Is EMCOR Strengthening Its Growth Position in U.S. Infrastructure?

EMCOR Group, Inc. EME is rapidly sharpening its focus in the United States infrastructure market, with the divestiture of its U.K. Building Services on Dec. 1, 2025, marking the first step toward this strategy. Besides, its strong execution, diversified end markets and a growing project pipeline are backing up the prospects seamlessly.

A key indicator of EME’s strengthening infrastructure footprint is its record remaining performance obligations (RPO) of $13.25 billion, up 31% year over year. This backlog growth has been broad-based, with strong momentum across network and communications, institutional, water and wastewater and manufacturing sectors, areas closely tied to U.S. infrastructure investment.

Primarily, EMCOR’s two major segments, U.S. Electrical Construction and Facilities Services and U.S. Mechanical Construction and Facilities Services, are contributing to the incremental growth. During 2025, revenues from the Electrical Construction and Facilities Services segment increased 51.8% year over year to $5.07 billion, while the Mechanical Construction and Facilities Services revenues grew 10.1% year over year to $7.05 billion. The strong performance was largely driven by increased activity in the network and communications sector, particularly data center construction projects, which remained the largest market sector for the electrical construction business, contributing about $2.46 billion, or 48% of segment revenues in 2025.

Looking ahead, for 2026, EMEEME-- expects annual revenues to be in the band of $17.75-$18.5 billion compared with $16.99 billion reported in 2025. Annual EPS is expected to be within $27.25-$29.25 compared with $28.19 reported in 2025. Thus, with solid backlog visibility, exposure to infrastructure-driven markets and proven execution capabilities, EMCOREME-- appears well-positioned to deepen its role in the evolving U.S. infrastructure ecosystem.

EMCOR Riding Data Center Boom or Facing Power Rivals?

EMCOR, alongside renowned market peers including Quanta Services, Inc. PWR and KBR, Inc. KBR, is positioned differently to capture the data center-driven infrastructure cycle, shaped by AI-led power demand and electrification trends.

Quanta is emerging as a structural winner from data center demand by targeting the upstream power ecosystem. With data centers now a fast-growing portion of backlog, its integrated “total solutions” model, spanning transmission, substations and generation, offers multi-year visibility. On the other hand, KBR operates more indirectly, focusing on engineering, consulting and government-led infrastructure programs rather than core construction or power delivery. This positions it to benefit from long-cycle digital infrastructure and energy transition projects, though with less direct leverage to hyperscale data center builds.

Overall, while EMCOR captures on-site construction demand, Quanta dominates power infrastructure, and KBR participates through advisory and program execution, reflecting distinct yet complementary roles in the evolving data center ecosystem.

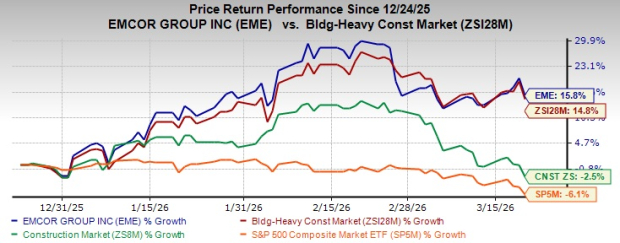

EME Stock’s Price Performance & Valuation Trend

Shares of this Connecticut-based infrastructure service provider have gained 15.8% in the past three months, outperforming the Zacks Building Products - Heavy Construction industry, the Construction sector and the S&P 500 Index.

Image Source: Zacks Investment Research

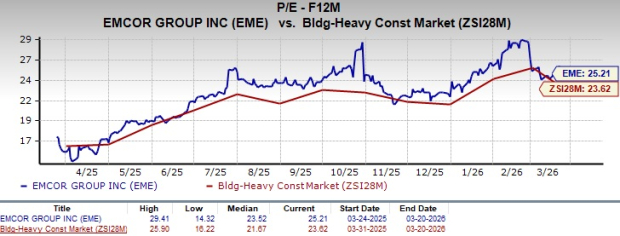

EME stock is currently trading at a premium compared with the industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 25.21, as evidenced by the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision of EME

EME’s earnings estimates for 2026 and 2027 have moved upward in the past 30 days to $28.23 and $30.59 per share, respectively. The estimates for 2026 and 2027 imply year-over-year growth of 9.1% and 8.3%, respectively.

Image Source: Zacks Investment Research

EMCOR stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Quanta Services, Inc. (PWR): Free Stock Analysis Report

KBR, Inc. (KBR): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

Zacks is the leading investment research firm focusing on equities earnings estimates and stock analysis for the individual investor, including stock picks, stock screening, portfolio stock tracker and stock screeners. Copyright 2006-2026 Zacks Equity Research, Inc. editor@zacks.com (Manaing editor) webmaster@zacks.com (Webmaster)

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet