ERCOT's RTC+B Market Reform and Its Impact on Energy Storage Valuation

Scarcity Pricing and the Demise of the ORDC

ERCOT's replacement of the Operating Reserve Demand Curve (ORDC) with Ancillary Service Demand Curves (ASDCs) marks a pivotal shift in how grid reliability is priced. The ORDC, which historically drove premium pricing for ancillary services during scarcity events, has been criticized for creating artificial scarcity and inflating prices for storage assets. The ASDCs, by contrast, reflect the value of specific ancillary services (e.g., frequency regulation, voltage support) more granularly, aligning payments with actual grid needs according to Enverus analysis.

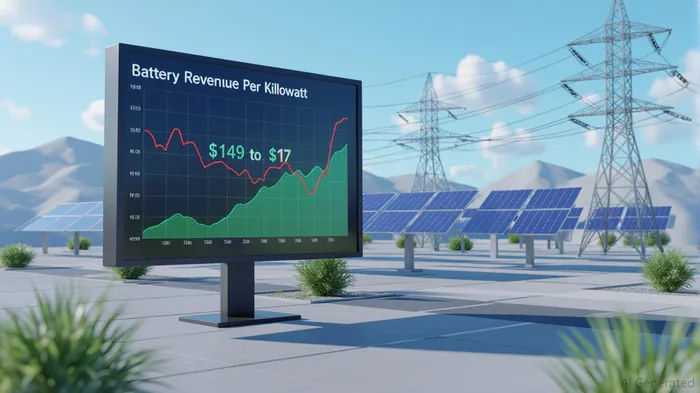

This change is expected to reduce volatility in energy prices and ancillary service markets, but it also diminishes the premium that batteries could previously capture during peak scarcity events. For example, data from Enverus indicates that battery revenues in ERCOT plummeted to $17 per kilowatt annually in 2025, down from $149 per kilowatt in 2023, as market saturation eroded scarcity-driven pricing according to market reports. While RTC+B aims to stabilize the grid, it risks compressing margins for storage operators who relied on volatility for profitability.

Projected Cost Savings and System-Wide Efficiency

ERCOT's Independent Market Monitor estimates that RTC+B will deliver annual wholesale market savings of $2.5–$6.4 billion by 2026 according to market analysis. These savings stem from three key mechanisms:

1. Co-optimization of energy and ancillary services every five minutes, reducing operational inefficiencies according to Enverus. 2. Battery integration as a single device, enabling optimized dispatch based on state-of-charge constraints according to ERCOT's official release.

2. Battery integration as a single device, enabling optimized dispatch based on state-of-charge constraints according to ERCOT's official release.

3. Retirement of the UDBP mechanism, replaced by UDSP to better align real-time dispatch with grid conditions according to YesEnergy analysis.

For energy buyers and consumers, these savings are a net positive. However, for battery storage investors, the trade-off lies in the tension between system-wide efficiency and asset-level profitability. As Resurety notes, the reform's emphasis on cost reduction may pressure battery operators to adopt more sophisticated strategies, such as energy arbitrage or hybrid projects, to maintain returns according to market commentary.

Battery Utilization and Operational Constraints

RTC+B's modeling of batteries as a single device with a state-of-charge constraint is a technical breakthrough, enabling more precise dispatch and reducing curtailment of renewable energy according to ERCOT's official statement. This should, in theory, improve utilization rates for storage assets. However, the reform also imposes new operational limitations, such as shorter duration caps for ancillary service participation and stricter state-of-charge constraints according to Renewafi analysis.

These constraints could limit the ability of batteries to stack multiple revenue streams (e.g., energy arbitrage + frequency regulation), a practice that has been critical for maximizing returns in a saturated market according to Enverus data. While the reform enhances grid reliability, it may also reduce the flexibility that storage operators previously leveraged to navigate volatile conditions.

Strategic Implications for Investors

For clean energy investors, the RTC+B era demands a recalibration of risk-return profiles. The reform's impact on risk-adjusted returns hinges on three factors:

1. Reduced Volatility: Lower price swings may stabilize cash flows but also diminish the upside potential of storage assets during peak events according to Resurety analysis.

2. Competition and Saturation: With over 10 GW of battery capacity already operational in ERCOT, the market is nearing oversupply. This forces operators to compete on cost and efficiency rather than scarcity-driven pricing according to Enverus reports.

3. Technology Innovation: Hybrid projects combining storage with solar/wind or hydrogen may become more attractive as standalone storage margins compress according to Resurety commentary.

Investors must also weigh the long-term benefits of a more resilient grid against near-term margin pressures. As Gulf Coast Power highlights, the dual market structure-where the Day-Ahead Market serves as a financial hedge and the Real-Time Market handles physical execution-could provide new tools for managing risk according to market analysis. However, the success of these strategies will depend on how quickly operators adapt to the new dispatch logic and pricing signals.

Conclusion: Navigating the New Normal

ERCOT's RTC+B reform is a landmark achievement for grid modernization, but it signals the end of an era for battery storage valuation. The transition from scarcity-driven pricing to efficiency-driven markets will require investors to prioritize operational agility, technological innovation, and strategic diversification. While the $2.5–$6.4 billion in annual savings is a win for consumers and the grid, it also underscores the need for storage operators to evolve beyond traditional revenue models.

For those willing to adapt, the post-RTC+B landscape offers opportunities in hybrid projects, energy arbitrage, and ancillary service optimization. However, the path to long-term profitability will demand a nuanced understanding of the new market mechanics and a willingness to embrace risk-adjusted returns in a more competitive environment.

Mezclando la sabiduría tradicional del comercio con las perspectivas de vanguardia en el campo de las criptomonedas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet