Expanding Wafer Fab Equipment Spending Aids KLAC: What's Ahead?

KLA KLAC is benefiting from strong spending in the Wafer Fabrication Equipment (“WFE”) market. The company expects the WFE market to grow from about $110 billion in 2025 to the mid-$130 billion range in 2026. The growth is driven by increasing demand for AI chips, advanced logic chips and memory such as DRAM.

Higher WFE spending will benefit the company’s Semiconductor Process Control segment, which accounted for 91.1% of second-quarter fiscal 2026 revenues. The segment sees higher demand for KLAC’s semiconductor manufacturing tools that are used inside wafer fabrication facilities. These tools include systems for rigorous defect inspection to detect wafer defects, metrology tools that measure tiny features during chip manufacturing and yield optimization solutions.

As demand for AI chips grows exponentially, semiconductor manufacturers are spending more on WFE equipment, which increases demand for KLA’s process-control tools. WFE demand is supported by multiple growth vectors like Foundry/Logic, Memory, Advanced Packaging and Services, which drive demand for KLAKLAC-- tools, as these growth areas are directly linked to global WFE spending trends.

In calendar 2025, KLA generated total systems revenues of $950 million, which jumped 70% year over year, primarily driven by advanced packaging revenue growth and market share gains. KLACKLAC-- expects this momentum to continue in calendar 2026, with a year-over-year growth rate in the mid-to-high teens, driven by strong growth in process control products. Strong investments in WFE and advanced packaging represent a growth opportunity for the company. Growth in advanced packaging, supporting heterogeneous chip integration, has become a new market for KLA, which is currently worth $11 billion and expanding faster than core WFE.

KLA now expects third-quarter fiscal 2026 revenues of $3.35 billion (+/- $150 million), reflecting a modestly weak product mix on a sequential basis. The guidance reflects the rapidly escalating cost of DRAM chips used in KLA’s image processing computers that ship with its systems, hurting gross margin. Increasing lead times due to supply constraints and the negative tariff impact of roughly 100 bps are near-term headwinds. The Zacks Consensus Estimate for third-quarter fiscal 2026 revenues is currently pegged at $3.38 billion, suggesting 10.5% growth from the figure reported in the year-ago quarter.

Tough Competition Hurts KLAC’s Prospects

KLAC is facing stiff competition from the likes of ASML ASML and Applied Materials AMAT, both of which are well known for their process control offerings.

Sustained demand for AI and HPC chips from global data centers, AI labs and hyperscalers reinforces ASML’s long-term growth outlook, as the company provides extreme ultraviolet (EUV) semiconductor lithography tools to chip manufacturers that enable capacity expansion. ASML benefits from a growing installed base, which drives high-margin service and upgrade revenues, as customers increasingly view upgrades as the fastest way to add capacity.

Applied Materials is at the forefront of AI-driven semiconductor innovations. It is a major manufacturer of semiconductor fabrication equipment, covering deposition, etching and inspection, serving the most crucial stages of chip manufacturing. AMAT expects its leading-edge foundry, logic, DRAM and high-bandwidth memory (HBM) to be the fastest-growing wafer fabrication equipment businesses in 2026.

KLAC’s Share Price Performance, Valuation & Estimates

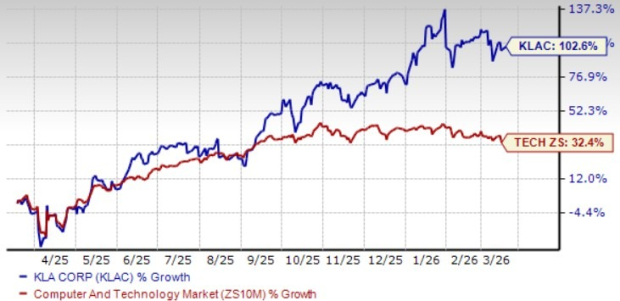

KLAC shares have jumped 102.6% on a trailing 12-month basis, outperforming the broader Zacks Computer and Technology sector’s growth of 32.4%

KLAC Stock’s Performance

KLA stock is overvalued, with a forward 12-month price/sales of 12.31X compared with the broader sector’s 6.02X. KLAC has a Value Score of F.

KLAC Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $36.62 per share, up 0.11% over the past 30 days, suggesting 10% growth from the figure reported in fiscal 2025.

KLA currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

See Our Newest 5 Stocks Set to Double Picks >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

KLA Corporation (KLAC): Free Stock Analysis Report

ASML Holding N.V. (ASML): Free Stock Analysis Report

Applied Materials, Inc. (AMAT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet