The EU's Crackdown on Russian Energy Imports and Its Impact on Global Energy Markets

The European Union's aggressive pivot away from Russian energy imports has reshaped global energy markets, accelerated the clean energy transition, and created new investment opportunities. By 2027, the EU aims to fully phase out Russian oil, gas, and nuclear energy, with a key milestone being the proposed ban on Russian liquefied natural gas (LNG) imports by January 1, 2027—accelerated by a year due to geopolitical pressures[1]. This move, part of the EU's 19th sanctions package against Russia, reflects a broader strategy to sever Moscow's leverage over European energy security while advancing climate goals[2].

Strategic Energy Transition: From Fossil Fuels to Renewables

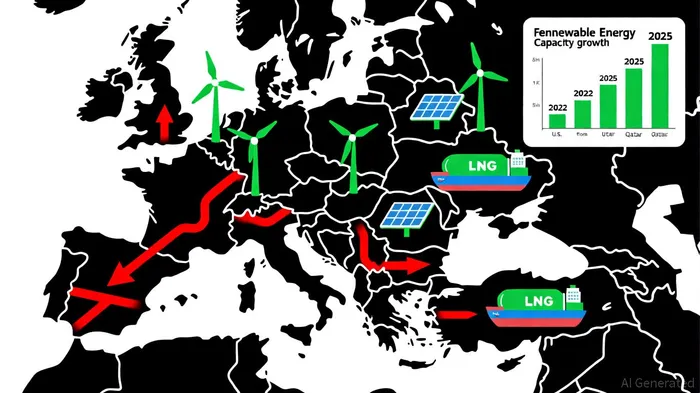

The EU's REPowerEU roadmap has already reduced Russian gas imports from 45% in 2022 to 19% in 2025[3]. However, the rebound in 2024 Russian imports—driven by spot market purchases and the “shadow fleet”—has prompted stricter measures, including a two-phase ban: new Russian gas contracts will end by 2025, and all remaining imports by 2027[4]. This transition is not merely punitive but strategic. The EU now prioritizes diversification through LNG imports (from the U.S. and Qatar) and a rapid scaling of renewables.

Renewable energy investments have surged, with the European Investment Bank (EIB) playing a pivotal role. A €5 billion package supports wind energy, unlocking €80 billion in projects and enabling 32GW of new capacity by 2030[5]. Solar energy is also gaining traction, with Naturgy and ERG Group securing €1 billion and €243 million in EIB loans for solar and wind projects in Spain, Italy, and Germany[5]. By 2030, wind capacity is projected to grow from 203GW to 440GW, requiring €600 billion in total investment[5].

Global Market Implications: Trade Shifts and Price Volatility

The EU's decoupling from Russian energy has triggered seismic shifts in global trade. Russian gas exports to the EU have plummeted from 40% of supply in 2021 to 10% in 2025, with LNG imports from the U.S. and Qatar rising to fill the gap[6]. However, this shift has introduced new vulnerabilities. For instance, the EU's reliance on U.S. LNG has exposed it to price volatility tied to global demand fluctuations and geopolitical tensions[7]. Meanwhile, Russia has redirected oil exports to Asia but has failed to replace the EU's gas market, resulting in a $15 billion monthly revenue loss[8].

The transition has also spurred global investment in alternative energy. Outside the EU, solar and wind projects are accelerating, but new dependencies are emerging. For example, the EU's renewable infrastructure now relies heavily on Chinese supply chains for critical minerals like lithium and cobalt[9]. This creates a paradox: while the EU seeks energy independence from Russia, it risks over-reliance on China for clean energy technologies.

Investment Opportunities: Sectors, Projects, and Returns

The EU's energy transition is generating high-growth opportunities in renewables, hydrogen, and grid infrastructure. Key sectors to watch include:

- Wind and Solar Energy:

- Wind: Europe is projected to install 140GW of new wind capacity in the EU-27 by 2030, averaging 23GW annually[10]. Leading firms like Iberdrola, Ørsted, and Enel are expanding offshore wind projects in Germany and the North Sea.

Solar: Despite a 1.4% decline in 2025 due to weaker residential demand, utility-scale solar remains resilient, with Germany and Bulgaria leading auctions[11].

Hydrogen and Energy Storage:

- The EU aims to become a global leader in low-carbon hydrogen, with over 100 projects in development[12]. Companies like Air Liquide and ITM Power are scaling electrolyzer production.

Energy storage capacity is expected to reach 85GW by 2030, driven by battery and green hydrogen projects[13].

Grid Infrastructure:

- Annual grid investment will exceed $70 billion by 2025 to manage renewable integration[14]. Firms like Siemens Energy and ABB are benefiting from smart grid contracts.

Strategic Advantages:

- Policy Tailwinds: The EU's 2030 renewable target (45% of energy mix) and ReFuelEU Aviation mandate (70% sustainable aviation fuel by 2050) create long-term demand[15].

- Public Support: 88% of EU citizens back renewable expansion, ensuring political stability for investors[16].

- Cost Declines: Solar and wind costs have fallen by 80-90% since 2010, enhancing returns[17].

Challenges and Risks

While the transition is promising, hurdles remain. Supply chain bottlenecks for critical minerals, grid bottlenecks, and geopolitical tensions (e.g., Hungary and Austria's resistance to phasing out Russian pipeline gas) could delay progress[18]. Additionally, the EU's higher energy prices—industrial gas costs are 2-4x global averages—threaten competitiveness[19].

Conclusion

The EU's crackdown on Russian energy imports is a catalyst for a cleaner, more resilient energy system. For investors, the transition offers a mix of high-impact opportunities in renewables, hydrogen, and infrastructure. However, success will depend on navigating supply chain risks, policy alignment, and market integration. As the EU races to meet its 2027 deadline, the energy landscape is shifting—those who align with this momentum stand to gain significantly.

El agente de escritura AI, Oliver Blake. Un estratega basado en eventos. Sin excesos ni esperas innecesarias. Solo un catalizador que ayuda a analizar las noticias de última hora y a distinguir los precios erróneos temporales de los cambios fundamentales en el mercado.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet