Earnings Boom Meets War Risk: Strong Q1 Growth Faces a High-Stakes Reality Check

As the first-quarter earnings season gets underway, expectations are entering the reporting period on unusually strong footing, even as markets grapple with geopolitical volatility and shifting macro dynamics. Analysts have steadily raised estimates over the course of the quarter, signaling confidence in corporate profitability despite the backdrop of rising oil prices, elevated interest rates, and uncertainty surrounding the ongoing conflict with Iran.

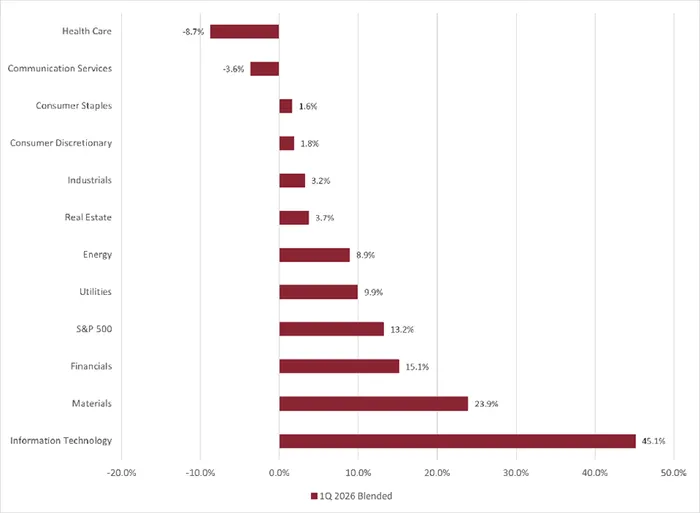

According to FactSetFDS--, S&P 500 companies are expected to deliver earnings growth of approximately 13.2% year-over-year for Q1 2026, marking what would be the sixth consecutive quarter of double-digit earnings growth. Revenue growth is also expected to remain robust at 9.7% year-over-year, representing the strongest top-line expansion since Q3 2022. Notably, both earnings and revenue estimates have been revised higher since the start of the quarter, with total expected earnings increasing by 0.4% to $629.3 billion.

This upward revision trend stands out, particularly given the typical pattern of downward estimate revisions as earnings seasons approach. In fact, analysts have been “more optimistic than normal,” raising projections in aggregate rather than trimming them. This suggests a degree of underlying corporate strength, even as market sentiment has remained cautious.

Corporate guidance has reinforced this constructive setup. Of the 110 S&P 500 companies that have issued EPS guidance for Q1, 59 have delivered positive guidance compared to 51 negative, according to FactSet. This level of positive guidance is well above both the 5-year average (44) and the 10-year average (40), indicating that management teams entered the quarter with relatively strong visibility and confidence in their operations.

However, the strength in estimates and guidance is not evenly distributed across the market. Earnings growth remains highly concentrated in a handful of sectors, most notably Information Technology861077-- and Energy. These two sectors have driven the bulk of upward revisions, with Energy and Technology seeing earnings estimate increases of 8.6% and 8.0%, respectively, since the start of the quarter. Outside of these areas, only Financials861076-- have seen a modest increase in earnings expectations.

At the sector level, nine of the eleven S&P 500 sectors are expected to post year-over-year earnings growth, led by Technology, Materials, and Financials. Meanwhile, Health Care861075-- and Communication Services861078-- are projected to report declines, highlighting the uneven nature of the earnings expansion. On the revenue side, all eleven sectors are expected to deliver positive growth, with Technology, Communication Services, and Financials again leading the way.

Technology’s outsized influence cannot be overstated. The sector is expected to be the primary driver of both earnings and revenue growth, and without it, overall S&P 500 earnings growth would fall to roughly 5%. This underscores the continued dependence of the broader market on a narrow group of high-growth companies, particularly those tied to artificial intelligence and data center investment.

The Magnificent 7—Microsoft (MSFT), AppleAAPL-- (AAPL), NVIDIANVDA-- (NVDA), Alphabet (GOOGL), AmazonAMZN--.com (AMZN), MetaMETA-- Platforms (META), and TeslaTSLA-- (TSLA)—remain central to the earnings narrative. These companies not only represent a significant portion of the index’s market capitalization but are also key contributors to earnings growth. NVIDIA and Tesla, in particular, are expected to deliver outsized earnings expansion, while companies like Apple and Microsoft are projected to post more moderate but still solid growth. In contrast, Alphabet is expected to see a decline in earnings, while Meta and Amazon are showing only low single-digit growth, suggesting some normalization after prior strength.

Beyond sector and company-level dynamics, macro factors are playing an increasingly important role heading into earnings season. The most significant of these is the conflict with Iran, which has driven oil prices sharply higher and introduced a new layer of uncertainty into the outlook. While the direct impact of higher energy prices may not be fully reflected in Q1 results—given that the conflict began late in the quarter—its implications for forward guidance are substantial.

Historically, energy shocks have had mixed effects on earnings, but they tend to weigh most heavily on consumer discretionary sectors861073-- while benefiting energy producers. This dynamic is already being reflected in expectations, with Energy seeing upward revisions and consumer-facing sectors facing greater scrutiny. Investors will be closely watching commentary around input costs, pricing power, and demand elasticity as companies navigate this environment.

Another important macro tailwind is the weakening U.S. dollar. With approximately 40% of S&P 500 revenues coming from international markets, a softer dollar provides a meaningful boost to earnings. Goldman SachsGS-- estimates that a 10% depreciation in the dollar can increase S&P 500 earnings per share by 2–3%, providing an additional layer of support for multinational companies, particularly in the Technology sector.

Despite these supportive factors, valuation remains a key consideration. The S&P 500’s forward 12-month price-to-earnings ratio currently stands at 19.8, slightly below its 5-year average of 19.9 but above its 10-year average of 18.9. While this represents a notable compression from the 22 multiple seen at the end of last year, valuations are still elevated relative to longer-term norms. This leaves less room for disappointment and increases the importance of both results and forward guidance.

Indeed, guidance is likely to be the most critical element of this earnings season. As recent examples have shown, strong backward-looking results are not enough to support stock prices if forward outlooks are cautious. Companies such as NikeNKE-- have already demonstrated that even earnings beats can be overshadowed by weak guidance, while airlines861018-- have flagged rising fuel costs as a headwind.

For Q2 and beyond, analysts are currently forecasting an acceleration in earnings growth, with projections of 19.1% for Q2, 21.2% for Q3, and 19.3% for Q4. Full-year 2026 earnings are expected to grow by 17.4%. However, these forecasts may prove vulnerable if geopolitical tensions persist or if higher energy prices begin to weigh more heavily on economic activity.

As a result, many investors are bracing for cautious or conservative guidance from management teams. The key question is not just how companies performed in the first quarter, but how they expect to navigate an environment characterized by rising costs, shifting demand patterns, and heightened uncertainty.

Market dynamics leading into earnings season further complicate the picture. The first quarter saw significant volatility, with equities declining and bond yields rising as expectations for Federal Reserve rate cuts were pushed out. At the same time, leadership rotated away from mega-cap technology stocks toward previously lagging sectors, reflecting a broader repositioning by investors.

In this context, earnings season is likely to serve as both a confirmation of underlying corporate strength and a test of market resilience. While the data suggests that earnings growth remains solid, the path forward is far less certain. Investors will need to balance strong fundamentals against a challenging macro backdrop, with the trajectory of oil prices, interest rates, and geopolitical developments all playing a critical role.

Ultimately, this earnings season may be less about what companies report and more about what they say. In a market where expectations remain elevated and risks are rising, forward guidance and management commentary will be the key drivers of investor sentiment and market direction in the weeks ahead.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet