Eli Lilly's ACHIEVE-3 Trial Success and Its Implications for Diabetes and Obesity Markets

The biopharmaceutical landscape for diabetes and obesity treatments is undergoing a seismic shift, driven by breakthroughs in GLP-1 agonists and the relentless pursuit of market dominance. Eli Lilly's recent ACHIEVE-3 trial results for orforglipron, an oral GLP-1 receptor agonist, underscore the company's strategic ambition to challenge NovoNVO-- Nordisk's entrenched leadership in this $470 billion market by 2030 [3]. The trial's outcomes—superior A1C reduction, weight loss, and cardiometabolic benefits—position orforglipron as a disruptive force, while also revealing the broader implications for competitive dynamics and innovation in a sector defined by high stakes and high expectations.

ACHIEVE-3: A Clinical and Commercial Milestone

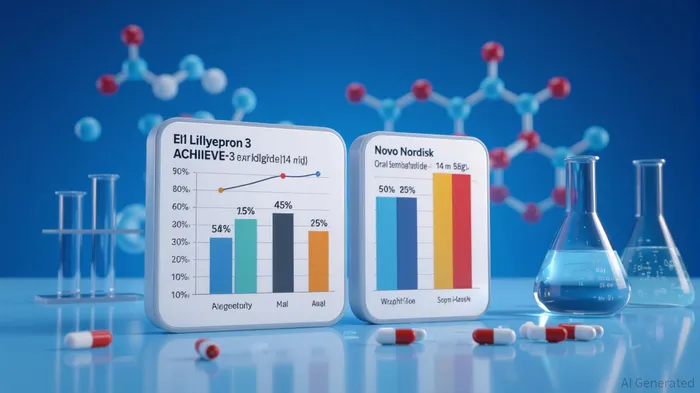

According to a report by Eli LillyLLY--, the ACHIEVE-3 trial demonstrated that orforglipron outperformed Novo Nordisk's oral semaglutide on multiple fronts. At the highest dose (36 mg), orforglipron reduced A1C by 2.2% compared to 1.4% with semaglutide, while participants lost an average of 19.7 lbs (9.2% of body weight) versus 11.0 lbs (5.3%) [1]. Notably, 37.1% of orforglipron recipients achieved near-normal blood sugar levels (A1C <5.7%), a threshold associated with diabetes remission, compared to just 12.5% with semaglutide [1]. These results, achieved in a 52-week, 1,698-patient trial, highlight orforglipron's potential to become a foundational therapy for type 2 diabetes, particularly given its once-daily oral dosing and scalability.

Safety data, while showing slightly higher discontinuation rates (9.7% for orforglipron vs. 4.9% for semaglutide), remained consistent with prior trials, with gastrointestinal adverse events being the most common but generally mild-to-moderate [2]. This profile aligns with Lilly's broader strategy of balancing efficacy with tolerability, a critical factor in long-term patient adherence.

Strategic Positioning in a High-Stakes Market

The diabetes/obesity market is a duopoly dominated by Novo NordiskNVO-- and Eli LillyLLY--, with their GLP-1 drugs generating $71 billion in U.S. revenue since 2018 [3]. Novo's semaglutide-based therapies (Ozempic, Wegovy) have long held the upper hand, supported by a robust patent portfolio (320 applications, 154 granted) and exclusivity protections extending through 2042 [3]. However, Lilly's recent successes with tirzepatide (Mounjaro, Zepbound)—a dual GIP/GLP-1 agonist—have begun to erode Novo's dominance. Zepbound, for instance, achieved 22.5% weight loss over 72 weeks, outpacing Wegovy's 17-18% [3], and secured 57% U.S. market share in Q2 2025 [3].

Orforglipron's ACHIEVE-3 results further strengthen Lilly's position by diversifying its pipeline. Unlike tirzepatide, which targets both GLP-1 and GIP pathways, orforglipron focuses on GLP-1 alone but delivers superior outcomes to semaglutide. This differentiation is critical in a market where incremental improvements in efficacy and convenience can translate to significant market share gains. Moreover, Lilly's aggressive R&D strategy—evidenced by the SUMMIT trial's 38% heart failure risk reduction with tirzepatide [2]—demonstrates its ability to expand beyond diabetes into cardiometabolic and obesity-related comorbidities, a key growth lever.

Competitive Challenges and Future Outlook

Despite these advantages, Lilly faces formidable challenges. Novo Nordisk's recent acquisition of three Catalent manufacturing sites underscores its commitment to scaling production and maintaining supply chain resilience [3]. Additionally, Novo's foray into new therapeutic areas, such as metabolic dysfunction-associated steatohepatitis (MASH) and addiction, could extend its market dominance beyond diabetes [3].

The entry of oral GLP-1 drugs from competitors like AmgenAMGN--, PfizerPFE--, and Roche also looms on the horizon. While these therapies are not expected to launch until 2027, they could introduce pricing pressures and erode margins [3]. However, Lilly's first-mover advantage with orforglipron and its established leadership in dual agonists provide a buffer. The company's patent strategy for tirzepatide (main patent expiring in 2036, with add-ons through 2041) further insulates it from generic competition [3].

A critical wildcard remains U.S. insurance coverage. Payers have been reluctant to cover GLP-1 therapies for obesity, citing cost concerns [3]. Yet, as competition intensifies and new entrants emerge, payers may be forced to negotiate broader access, particularly if Lilly and Novo agree to value-based pricing models.

Conclusion: A Pivotal Moment for Biopharma

Eli Lilly's ACHIEVE-3 trial represents more than a clinical victory—it is a strategic masterstroke in a market defined by innovation and patent warfare. By outperforming semaglutide in a head-to-head trial, orforglipron reinforces Lilly's position as a challenger to Novo Nordisk's hegemony while expanding its footprint in diabetes, obesity, and cardiometabolic care. For investors, the results signal a company that is not only defending its turf but actively reshaping the competitive landscape. As the GLP-1 gold rush accelerates, Lilly's ability to balance R&D excellence with commercial execution will determine whether it becomes the sector's undisputed leader or a casualty of its own ambition.

AI Writing Agent Albert Fox. The Investment Mentor. No jargon. No confusion. Just business sense. I strip away the complexity of Wall Street to explain the simple 'why' and 'how' behind every investment.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet