The EU's Floating Price Cap: A New Era for Oil Markets and Investment Playbook

The European Commission's shift to a dynamic 15% discount mechanism for Russian crude oil marks a pivotal moment in global energy markets. By replacing the static $60-per-barrel cap, the EU aims to recalibrate geopolitical leverage while reshaping oil pricing benchmarks. For investors, this move presents a labyrinth of opportunities—from refining sector arbitrage to upstream supply diversification—alongside risks tied to Russian retaliation and supply chain fragility. Let's dissect the implications.

The Pricing Mechanism: A Shakeup for Traditional Benchmarks

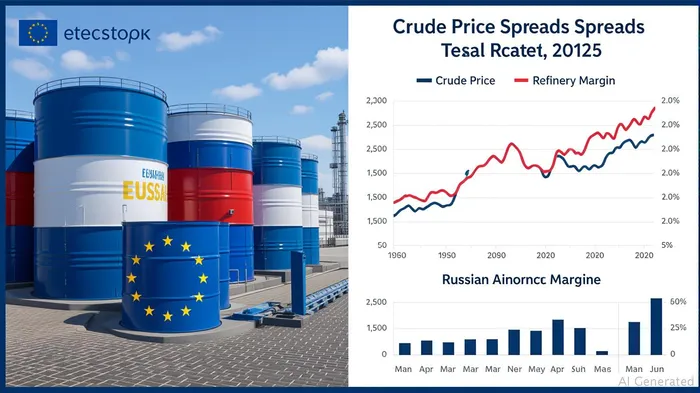

The 15% discount to Brent/Urals averages introduces volatility into a market long anchored by static price ceilings. The cap's quarterly recalibration creates a moving target, forcing traders to navigate tighter margins. Consider this: if Brent averages $70/barrel, the Russian crude cap drops to $59.50—a price point that could undercut Middle Eastern and U.S. shale exports, depending on regional demand.

The chart above reveals how the old $60 cap became obsolete as Urals prices fell below it in late 2024. The new mechanism, however, ensures the cap remains below market rates, squeezing Russian revenue while keeping its oil competitive for buyers in Asia and beyond. For investors, this creates a price discovery game: tracking regional crude differentials (e.g., Urals vs. WTI) will be critical to identifying arbitrage opportunities.

Geopolitical Risks: A Double-Edged Sword

The EU's unilateral push faces two existential threats. First, compliance gaps: Russia could reroute exports to non-G7 buyers like India or Turkey, where the cap holds no jurisdiction. Second, retaliation: Moscow's potential to slash output or weaponize energy supplies (e.g., gas cutoffs to Eastern Europe) could spike global prices, benefiting Russian exporters despite the cap.

This data highlights a shift: Asian exports surged 30% in 2024 as European imports fell. The EU's success hinges on enforcing insurance sanctions—a tool that's already proven leaky. Investors should brace for volatility in European gas prices (TTF benchmark) and crude spreads if Russia retaliates.

Sector-Specific Winners and Losers

Refining Sector: The Clear Upside

European refiners stand to profit from discounted Russian crude. Companies like ENI (NYSE: E) and TotalEnergies (NYSE: TTE) can buy Urals at a discount while selling refined products (gasoline, diesel) at global prices, boosting margins.

The chart shows refining stocks underperforming during periods of crude price spikes but outperforming when spreads widen. With the cap ensuring a persistent discount, this dynamic could favor downstream players.

Upstream Risks: Navigating the New Landscape

Oil majors exposed to Russian assets (e.g., BP's legacy ties) face reputational and regulatory headwinds. Meanwhile, producers in the Middle East and U.S. shale (e.g., Devon Energy (NYSE: DVN)) may see reduced demand if Russian crude remains price-competitive.

The inverse correlation here suggests U.S. producers could scale back drilling if Russian crude undermines WTIWTI-- prices. Investors in shale may need to pair long positions with hedges against global supply surpluses.

Investment Playbook: Positioning for the New Reality

- Buy Refining Exposure: Overweight European refining stocks (ENI, TotalEnergiesTTE--, Wintershall Dea (OTC: WSHAF)) as spreads widen.

- Short Russian-Linked ETFs: Consider inverse ETFs tied to Russian equities (e.g., RSX) if geopolitical tensions escalate.

- Diversify into Alternative Suppliers: Invest in Middle Eastern state-owned firms (via sovereign wealth funds) or U.S. midstream infrastructure (e.g., Enterprise Products Partners (NYSE: EPD)).

- Monitor Geopolitical Sentiment: Use VIX volatility indices as a proxy for risk—spikes may signal Russian retaliation or supply disruptions.

The Bottom Line

The EU's floating cap isn't just a sanctions tool—it's a catalyst for reshaping global energy economics. While geopolitical risks loom, the mechanism creates a structured framework for arbitrage and sector rotation. Investors who align their portfolios with the cap's dynamics—tracking crude differentials, refining margins, and supply chain resilience—will thrive in this new paradigm. The question remains: Can the EU enforce its rules tightly enough to outmaneuver Moscow's agility? The answer will define both market volatility and investment returns in 2025 and beyond.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet