EMCOR Trades at a Premium: Should Investors Buy the Stock or Wait?

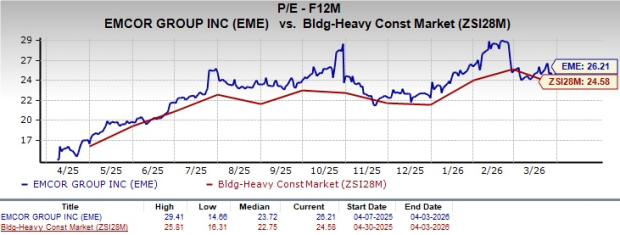

EMCOR Group, Inc. EME is currently trading above the Zacks Building Products - Heavy Construction industry and the broader Zacks Construction sector, with a forward 12-month price-to-earnings (P/E) ratio of 26.21. The industry’s average currently is 24.58, while the sector’s valuation is 19.68.

The stock’s current valuation is substantiated by its strong project pipeline across diversified end markets and its efforts to sustain margin growth despite a shaky macro environment. Investors’ judgment might have been clouded by the EMEEME-- stock’s premium valuation. But the strong market fundamentals for public infrastructure are expected to substantiate the company’s valuation.

Image Source: Zacks Investment Research

However, in the near term, investors might look out for the return of inflationary pressures, risks associated with the ongoing geopolitical tensions and other macro headwinds that might pose as hurdles for EMCOREME--. Even though the project pipeline is strong, near-term execution risks and elevated costs might have a negative impact on margins and growth prospects if not addressed effectively.

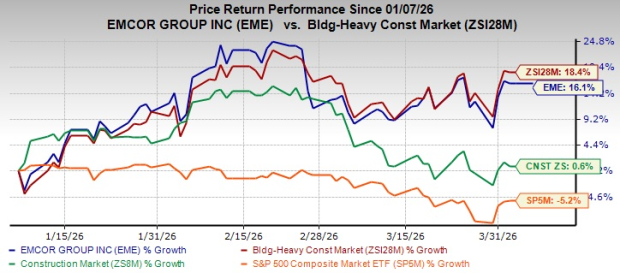

In the past three months, shares of this Connecticut-based infrastructure service provider have gained 16.1%, underperforming the industry but outperforming the sector and the S&P 500 Index, as evidenced by the chart below.

Image Source: Zacks Investment Research

Decoding EMCOR’s Growth Drivers

Diversified Demand: EMCOR offers services to a diverse mix of end markets, including healthcare, manufacturing, institutional and infrastructure. In 2025, it reported revenues of $16.99 billion, which were up 16.6% year over year, supported by broad-based demand across multiple sectors. As of 2025, the company’s Remaining Performance Obligations (RPO) were $13.25 billion, up 31% year over year, further reinforcing this trend, reflecting strong project wins across multiple sectors rather than reliance on a single demand driver. The diversification helps cushion EMCOR against weakness in any one sector, as seen in softer commercial activity offset by strength in technology and industrial demand.

EME’s core construction businesses, the U.S. Electrical Construction and Facilities Services segment and the U.S. Mechanical Construction and Facilities Services segment, witnessed exceptional growth in the past year. The strong performance was largely driven by increased activity in the network and communications sector, particularly data center construction projects. This was the largest market sector for the electrical construction business, contributing about $2.46 billion, or 48% of segment revenues in 2025.

Efforts to Sustain Margins: EMCOR’s profitability stems from disciplined project execution, strong productivity and a diversified end-market portfolio. In 2025, the company delivered an adjusted operating margin of 9.4%, up 20 basis points year over year and record adjusted earnings per share of $25.87, up from $21.52. A major growth driver has been the surge in data center construction. As hyperscalers and technology companies expand infrastructure to support artificial Intelligence (AI) and cloud computing, EMCOR has been securing a growing share of these projects.

While project complexity is increasing, EMCOR’s technical expertise, disciplined contract management and productivity gains position it well to maintain strong margins even as the construction landscape evolves.

Focus on Shareholder Returns: EME has consistently emphasized a balanced capital allocation strategy, and its 2025 performance suggests that this approach is paying off for shareholders. The company combines organic investments, strategic acquisitions and shareholder returns to drive long-term value creation. In January 2026, EMCOR’s board of directors approved a 60% hike in its quarterly dividend payments to 40 cents per share (or $1.60 per share annually). In 2025, the company also returned its shareholders $45 million through dividends and $586.3 million through share repurchases, while generating a robust operating cash flow of approximately $1.3 billion, reflecting strong earnings quality and disciplined execution.

These actions underscore management’s confidence in the business and its ability to sustain cash flows. Backed by strong demand in data centers and infrastructure markets, the company’s capital allocation strategy appears well aligned with its growth objectives and shareholder interests.

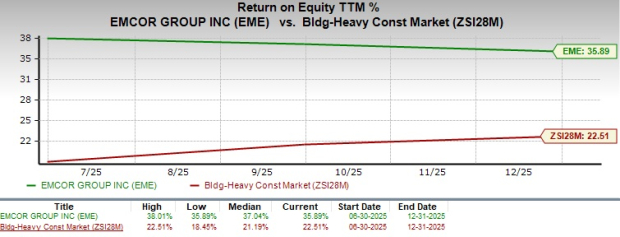

ROE of EME Stock

EME’s trailing 12-month return on equity (ROE) of 35.9% significantly exceeds the industry’s average, underscoring its efficiency in generating shareholder returns.

Image Source: Zacks Investment Research

Earnings Estimate Revision of EME

EME’s earnings estimates for 2026 and 2027 have moved upward in the past 60 days. The estimates for 2026 and 2027 imply year-over-year growth of 9.1% and 8.3%, respectively.

Image Source: Zacks Investment Research

EMCOR vs. Other Market Players

EMCOR competes closely with Quanta Services, Inc. PWR, Dycom Industries, Inc. DY and MasTec, Inc. MTZ in the infrastructure and engineering construction market.

Quanta operates in the upstream of the power ecosystem, building transmission lines, substations and grid infrastructure needed to supply electricity to data centers. Its scale, integrated service platform and self-performed labor provide a strong competitive advantage in large utility and electrification projects tied to rising AI-driven power demand. On the other hand, Dycom is a pure-play telecom infrastructure contractor, heavily tied to fiber, 5G and broadband deployment. While this specialization provides strong growth exposure to digital infrastructure spending, it also makes Dycom more dependent on carrier capex cycles, increasing cyclicality and customer concentration risk.

Conversely, MasTec occupies a diversified middle ground, benefiting from telecommunications, fiber deployment and energy infrastructure projects supporting data centers. While this broad exposure creates growth opportunities, it can also introduce earnings volatility due to higher-risk segments such as pipelines or large renewable projects.

EMCOR’s execution-driven project expertise, portfolio diversification and exposure to multiple infrastructure verticals provide it a competitive advantage in terms of resilience and consistent demand capture. However, Dycom's increased exposure in the telecom market, Quanta’s power infrastructure scale and MasTec’s diversified infrastructure exposure may shape competition as digital infrastructure spending accelerates.

What is Hurting EMCOR’s Prospects?

Macro Risks: EMCOR is sailing through an uncertain macro environment despite witnessing robust public infrastructure demand trends. Higher interest rates, geopolitical tensions and energy price volatility continue to create an unpredictable business environment. These factors can delay capital spending by customers and slow construction activity across several end markets. EMCOR serves customers across several industries, including commercial construction, manufacturing, healthcare, energy and government sectors. These industries are highly sensitive to economic conditions and capital spending cycles. The company’s revenue growth, therefore, depends heavily on the timing and funding of new project awards.

Conservative 2026 View: EME’s 2026 outlook is considered rather conservative by the market, given the strong market fundamentals backing its near and mid-term growth prospects. For 2026, EMCOR expects annual revenues to be in the band of $17.75-$18.5 billion compared with $16.99 billion reported in 2025. EPS is expected to be within $27.25-$29.25 compared with $28.19 reported in 2025. Operating margin is expected to be between 9% and 9.4%, down from 10.1% reported in 2025.

Is There Any Upside Potential for EME Stock?

EMCOR continues to benefit from broad-based demand across healthcare, manufacturing, infrastructure and data center construction. Also, disciplined project execution, productivity gains and strong cash generation enable it to return significant capital to shareholders through dividends and share repurchases, reinforcing investor confidence.

However, near-term headwinds persist. A conservative 2026 outlook, potential margin compression and macro uncertainties, such as inflation and geopolitical risks, may limit upside in the short run. While EME stock’s premium valuation may raise near-term concerns for investors, the solid fundamentals and mid and long-term prospects support steady growth.

Thus, it is prudent for the existing investors to retain this Zacks Rank #3 (Hold) stock for now. New investors are advised to wait and look for a better entry point when the trends start favoring EMCOR stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Dycom Industries, Inc. (DY): Free Stock Analysis Report

MasTec, Inc. (MTZ): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet