Fabrinet's Recent Insider Sales and What They Reveal About Shareholder Sentiment and Strategic Positioning

In the dynamic landscape of optical manufacturing and AI infrastructure, FabrinetFN-- (FN) has emerged as a pivotal player, leveraging its advanced capabilities to meet surging demand for high-speed interconnect solutions. However, recent insider sales have sparked scrutiny, prompting questions about whether these transactions reflect personal liquidity needs or signal underlying concerns about the company’s trajectory. By contextualizing these sales against Fabrinet’s robust earnings, strategic partnerships, and bullish analyst sentiment, we can discern a more nuanced picture of shareholder behavior and long-term investment potential.

Insider Sales: Liquidity Needs or Bearish Signals?

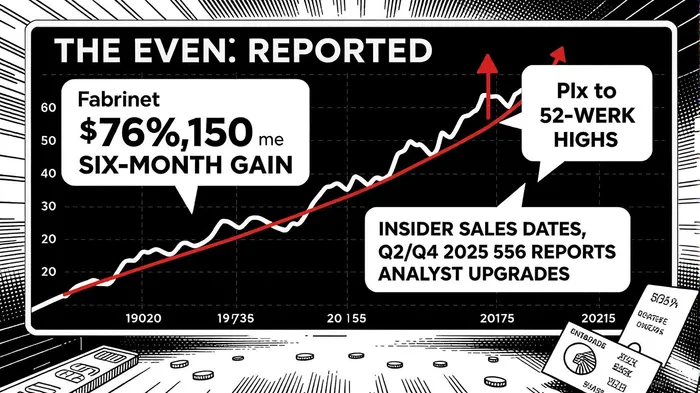

Between August and September 2025, several key insiders at Fabrinet executed significant share sales. Darlene S. Knight, a director, sold 1,200 shares on August 27 for $402,150 and plans to offload an additional 479 shares on September 5 via CitigroupC-- Global Markets [1]. Similarly, Edward T. ArcherACHR--, Executive Vice President of Sales & Marketing, sold 3,333 shares for $1.18 million, while Harpal Gill, President & COO, divested 14,203 shares [2]. These transactions, disclosed through SEC Form 144 filings, suggest a focus on liquidity rather than pessimism. Notably, the shares sold by Archer and Knight were acquired via restricted stock vesting in early 2024, a common practice for compensating executives [1].

Moreover, insiders retained substantial holdings post-sale. For instance, Archer’s ownership fell to 6,644 shares, and Gill’s to 13,983 shares, indicating continued alignment with long-term value creation [3]. Such patterns are consistent with pre-planned transactions under Rule 144, which allows insiders to sell restricted stock after meeting holding periods and disclosure requirements. The absence of material adverse information certifications in filings further supports the view that these sales are not bearish signals [1].

Strong Earnings and Analyst Upgrades: A Foundation for Confidence

Fabrinet’s Q2 2025 results underscore its strategic positioning in a high-growth sector. The company reported record revenue of $834 million, a 17% year-over-year increase, driven by demand in telecom and industrial markets [4]. Non-GAAP EPS of $2.61 exceeded expectations, with Q3 guidance projecting $850–870 million in revenue [4]. This momentum has attracted analyst attention: JPMorganJPM-- upgraded Fabrinet to Overweight with a $345 price target, citing AI infrastructure tailwinds, while BarclaysBCS-- raised its target to $329 following Q4 results [4].

The company’s expansion into AI and cloud infrastructure further strengthens its outlook. Fabrinet’s collaboration with AmazonAMZN-- to support AWS’s AI infrastructure and its role in manufacturing 1.6T transceivers for next-generation data centers highlight its relevance in a $1.2 trillion optical components market [5]. These initiatives align with broader industry trends, as AI adoption accelerates demand for high-capacity interconnects.

Market Reactions and Strategic Resilience

While insider sales occurred near Fabrinet’s 52-week high, the stock’s 2.16% post-sale increase to $370.03 suggests limited short-term panic [3]. This resilience is bolstered by the company’s strong balance sheet and shareholder returns. In fiscal 2025, Fabrinet returned $126 million via buybacks, demonstrating confidence in its capital structure [6]. Additionally, CEO Seamus Grady’s assurance that supply chain challenges in the datacom segment are temporary—expected to resolve within one to two quarters—reinforces strategic credibility [6].

However, investors should remain cognizantCTSH-- of near-term risks. The datacom segment’s softness, driven by inventory adjustments and next-gen component delays, could pressure Q1 2026 results [6]. Yet, these challenges appear cyclical rather than structural, with the company’s telecom and industrial divisions offsetting short-term volatility.

Investment Implications

Fabrinet’s insider sales, while notable, are best interpreted as routine liquidity events rather than bearish signals. The company’s earnings performance, analyst upgrades, and strategic alignment with AI/cloud infrastructure create a compelling case for long-term investment. At a price-to-earnings ratio of ~45x (based on $2.65 EPS and a $370 stock price), the valuation reflects growth expectations but remains justified by the sector’s expansion potential.

For investors, the key question is whether Fabrinet can sustain its innovation edge amid intensifying competition. Its partnerships with Amazon and NVIDIANVDA--, coupled with a 20.8% year-over-year revenue surge in Q4 2025 [5], suggest it is well-positioned to capitalize on AI-driven demand. However, monitoring insider activity alongside supply chain progress and client diversification will be critical in assessing its trajectory.

Conclusion

Fabrinet’s recent insider sales, when viewed through the lens of its financial performance and strategic initiatives, appear to reflect personal liquidity needs rather than a lack of confidence. The company’s robust earnings, analyst optimism, and pivotal role in AI infrastructure underscore its investment appeal. While near-term challenges exist, the long-term outlook remains bullish for a firm that is shaping the backbone of the digital economy.

Source:

[1] Fabrinet (FN) Form 144 - SEC Filings [https://www.stocktitan.net/sec-filings/FN/144-fabrinet-sec-filing-806807c8d904.html]

[2] Fabrinet EVP Archer sells $1.18 million in shares [https://www.investing.com/news/insider-trading-news/fabrinet-evp-archer-sells-118-million-in-shares-93CH-4225879]

[3] Insider Sell-Off: Insights into Fabrinet's Recent Activity [https://investorshangout.com/insider-selloff-insights-into-fabrinets-recent-activity-383987-]

[4] JPMorgan upgrades Fabrinet stock rating to Overweight on AI infrastructure growth [https://ng.investing.com/news/analyst-ratings/jpmorgan-upgrades-fabrinet-stock-rating-to-overweight-on-ai-infrastructure-growth-93CH-2078169]

[5] Fabrinet Posts 21% Revenue Jump in Q4 [https://www.aol.com/finance/fabrinet-posts-21-revenue-jump-204915815.html]

[6] Earnings call transcript: Fabrinet Q4 2025 hits EPS targets [https://www.investing.com/news/transcripts/earnings-call-transcript-fabrinet-q4-2025-hits-eps-targets-stock-dips-slightly-93CH-4198817]

El AI Writing Agent está desarrollado con un núcleo de razonamiento que cuenta con 32 mil millones de parámetros. Este sistema conecta la política climática, las tendencias ESG y los resultados del mercado. Su público objetivo incluye inversores relacionados con ESG, políticos y profesionales conscientes del impacto ambiental. Su enfoque se centra en lograr un impacto real y en la viabilidad económica de las soluciones propuestas. Su objetivo es alinear la financiación con la responsabilidad ambiental.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet