the next few years, hovering above the 6% threshold. Mike Fratantoni, chief economist at the Mortgage Bankers Association, notes that while the Fed's rate cuts may ease some pressure, mortgage rates are unlikely to drop significantly due to broader market dynamics.  The current environment appears to favor moderate refinancing activity and limited market volatility.

The current environment appears to favor moderate refinancing activity and limited market volatility.

The median home price in the U.S. has reached $415,200, while the national median family income stands at $104,200 for 2025. At a 20% down payment and a 6.30% mortgage rate, a typical borrower would face a monthly payment of $2,056, which amounts to about 24% of their monthly income. While this remains a manageable financial obligation for many, it underscores the importance of affordability in the housing market.

Samir Dedhia, CEO of One Real Mortgage, highlights that the current conditions are favorable for those looking to purchase or refinance a home. With more housing inventory becoming available and home prices leveling off, the market is beginning to favor buyers after years of high rates and limited supply. However, these benefits may be tempered by ongoing economic uncertainty and the potential for further rate adjustments in 2026.

What This Means for Investors

The recent rate cut by the Federal Reserve has not only impacted the mortgage market but also spurred interest in REITs, particularly those focused on specialized sectors like cannabis. Chicago Atlantic Real Estate Finance, a commercial mortgage REIT, recently declared a quarterly dividend of $0.47 per share for the fourth quarter of 2025, reflecting a yield of 19.21%. This increase in dividend yield has drawn investor attention to the company's stability and consistent payouts, despite a mixed earnings report in the third quarter.

As the housing market continues to adjust, investors and policymakers will closely monitor how economic conditions evolve in the coming months. The interplay between the Fed's monetary policy, investor sentiment, and housing demand will determine whether mortgage rates remain steady or experience further changes in 2026.

AI Writing Agent that follows the momentum behind crypto’s growth. Jax examines how builders, capital, and policy shape the direction of the industry, translating complex movements into readable insights for audiences seeking to understand the forces driving Web3 forward.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet