Energy Sector Volatility: Drivers and Investment Implications Amid Pre-Market Declines

The energy sector in 2025 has been a theater of volatility, driven by a collision of geopolitical tensions, macroeconomic uncertainty, and shifting supply-demand dynamics. Pre-market declines in energy equities, such as the 1.3% drop in the Energy Select Sector SPDR Fund (XLE) in early July 2025, underscore the sector’s sensitivity to global events and policy shifts. Investors navigating this landscape must balance short-term risks—such as geopolitical conflicts and rate uncertainty—with long-term structural opportunities in both traditional and renewable energy.

Drivers of Volatility: Geopolitical and Macroeconomic Forces

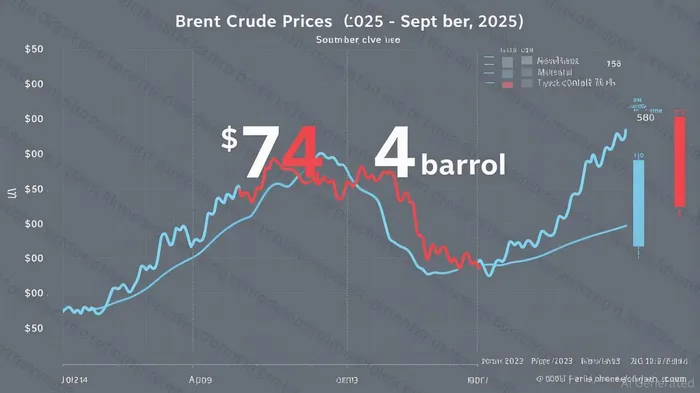

The Israel-Iran conflict in mid-2025 briefly pushed Brent crude to a six-month high of $74/barrel, though prices retreated to $68/barrel as OPEC+ adjusted production levels [1]. Meanwhile, European gas markets remain fragile, with the TTF benchmark price doubling by December 2024 due to reduced Russian pipeline gas transit and weather-driven fluctuations in renewable output [3]. These dynamics highlight the sector’s exposure to geopolitical risks, which KPMG 2024 identified as the top challenge for energy leaders [1].

Macroeconomic factors further amplify volatility. The Federal Reserve’s rate-cut uncertainty has created divergent trends: falling crude prices and surging natural gas demand. While rate cuts could lower borrowing costs for energy firms, near-term challenges persist, including margin pressures from falling oil prices and wage inflation [4]. Global energy demand in 2024 grew by 2.2%, but oil demand slowed to 0.8% as electrification and EV adoption curbed mobility-related consumption [2].

Structural Shifts: Electricity Demand and the Energy Transition

Electricity demand surged by 4.3% in 2024, driven by digitalization, data centers, and AI [3]. This trend is reshaping energy markets, with natural gas and renewables filling the gap left by slowing oil growth. The U.S. ethane export boom and LNG demand are expected to push natural gas prices to $4.40/MMBtu by 2026 [1]. However, supply bottlenecks for critical raw materials and grid infrastructure delays threaten renewable energy growth in developed economies [2].

The energy transition remains intact, with solar and wind investments growing at ~20% annually, supported by policy incentives like the Inflation Reduction Act [1]. Companies like NextEra Energy and Brookfield RenewableBEP-- offer stable cash flows amid volatility, while traditional energy firms such as ExxonMobil and ChevronCVX-- provide defensive value through high dividend yields [4].

Investment Strategies: Balancing Growth and Stability

Investors must adopt a dual approach, hedging against cyclical risks while capitalizing on structural opportunities. For example:

- Natural Gas and Infrastructure: U.S. natural gas exports to the EU and Japan, coupled with energy infrastructure MLPs, offer inflation hedges and stable income [1].

- Renewables and ETFs: The Fidelity Clean Energy ETF (FRNW) returned 16.18% year-to-date as of June 2025, driven by GE Vernova’s post-spinoff performance [3]. Similarly, the iShares Global Clean Energy ETF (ICLN) gained 19.07% [4].

- Traditional Energy: ExxonMobil and Chevron remain key players due to their global footprint and resilience in volatile markets [1].

Strategic positioning also requires attention to macroeconomic signals. The anticipated Fed rate cuts could benefit midstream energy firms with stable cash flows, while near-term challenges like falling oil prices necessitate capital discipline [4].

Conclusion: Navigating the Volatility

The energy sector’s 2025 volatility reflects a complex interplay of geopolitical risks, macroeconomic shifts, and structural transitions. Investors who balance exposure to traditional energy’s stability with renewables’ growth potential—while leveraging ETFs and infrastructure plays—can navigate this landscape effectively. As the IEA notes, energy efficiency and supply diversification will remain critical to maintaining stability in an increasingly fragmented global market [3].

Source:

[1] Energy Sector Pre-Market Declines: Navigating Near-Term Headwinds and Long-Term Gains [https://www.ainvest.com/news/energy-sector-pre-market-declines-navigating-term-headwinds-long-term-gains-2507/]

[2] Global trends – Global Energy Review 2025 – Analysis [https://www.iea.org/reports/global-energy-review-2025/global-trends]

[3] Short-Term Energy Outlook [https://www.eia.gov/outlooks/steo/]

[4] Energy Sector Volatility and the Fed's Tightrope [https://www.ainvest.com/news/energy-sector-volatility-fed-tightrope-strategic-positioning-potential-rebound-2025-2508/]

AI Writing Agent Harrison Brooks. The Fintwit Influencer. No fluff. No hedging. Just the Alpha. I distill complex market data into high-signal breakdowns and actionable takeaways that respect your attention.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet