The Fed's 50-Basis-Point Cut and Its Catalytic Impact on the Refinance Wave of 2025

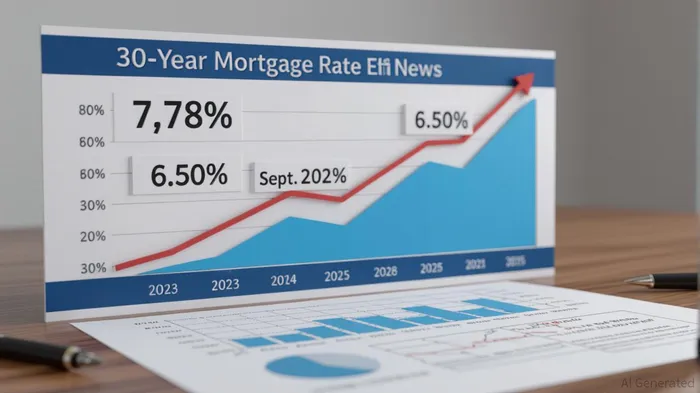

The Federal Reserve's 50-basis-point rate cut in September 2025 has ignited a seismic shift in the housing market, unlocking a refinancing surge that is reshaping liquidity dynamics and redefining opportunities in mortgage-backed securities (MBS). As mortgage rates plummeted to 6.50% by late September 2025—a 11-month low—homeowners are flocking to refinance, creating a ripple effect across real estate and financial markets. For investors, this moment represents a rare confluence of policy-driven tailwinds and structural market imbalances, offering high-conviction plays in housing liquidity and MBS.

The Mechanics of the Fed's Rate Cut and Refinancing Surge

The Fed's aggressive easing, driven by soft labor data and inflation hovering near 3.5%, has directly reduced borrowing costs. By September 2025, the 30-year fixed mortgage rate had dropped 129 basis points from its October 2023 peak of 7.79%. This decline has unlocked a refinancing frenzy: the refinance share of mortgage applications hit 47% in late August 2025, the highest since October 2024. Borrowers from the 2023–2024 vintage—many locked into rates above 7%—are now refinancing to secure savings of 50–75 basis points, with lenders reporting a 30% increase in pre-approvals for refinances.

The lag between rate cuts and housing market effects is narrowing. Historically, home price appreciation lags rate changes by 6–18 months, but the 2025 refinance wave is accelerating this timeline. With 4.2 million homeowners expected to refinance in Q4 2025 alone, liquidity is surging in the secondary mortgage market. This surge is not just a short-term blip—it's a structural reset.

Housing Market Liquidity: A Post-Rate-Cut Boon

The Fed's cuts are catalyzing a liquidity rebound in a market starved for affordability. While home prices remain elevated (median price at $435,300 in June 2025), the drop in mortgage rates is easing monthly payment burdens. For a $400,000 loan, a 75-basis-point rate reduction translates to a $1,200 monthly savings—a lifeline for households strained by 2022–2023 rate hikes.

This affordability boost is translating into increased buyer confidence. Purchase activity, though still constrained by inventory shortages, is showing early signs of stabilization. The National Association of Realtors reported a 4% increase in pending home sales in August 2025 compared to July, with urban markets seeing the most traction. For investors, this signals a transition from a “seller's market” to a more balanced one, where liquidity gains will outpace price volatility.

Mortgage-Backed Securities: A High-Conviction Play

The refinance wave is reshaping MBS performance in two key ways: prepayment risk and yield compression.

Prepayment Risk Mitigation: As refinancing accelerates, prepayment speeds for seasoned MBS are rising. By September 2025, prepayment speeds for 2023–2024 vintage loans had increased to 12% of outstanding balances, up from 6% in January 2025. While this shortens the duration of MBS holdings, it also reduces credit risk—defaults are declining as homeowners lock in lower rates. Passive investors in agency MBS (e.g., FNMA, FHLMC) are seeing improved cash flows, with spreads over 10-year Treasuries narrowing to 200 basis points (vs. 250 in October 2023).

Yield Compression and Active Strategies: The drop in mortgage rates has compressed MBS yields, but this creates opportunities for active management. Non-agency MBS with credit enhancements (e.g., CMBSCMBS-- with AAA tranches) are gaining traction as investors seek higher returns. For example, CMBS linked to multi-family housing and industrial properties—sectors with strong occupancy rates—are trading at a 15–20 basis point premium to agency MBS.

Investment Strategy: Balancing Risk and Reward

For investors, the post-rate-cut environment demands a dual approach:

Long Liquidity, Short Duration: Allocate to agency MBS with shorter durations (e.g., 5–7 years) to capture refinancing gains without overexposure to prepayment risk. These securities offer stable cash flows and are less sensitive to rate volatility.

Active Hedging in Non-Agency MBS: For higher returns, targetTGT-- non-agency MBS with defensive collateral (e.g., commercial real estate, industrial properties). Use interest rate swaps or duration-matching to hedge against further rate cuts.

Leverage Refinance Mining: Mortgage lenders and brokers should prioritize “refi mining” by identifying borrowers with 50+ basis points in savings potential. Streamlined underwriting and pre-collected documentation can accelerate approvals, capturing market share before rates stabilize.

Risks and Mitigation

While the outlook is bullish, risks persist:

- Inflation Rebound: A surge in energy prices or geopolitical tensions could reverse rate cuts. Investors should maintain a 10–15% allocation to inflation-protected securities (TIPS) as a hedge.

- Inventory Constraints: Limited resale inventory may cap home price gains. Focus on markets with strong rental demand (e.g., Austin, Phoenix) to diversify exposure.

Conclusion

The Fed's 50-basis-point cut in September 2025 is not just a policy adjustment—it's a catalyst for a refinance-driven liquidity boom. For investors, the housing market and MBS sector present high-conviction opportunities, provided strategies are tailored to balance prepayment risk and yield potential. As mortgage rates stabilize near 6.2% by early 2026, the window for capitalizing on this cycle is narrowing. The time to act is now.

Delivering real-time insights and analysis on emerging financial trends and market movements.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet