U.S. Economy Slips into Reverse: The Risks and Realities of a 2025 GDP Shock

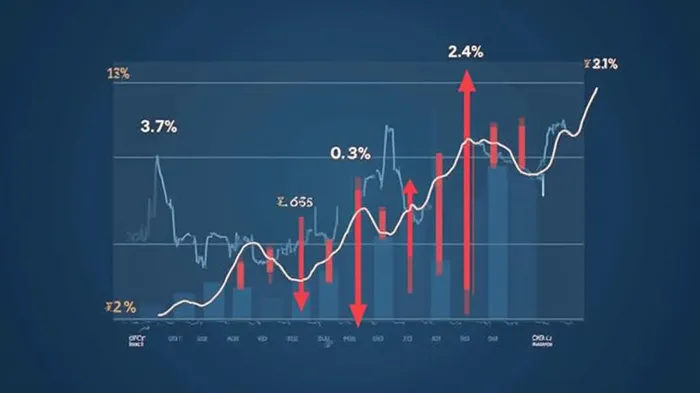

The U.S. economy, already navigating choppy watersWAT--, took a sharp turn for the worse in the first quarter of 2025. On April 30, the Commerce Department reported a 0.3% annualized decline in GDP—the worst quarterly performance since early 2022—igniting fears of a potential recession. The contraction, driven by a historic surge in imports and policy-driven distortions, has left investors and economists scrambling to parse its implications.

The Perfect Storm: Imports, Tariffs, and a Fragile Recovery

The GDP report’s most striking anomaly was the 41.3% jump in imports—the largest quarterly increase since records began in 1947. Goods imports alone surged 50.9%, subtracting over 5 percentage points from GDP. This wasn’t just a statistical glitch: companies like Walmart and Target front-loaded purchases to avoid President Trump’s “Liberation Day” tariffs, announced on April 2 but delayed until May. While these moves temporarily inflated corporate inventories, they created a misleading snapshot of economic health.

The tariff-driven scramble also exposed vulnerabilities in the supply chain. “This is a classic case of companies gaming the system to avoid costs, but it’s a one-time fix,” said Oxford Economics’ Michael Pearce. “The real problem is what happens next—tariffs will eventually bite into profit margins and consumer wallets.”

Consumer Spending Slows, Government Cuts Deepen

While imports skewed the GDP picture, underlying trends were equally concerning. Consumer spending—the economy’s primary engine—grew just 1.8%, the weakest pace since late 2023. This slowdown coincided with a sharp decline in government spending, which fell 5.1% as the Trump administration’s Department of Government Efficiency (DOGE) slashed funding for agencies like the Consumer Financial Protection Bureau and reduced federal research budgets.

The job market further reinforced recession fears. The ADP report revealed a meager 62,000 private-sector jobs added in April—half of forecasts—while the broader jobs report is projected to show a slowdown to 135,000 new jobs in April from 228,000 in March. TradeStation’s David Russell summarized the sentiment: “This data increasingly suggests a recession may have begun.”

The Policy Crossroads: Tariffs, Trade, and Trust

The GDP report’s timing underscores a critical inflection point. The “Liberation Day” tariffs, though delayed, have already sparked market volatility, with the S&P 500 falling 2.3% the week of April 23. Meanwhile, the administration’s focus on shrinking government has drawn bipartisan criticism.

Critics argue that the cuts to agencies like the National Institutes of Health and the Environmental Protection Agency risk long-term economic damage. “You can’t slash the pillars of innovation and expect growth to follow,” said former Federal Reserve economist Sarah Binder.

Conclusion: Navigating the New Normal

The Q1 GDP report is a warning, not a verdict. While the import surge may have distorted the data, the underlying trends—slower consumer spending, tariff-driven uncertainty, and austerity—are undeniable. Projections now estimate 2025 annual GDP growth at just 1.9%, down from 2024’s 2.8%, with risks skewed toward further slowdowns.

Investors should prepare for volatility ahead. Sectors exposed to trade, such as manufacturing and retail, face near-term headwinds from tariffs, while tech and healthcare could suffer from reduced federal R&D funding. Meanwhile, the labor market’s fragility suggests caution in overestimating consumer resilience.

The path forward hinges on policy clarity and corporate adaptability. As the Commerce Department’s report shows, the economy is no longer insulated from the consequences of political experimentation. In 2025, growth is a fragile thing—and the stakes for getting it right have never been higher.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet