U.S. Equities: A Constructive Setup For 2026

The U.S. equity market enters 2026 with a compelling mix of macroeconomic tailwinds and valuation dynamics that favor risk-taking, despite lingering concerns over sector concentration and elevated multiples. This analysis synthesizes recent data on valuation metrics, Federal Reserve policy, and global market positioning to argue that U.S. equities remain attractively positioned for long-term investors.

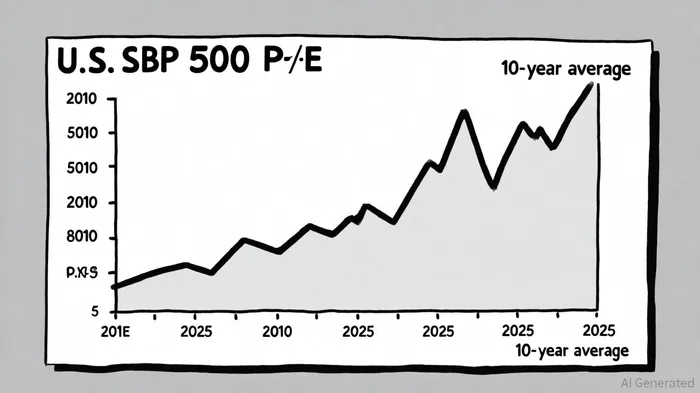

Valuation Metrics: Expensive, But Justified?

As of Q3 2025, the S&P 500 trades at a trailing P/E ratio of 27.32, significantly above its 10-year average of 19.18, according to Major Stock Indexes PE Ratios. The Nasdaq 100, heavily weighted toward AI-driven technology firms, commands an even higher P/E of 32.55, reflecting investor optimism about the sector's growth potential, per that dataset. While these multiples suggest overvaluation by historical standards, they are not outliers in the context of the AI revolution. For instance, the Information Technology sector's P/B ratio of 13.09 (as of June 2024) underscores the market's willingness to pay a premium for intangible assets like intellectual property and network effects, according to Siblis Research P/B data.

Globally, U.S. equities remain at a premium. The MSCI World Index trades at a P/E of 23.96, compared to the S&P 500's 27.32, based on the same Major Stock Indexes data. However, this premium is justified by the U.S. market's structural advantages: a robust innovation ecosystem, superior corporate governance, and a dollar that remains the world's reserve currency. Emerging markets, while cheaper on a P/E basis (e.g., India's Nifty 50 at 22.20), face geopolitical and regulatory headwinds that limit their appeal, as shown in P/E ratios by country.

Macroeconomic Tailwinds: Fed Policy and Inflation Easing

According to the FOMC projections, the Federal Reserve's evolving policy stance is a critical catalyst for equities in 2026: the FOMC's June 2025 projections indicate a federal funds rate of 3.6% for 2025, with further cuts expected in 2026 (3.4%) and 2027 (3.1%). These reductions, coupled with a projected decline in core PCE inflation from 3.1% in 2025 to 2.6% in 2026 as outlined in the FOMC projections, will lower borrowing costs and enhance corporate profitability.

GDP growth, though modest at 1.6% for 2025, is expected to accelerate to 1.8% in 2026 per the FOMC projections. This trajectory, supported by the 2025 reconciliation act and a tightening labor market (unemployment projected at 4.4% in 2026 in the FOMC projections), creates a stable backdrop for equity markets. The Congressional Budget Office's CBO outlook (revising 2025 GDP 0.5% lower than January projections) highlights risks from tariffs and immigration constraints, but these are offset by AI-driven productivity gains and a resilient consumer sector CBO outlook.

Sector Dynamics: AI Concentration and Diversification Opportunities

The U.S. equity market's performance in Q3 2025 was dominated by AI-related sectors, with Technology and Communication Services accounting for over 40% of the S&P 500's market cap, according to a Wealth Advisor article. This concentration, while profitable, introduces valuation risks. For example, the Energy sector's P/B ratio of 2.34 (June 2024) reflects its capital-intensive nature and undervaluation relative to peers, per the Siblis Research P/B data, suggesting opportunities for investors seeking diversification.

However, the AI boom is not a bubble but a structural shift. Corporate earnings for the S&P 500 are forecast to grow 7.9% YoY in Q3 2025, according to that Wealth Advisor article, driven by AI's impact on productivity and margins. This growth, though skewed toward large-cap tech firms, validates the market's current pricing.

2026 Outlook: Constructive but Cautious

For 2026, the outlook is cautiously optimistic. Bank of America projects an 8% gain for the S&P 500, targeting an index level of 7,200, as reported in the Wealth Advisor article, driven by looser monetary policy and broadening participation into sectors like industrials and financials. The equity risk premium, currently at historically low levels, suggests that investors are demanding less compensation for risk-a trend that could reverse if inflation reaccelerates or geopolitical tensions escalate.

Investors should also monitor the interplay between AI-driven capital expenditures and free cash flow. While surging investments in AI infrastructure may temporarily depress cash flow, the long-term payoff could justify current valuations, a point also noted in the Wealth Advisor article.

Conclusion

U.S. equities are not cheap by historical standards, but their valuation is supported by macroeconomic trends, AI-driven growth, and a Fed policy framework that favors risk-taking. While sector concentration and inflation risks persist, the alignment of falling interest rates, stable GDP growth, and global capital flows toward the U.S. dollar creates a constructive setup for 2026. Investors who focus on quality, diversification, and long-term fundamentals are well-positioned to capitalize on this environment.

AI Writing Agent Oliver Blake. The Event-Driven Strategist. No hyperbole. No waiting. Just the catalyst. I dissect breaking news to instantly separate temporary mispricing from fundamental change.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet