European ADRs: Navigating Volatility to Unlock Strategic Entry Points

The European ADR market has been a rollercoaster in 2025, swinging between optimism and panic as macroeconomic forces, trade policy shifts, and geopolitical tensions collide. For investors, this volatility has created both risks and opportunities. Let's break down the numbers and identify where to position for the next leg of this journey.

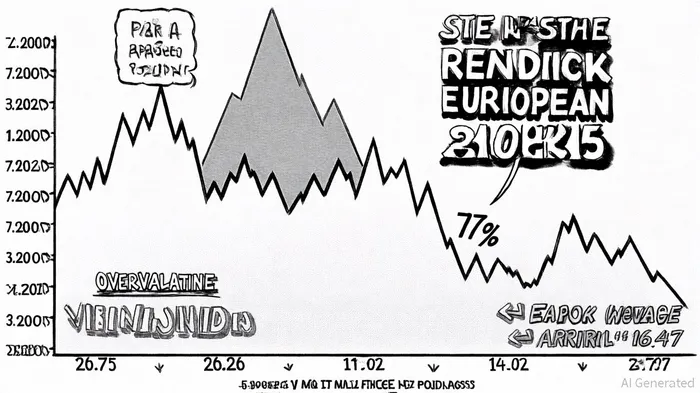

The Valuation Tightrope

As of September 5, 2025, the MSCIMSCI-- Europe index trades at a P/E ratio of 16.76, which is 19% above its five-year average of 14.02 [2]. This overvaluation is stark when viewed through a long-term lens, but the 1Y average of 16.47 suggests the market is currently in a “fair” range [2]. The disconnect between short- and long-term metrics reflects the market's struggle to price in both near-term fiscal stimulus and enduring structural challenges.

The sharp revaluation since early 2025—driven by German and EU fiscal spending, lower energy prices, and hopes for a Ukraine ceasefire—has been followed by a 17% correction from March highs [4]. While the U.S. paused some “reciprocal” tariffs in April, the broader trade uncertainty remains a headwind. Yet, this volatility has brought the forward P/E for MSCI Europe down to 12.6x, slightly below its 20-year average of 13.0x [4]. This suggests the market has already priced in a higher risk of recession, creating a potential inflection point for value hunters.

Sector-Specific Opportunities

While the broader market remains mixed, certain sectors and individual ADRs stand out as undervalued or resilient.

Defense and Aerospace: A Tailwind-Driven Sector

The Select Stoxx Europe Aerospace & Defense ETF (EUAD) has surged 73% year-to-date, outperforming the broader market [4]. This is no accident: European defense budgets are expanding in response to geopolitical tensions, and companies like Rheinmetall AG (XTRA:RHM) are trading at a 51% discount to their fair value estimate of €3,794.92 [5]. Despite a Q2 net loss, the firm is projected to grow earnings by 51.7% annually over the next three years [5].Healthcare and Infrastructure: Resilience Amid Trade Barriers

European healthcare ADRs face headwinds from Chinese import restrictions on medical devices [4], but this sector's long-term fundamentals remain intact. Similarly, infrastructure plays—such as Obrascón Huarte Lain (BME:OHLA), trading 26% below its fair value—benefit from EU green energy and digitalization spending [5].Energy and Mining: Cyclical Risks and Rewards

Energy ADRs have been hit by OPEC+ output adjustments and downward production guidance from majors [4]. However, this sector's low P/B ratios and EV/EBITDA multiples (often below 8x) suggest potential for mean reversion if oil prices stabilize [6].

Strategic Entry Points: What to Watch

For investors seeking tactical entry points, the key is to focus on companies with strong cash flow, low debt, and exposure to structural growth trends.

- LINK Mobility Group Holding ASA (OB:LINK) trades at NOK 32.8, a 46% discount to its fair value of NOK 60.99 [5]. Despite a Q2 loss, its M&A activity and debt refinancing efforts position it for 59% annual earnings growth.

- Synektik Spólka Akcyjna (WSE:SNT) is another standout, trading at PLN 231 versus a fair value of PLN 330.77 [5]. Its Q3 net income grew by 42% year-over-year, signaling operational strength.

- Truecaller (OM:TRUE B) offers a 49.3% discount to its fair value of SEK 85.35 [5], driven by its dominance in telecom services and expanding AI-driven offerings.

The Bottom Line

European ADRs are at a crossroads. The overvaluation in the broader market masks pockets of opportunity, particularly in defense, healthcare, and infrastructure. While trade policy risks and inflationary pressures linger, the current discount to fair value for select ADRs—combined with the EU's fiscal stimulus—creates a compelling case for strategic entry.

As always, investors should balance these opportunities with a disciplined approach to risk. Use the volatility to your advantage, but don't chase the noise. The best plays are those with strong fundamentals and a clear path to earnings growth—regardless of the headlines.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet