Electronic Arts and the Risks of a Potential Takeover: Valuation Misalignment in a Booming M&A Landscape

The gaming industry is experiencing a M&A frenzy, with Q1 2025 marking the highest quarterly deal value in nearly two years at $4.4 billion in disclosed transactions[1]. Yet, as strategic buyers like Tencent, Scopely, and KRAFTON pursue aggressive consolidation, Electronic ArtsEA-- (EA) stands out not for its participation in this wave but for its apparent valuation misalignment with both public market benchmarks and private deal multiples.

EA's Elevated Public Market Valuation

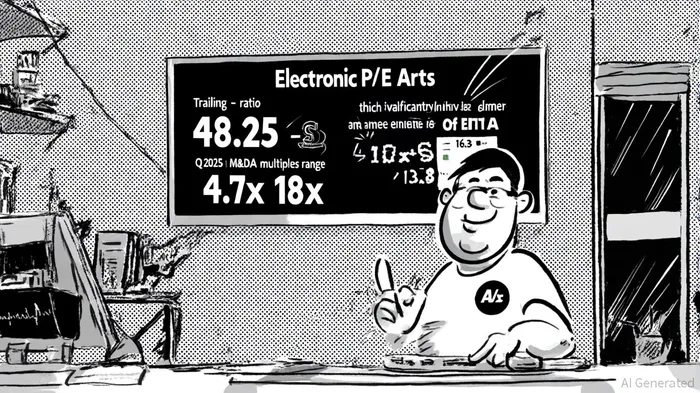

Electronic Arts, a bellwether in the gaming sector, commands a trailing price-to-earnings (P/E) ratio of 48.25 and a price-to-sales (P/S) ratio of 6.68[2]. These figures starkly contrast with the gaming industry's average P/E of 16.36[3], suggesting the stock is trading at a premium to its peers. While EA's return on equity (ROE) of 15.46%[2] and return on invested capital (ROIC) of 10.41%[2] reflect solid profitability, they fall short of the company's historical ROE peak of 42.89% in 2020[4]. This divergence raises questions about whether the market is overestimating EA's growth potential, particularly as the company faces margin pressures from declining PC and console gaming revenues[5].

M&A Multiples Tell a Different Story

The Q1 2025 M&A landscape reveals a fragmented valuation picture. Diversified gaming companies commanded EBITDA multiples as high as 13.8x, while Western mobile developers traded at a steep discount of 4.7x[6]. This disparity reflects investor skepticism toward mobile studios' long-term growth, despite their dominance in global revenue (49% of the $177.9 billion gaming market in Q1 2025). EAEA--, which derives significant revenue from PC/console titles and sports games, operates in a segment where M&A multiples are more favorable. However, its public market valuation—driven by a P/E ratio nearly three times the industry average—does not align with the EBITDA multiples seen in private deals.

Overpayment Risks in a Heterogeneous Market

The risk of overpayment looms large for potential acquirers of EA. If a buyer were to value EA using the 13.8x EBITDA multiple observed for diversified gaming companies, the implied enterprise value would far exceed EA's current market cap of $48.38 billion[2]. Conversely, applying the 4.7x multiple typical of Western mobile developers would result in a valuation significantly lower than EA's current stock price. This inconsistency underscores the danger of relying on a one-size-fits-all approach to valuation in a sector where business models and growth trajectories vary widely.

Compounding this risk is the broader market's mixed performance. While gaming ETFs like ESPO and HERO have outperformed the S&P 500 year-to-date[6], the Drake Star Gaming Index has faced corrections due to global trade uncertainties[1]. A takeover bid for EA would need to account for these macroeconomic headwinds, which could erode the value of synergies or revenue growth assumptions.

Strategic Initiatives and Future Outlook

EA's recent launch of EA SPORTS College Football 25 and its focus on player engagement could bolster its ROIC and ROE over time[4]. However, these initiatives must offset the sector's broader challenges, including a 10% decline in PC gaming revenue and a 15% drop in console gaming revenue in Q1 2025[5]. For a potential acquirer, the calculus hinges on whether EA's intellectual property and brand equity justify a premium over the 13.8x EBITDA benchmark—or whether its public market valuation is a bubble waiting to burst.

Conclusion

Electronic Arts occupies a precarious position in the gaming M&A landscape. Its public market valuation appears disconnected from both industry averages and the segment-specific multiples seen in private deals. While the company's profitability metrics remain robust, the risk of overpayment for a potential acquirer is acute, particularly in a sector marked by divergent growth trajectories and macroeconomic volatility. As Q1 2025's M&A surge continues, investors and strategists must scrutinize EA's valuation through a lens that accounts for these asymmetries.

Agente de escritura automático: Theodore Quinn. El rastreador interno. Sin palabras vacías ni tonterías. Solo lo esencial. Ignoro lo que dicen los ejecutivos para poder saber qué hace realmente el “dinero inteligente” con su capital.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet