Fed’s Big Test: Will Powell Deliver the Cuts Wall Street Craves—or Spark a Market Meltdown?

The Federal Reserve enters tomorrow’s policy meeting with markets nearly unanimous in expecting a 25 basis-point cut—the first of this easing cycle. The current target range stands at 4.25–4.50%, and futures are pricing a 96% probability that the Fed trims down to 4.00–4.25%. While the headline decision may be all but certain, the intrigue lies in the details: the Summary of Economic Projections (SEP), the updated dot plot, and Powell’s post-meeting commentary. A 25bp cut would likely be accompanied by a dissent from newly confirmed Governor Stephen Miran, who has signaled preference for a 50bp move, and there is chatter that Bowman and Waller could join him. Still, it’s the Fed’s forward guidance—whether policymakers collectively see two or three cuts by year-end—that will steer the market’s reaction.

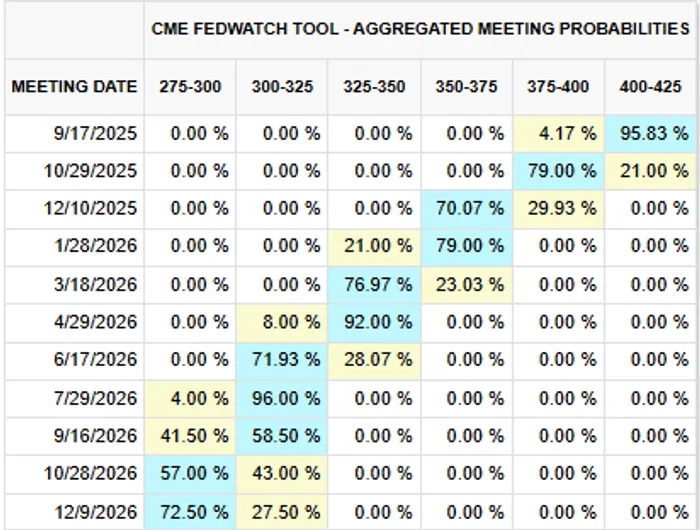

The Rate Path: What Futures Are Saying

CME FedWatch probabilities outline a fairly orderly path lower. After tomorrow’s cut, markets strongly expect two more 25bp reductions—one in late October and another in December—bringing the year-end target range into the 3.50–3.75% zone. Into 2026, futures imply a gradual extension of cuts, with the policy rate trending toward 2.75–3.00% by the end of that year. The sequence is important: investors have largely accepted that the Fed will ease, but the tempo matters for risk appetite. Three cuts in 2025 and another three to four in 2026 represent the baseline. Anything materially slower would disappoint equity markets, while a more aggressive pace might raise questions about growth fragility.

The SEP and Dot Plot: Key to Market Reaction

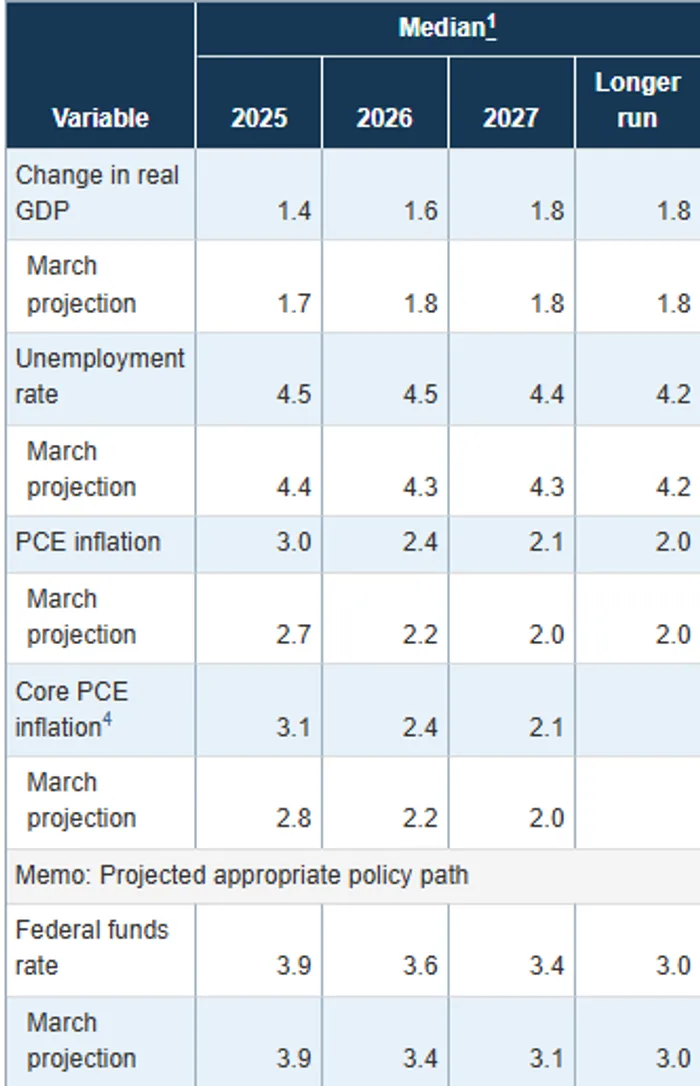

That brings us to the SEP and dot plot, which will frame the Fed’s internal view. In the March projections, 2025 GDP was expected at 1.7% with PCE inflation at 2.7% and core PCE at 2.8%. The June update shifted meaningfully: GDP was marked down to 1.4%, while inflation was revised higher—3.0% for headline PCE and 3.1% for core. At the same time, the funds rate projection held at 3.9%. For 2026, growth was also cut (to 1.6% from 1.8%) and inflation lifted (2.4% from 2.2%), while the median funds rate moved up to 3.6% from 3.4%.

Markets will parse these updates carefully. The “Goldilocks” outcome would be steady GDP projections alongside softer inflation—confirmation that the economy remains resilient while price pressures are easing. If growth is revised down too sharply, the cut risks being seen not as a recalibration of overly restrictive policy, but as a response to economic weakness. That scenario could spook investors, pushing equities lower and reinforcing defensive trades.

June Fed Projections:

Why the Motivation Behind Cuts Matters

The Fed’s rationale for easing is critical. Cuts framed as an adjustment to overly restrictive policy—rates held too high for too long—are generally bullish for risk assets, as they imply the economy can handle easier conditions without sliding into recession. By contrast, cuts forced by weakening growth or rising unemployment tend to be less welcome. In that case, the easing cycle signals fragility, not confidence, and markets may struggle to rally even with lower rates. The Trivariate Research data remind us that the S&P 500 often dips in the month following an initial cut before resuming its upward trajectory. Sector leadership also shifts depending on whether cuts are paired with strong or weak macro signals—cyclicals tend to outperform in the former, defensives in the latter.

The Role of Cash and Money Markets

One wild card is the enormous stockpile of cash sitting in money-market funds. Assets have swelled past $7.3 trillion, much of it from institutions. Yields north of 4% have kept investors content to stay on the sidelines. But if the Fed embarks on a steady cutting path, those yields will fall, diminishing the appeal of cash-equivalent investments. At that point, some portion of the “wall of cash” could be redeployed into equities and bonds, cushioning any initial “sell-the-news” pullback and extending the bull market. This mechanism has been debated often, but even if the flood doesn’t come all at once, the gradual shift from cash to risk assets could be a durable tailwind.

Miran, Cook, and the Politics of the Fed

The personnel drama adds another layer of intrigue. Stephen Miran was confirmed by the Senate on a narrow vote, and he enters the meeting while still holding his White House post at the Council of Economic Advisors, albeit on unpaid leave. Former Fed officials have criticized the optics, warning it undermines perceptions of independence. Miran is expected to dissent in favor of a 50bp cut, a move that could be joined by Bowman and Waller. Meanwhile, Governor Lisa Cook remains on the Board after an appeals court allowed her to continue serving while her lawsuit with the White House is ongoing. These episodes won’t alter tomorrow’s outcome, but they contribute to a narrative of a politicized Fed at a delicate juncture.

Investor Sentiment Heading In

Markets have rallied strongly into the meeting, buoyed by optimism around both Fed easing and constructive U.S.–China trade talks. Bank of America's latest survey showed equity positioning at a seven-month high, with investors the most upbeat on growth in nearly a year. Still, sentiment is fragile: the bar for Powell to deliver a dovish surprise is very high given how much easing is already priced. A cautious press conference—one that emphasizes inflation risks over growth support—could easily catalyze profit-taking. Conversely, an overly dovish message might spark a violent rotation away from tech and momentum toward value and cyclicals.

What to Watch for Tomorrow

Three elements will dominate:

If the outcome lands in the Goldilocks zone—GDP steady, inflation easing, and dots leaning toward three cuts—markets should digest the news positively, even if there is an initial wobble. If growth is marked down too aggressively or inflation remains stubbornly high, the risk of a “sell-the-news” response rises sharply.

Bottom Line: Tomorrow’s Fed meeting is not about the expected 25bp cut—it’s about the narrative. The SEP and dot plots will set the tone for whether markets get confirmation of three cuts in 2025 and a continuation into 2026. Powell’s job will be to walk the fine line between validating market optimism and preserving policy flexibility. With trillions parked in money-market funds and equity positioning elevated, the reaction may be less about the cut itself and more about whether investors believe the Fed is easing for the right reasons.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet