Economy Defies the Odds: Strong Jobs, Solid Spending, and Sticky Inflation Put the Fed on Hold

The latest batch of U.S. economic data is delivering a cautiously constructive message for markets: growth is holding up better than feared, but the underlying details still argue for vigilance rather than complacency. With a stronger-than-expected ADP report , resilient Retail Sales , and an expanding—but uneven— ISM Manufacturing survey , investors are increasingly leaning toward a “soft landing still intact” narrative. At the same time, persistent inflation pressures, geopolitical risks, and mixed labor signals are keeping both markets and the Federal Reserve firmly in wait-and-see mode.

Starting with the labor market, the March ADP report came in stronger than expected, with private payrolls rising by 62,000 jobs versus forecasts of 40,000. While the headline number is not particularly robust by historical standards, it represents a steady continuation of hiring and aligns with a broader narrative of moderation rather than deterioration. Importantly, February was revised higher to 66,000, reinforcing the idea that the labor market is slowing gradually rather than cracking. Wage growth also remains firm, with job-stayer pay up 4.5% year-over-year and job-changer pay accelerating to 6.6%, suggesting that income support for consumption remains intact.

However, the composition of the ADP report reveals some emerging fault lines. Job growth is being driven primarily by small businesses, while medium and large firms are either flat or contracting. Sectorally, strength in education and health services continues to offset weakness in trade, transportation, and utilities, which saw a sharp decline. Manufacturing employment also contracted, reinforcing the idea that goods-producing sectors remain under pressure. Regionally, hiring is heavily skewed toward the South, while the Northeast and Midwest saw declines, indicating an increasingly uneven labor market.

Retail sales provided a more encouraging signal on the consumer side. February retail sales rose 0.6% month-over-month, beating expectations and marking a rebound from a flat January print. Even after stripping out autos and gasoline, the data remained solid, with core retail sales rising 0.4% to 0.5%, ahead of consensus. Gains were broad-based, with strength in autos, gasoline, and discretionary categories such as sporting goods and apparel, suggesting that consumer demand remains resilient despite higher prices and ongoing geopolitical uncertainty.

That said, there are nuances worth watching. While headline retail sales are strong, some categories—such as furniture and department stores—remain weak, reflecting ongoing pressure on big-ticket and lower-tier discretionary spending. Meanwhile, the strength in gasoline sales highlights the impact of rising energy prices, which could begin to crowd out other forms of consumption if sustained. The broader takeaway is that the consumer is still spending, but the mix is shifting, and the durability of that strength will depend heavily on inflation trends and labor market stability.

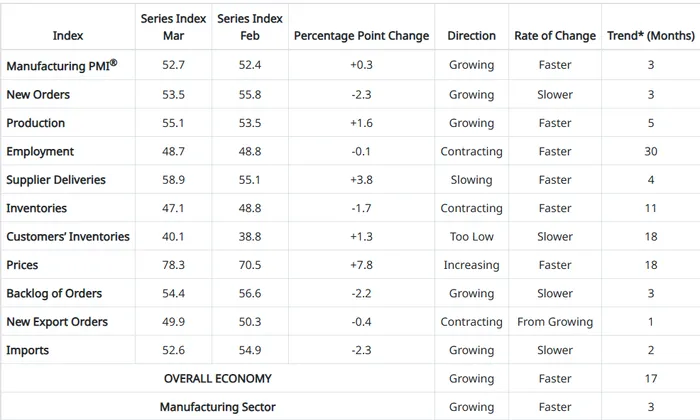

The ISM Manufacturing report added another layer to the “better than feared” narrative, with the PMI rising to 52.7, marking a third consecutive month of expansion. Production and new orders both remained in growth territory, suggesting that manufacturing activity is stabilizing after a prolonged downturn. Notably, customer inventories remain “too low,” which typically points to future production demand and potential restocking cycles.

However, beneath the surface, the report was far from clean. The employment index remained in contraction at 48.7, signaling continued weakness in manufacturing hiring. New export orders also slipped back into contraction, reflecting softer global demand. Perhaps most concerning, the prices index surged to 78.3, its highest level since mid-2022, highlighting a renewed wave of input cost pressures. Much of this appears tied to geopolitical developments, particularly the Middle East conflict, which is disrupting supply chains and driving up energy-related costs.

Comments from Federal Reserve official James Musalem reinforce the cautious interpretation of the data. A noted hawk, Musalem emphasized that monetary policy is “well positioned” and should remain on hold “for some time,” a view that aligns with the current data backdrop. He acknowledged that the economy continues to show solid growth with moderating inflation and stable unemployment as the baseline scenario, but also highlighted rising risks on both sides of the Fed’s dual mandate.

Crucially, Musalem pointed to supply shocks—particularly energy—as a key concern, noting that they carry greater inflation risks in the current environment. He also cautioned against “looking through” these shocks, suggesting that the Fed may be less willing to dismiss temporary price pressures if they begin to feed into broader inflation expectations. At the same time, he acknowledged that tariffs remain an inflation driver, though their impact should gradually wane.

Taken together, the data supports the idea that the Fed has the luxury of time. Growth is holding up, the labor market is not deteriorating rapidly, and while inflation pressures persist, they are not yet spiraling out of control. This allows policymakers to remain patient, avoiding premature rate cuts while monitoring how geopolitical developments—particularly in the Middle East—filter through to energy prices, inflation, and ultimately consumer behavior.

For investors, the key takeaway is that the economy remains resilient, but the margin for error is narrowing. The strength in retail sales and steady job growth provide a buffer against downside risks, but rising input costs, uneven labor dynamics, and global uncertainties continue to cloud the outlook. The next major test will come with the Nonfarm Payrolls report, which will either confirm the stability suggested by ADP or introduce new volatility into the narrative.

In the meantime, markets are likely to remain highly sensitive to incoming data and geopolitical headlines. The “better than feared” theme is enough to support risk assets in the near term, but without a clear improvement in inflation dynamics or a resolution to global tensions, it is unlikely to drive a sustained re-rating higher. For now, the economy is bending—but not breaking—and that is just enough to keep both investors and the Fed cautiously optimistic.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet