Exit Before the Crescendo: Why Burry Might Be Closing Scion Now

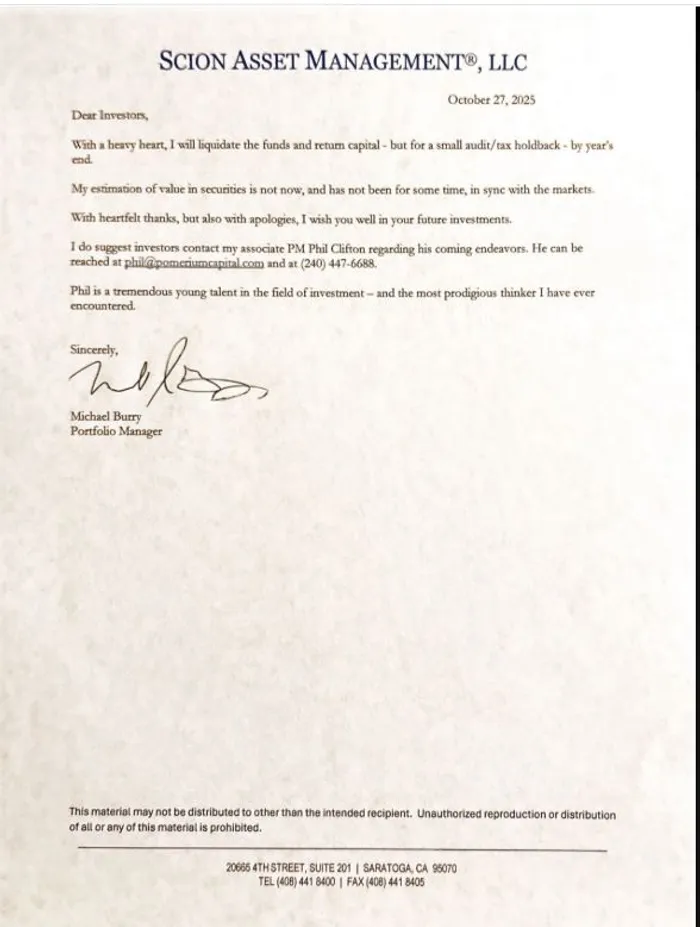

Michael Burry’s reported liquidation letter reads less like a retirement note and more like a macro call. The core line “My estimation of value in securities is not now, and has not been for some time, in sync with the markets” isn’t fatigue; it’s a valuation stalemate. For a fundamental, cash-flow-first investor, that mismatch isn’t workable inside a benchmarked fund structure. If you believe price and value have decisively parted ways, the rational move is to step off the treadmill not keep jogging and hope mean reversion rescues the quarterly tape.

The Accounting Edge: Depreciation as the Quiet EPS Engine

Burry’s thread on depreciation targets the AI supply chain’s profit optics. The claim: hyperscalers—think MSFTMSFT--, AMZNAMZN--, GOOGGOOG--, METAMETA--, ORCL—are boosting near-term earnings by extending the “useful lives” of servers and GPU clusters that, in economic reality, churn on a 2–3 year innovation cycle. When you lengthen asset lives in the accounting model, you shrink today’s depreciation expense. Lower depreciation → higher reported operating income → a cleaner EPS print. If those EPS levels are flattered by 20–30% versus a stricter schedule, then multiples atop those EPS are, in effect, paying a premium on already-elevated numbers. That’s a double-stacked optimism bet.

The “Me Then, Me Now” Frame

Burry’s meme then (subprime), now (AI infra) isn’t about identical mechanics; it’s about rhyme. In 2005, he saw investment-grade wrappers on weak collateral. In 2025, he sees trillion-dollar caps built on aggressive capex cycles and accounting choices that push costs forward. The timeline matters: if depreciation schedules revert closer to economic reality in 2026–2028 while AI growth normalizes, earnings growth could downshift or turn negative just as narratives cool. That’s how you get multiple compression right when fundamental momentum fades.

Why Shut Down Now?

Late-cycle dynamics often feature a euphoric last leg the “echo” rally where non-fundamental flows (passive, options, momentum) keep leaders levitating longer than valuation purists can tolerate. If Burry expects the eventual break to hit the same mega-caps that dominate indices, staying in a commingled, benchmark-sensitive vehicle becomes a career-risk trap: you either hug the index you’re skeptical of, or you fight it and bleed tracking error until clients capitulate. Closing Scion does three things:

1) Removes the benchmark/LP redemption pressure that punishes patience.

2) Lets him sit in cash or short selectively without quarterly diplomacy.

3) Sends a fiduciary message: “If I think the printed earnings power is overstated, I won’t park your money there on hope.”

What Could Prove Him Right (or Wrong)

Bear Case (Burry’s lane):

Earnings quality fades: Depreciation re-tightens just as AI workload growth normalizes, compressing margins.

Capex payback stretches: Monetization lags massive data-center spend, exposing ROIC gaps.

Flow reversal risk: If leaders weaken, passive and factor flows mechanically sell, turning a trickle into a downdraft.

Bull Case (the crowd’s lane):

Utilization catches up: AI workloads scale faster than feared; high fixed costs turn into operating leverage.

New revenue layers: Model hosting, inference tolls, and AI-native software/services lift durable free cash flow.

Accounting is transparent: Even with longer asset lives, disclosures and cash metrics (FCF/ROIC) remain robust.

How Investors Can Navigate the Debate

Focus on cash, not just EPS. Track free cash flow, capex intensity, and returns on incremental invested capital. If EPS is rising while FCF per share lags, scrutinize working capital and depreciation policies.

Watch asset-life assumptions. Any reversion in server/GPU useful lives will show up in depreciation lines—an early tell for EPS pressure.

Stress-test multiples. Apply one-turn and two-turn multiple compression scenarios to AI leaders and observe index-level sensitivity. Leaders are the market position sizing should reflect that concentration risk.

Diversify growth channels. Balance mega-cap AI exposure with cash-generative cyclicals, small/mid quality, or factors (quality/low-vol) that historically cushion drawdowns when leadership stalls.

Mind the timeline. If the crux is 2026–2028, interim upside squeezes are very possible. Hedging (put spreads, collars) may be more rational than outright exits for tax-sensitive investors.

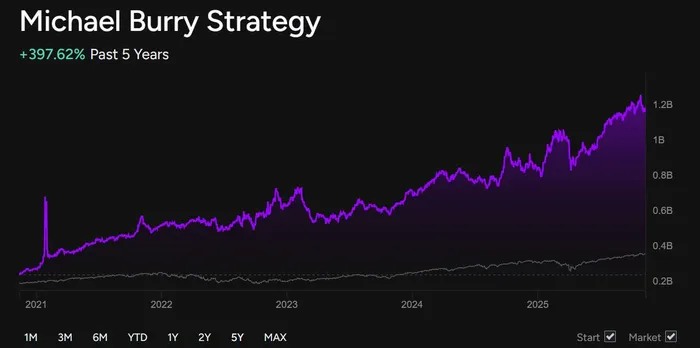

Just for fun, his returns and performance was looking good so we can rule out at least any performance based closure.

The Michael Burry Strategy attempts to mirror the portfolio of Michael Burry's Scion Asset Management using 13F filings and is rebalanced when new filings are reported. Source: quiverquant

Bottom Line

Burry’s exit looks like a philosophical risk-control move in a market he sees as late-cycle and earnings-inflated. Whether he’s early or right, the takeaway for retail investors is the same: separate story EPS from cash economics, pressure-test what you own under stricter depreciation, and size risk as if the leaders you love are also the index you carry.

This article is for informational purposes only and is not investment advice.

Market Radar delivers concise, daily trading ideas by tracking everything from options activity and market sentiment to high-profile political trades.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet