Early Warning Signs of a Deeper Stock Market Selloff in August 2025

The stock market is a theater of contradictions in August 2025. On one hand, the S&P 500 clings to its 200-day moving average, buoyed by double-digit earnings growth and a resilient tech sector. On the other, technical indicators, investor sentiment, and macroeconomic divergence are flashing red flags. For investors, the challenge lies in parsing these signals to avoid being caught off guard by a potential selloff.

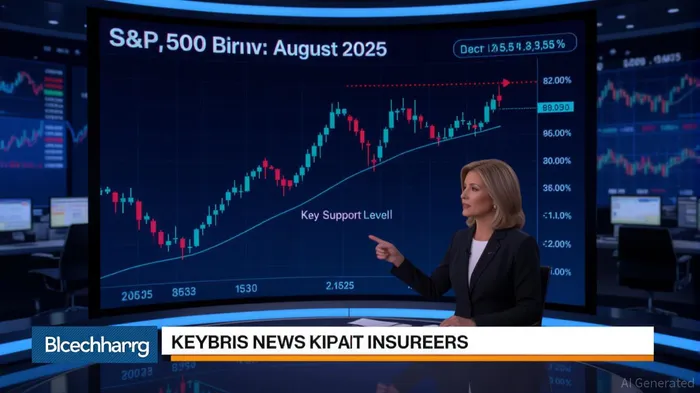

Technical Indicators: A Fragile Bullish Case

The S&P 500's technical profile is a patchwork of conflicting messages. While the 50-day and 200-day moving averages remain in bullish territory, the 5-day and 20-day averages have dipped into negative territory, signaling short-term weakness. The Relative Strength Index (RSI) for the index hovers around 54–57, avoiding overbought territory but showing no clear momentum. Meanwhile, the VIX (Volatility Index) has surged, with its 20-day and year-to-date averages declining by 7.61% and 9.53%, respectively. This divergence—where the S&P 500 trends higher but the VIX reflects rising fear—is a classic precursor to market instability.

The Average Directional Index (ADX) further complicates the picture. The S&P 500's ADX has fallen to 7.57 over 100 days, indicating a lack of conviction in the current trend. Conversely, the VIX's ADX stands at 45.37 for the 9-day period, pointing to a strong bearish bias in volatility expectations. This dissonance suggests that while the index may continue to inch upward, the market is bracing for a sharp correction.

Investor Sentiment: Optimism Masking Undercurrents

The AAII Investor Sentiment Survey reveals a surge in bullish sentiment, with 40.3% of investors optimistic as of July 30, 2025. This is above the historical average of 37.5% but far from the euphoric levels seen in early 2021. However, the Put/Call Ratio tells a different story. While exact figures for August are unavailable, the ratio has historically spiked to above 1.0 during periods of heightened fear, such as the April 2025 tariff announcements. A rising put/call ratio, even if not yet extreme, signals growing defensive positioning.

The Fear & Greed Index, which aggregates seven sentiment metrics, is currently in a “greed” zone but at a level that historically precedes corrections. For example, in 2009, bearish sentiment hit 70.3% before the market bottomed, while in 2021, bullish sentiment peaked at 63.3% before a sharp pullback. The current reading, while not at an extreme, suggests complacency is creeping in.

Macroeconomic Divergence: A Ticking Time Bomb

The broader economic landscape is a minefield of contradictions. J.P. Morgan Research highlights three critical risks:

1. Trade Policy Uncertainty: U.S. tariffs on global goods are expected to dampen growth in both domestic and international markets. While the immediate impact on consumer prices has been muted, the long-term drag on purchasing power and business confidence is a growing concern.

2. Monetary Policy Divergence: The U.S. Federal Reserve's pause on rate cuts contrasts with aggressive easing in emerging markets (EM). This has weakened the dollar, boosting EM currencies but creating capital outflows from U.S. equities.

3. Structural Headwinds: Reduced immigration and a shift away from federal R&D funding are eroding the U.S. economy's long-term growth potential. These factors could force the Fed into a more hawkish stance than currently priced in, triggering a selloff.

The MOVE Index, a bond market volatility gauge, has risen for two consecutive days, signaling renewed anxiety in fixed-income markets. This is a critical warning sign, as bond volatility often precedes equity market turbulence.

Strategic Hedges and Risk Mitigation

For investors, the key is to balance exposure to growth sectors with defensive hedges. Here's how to position your portfolio:

1. Short-Term Volatility Plays: Use VIX futures or inverse VIX ETFs to capitalize on rising fear. The VIX's 9-day RSI at 45.43% and 20-day RSI at 38.67% suggest it's in oversold territory, making it a potential rebound candidate.

2. Defensive Sectors: Overweight utilities, healthcare, and consumer staples, which tend to outperform during corrections. Avoid overleveraged tech stocks, which are most vulnerable to a liquidity crunch.

3. Gold and Treasury Bonds: Gold is projected to hit $3,700 by year-end, driven by central bank purchases. U.S. Treasuries, while facing yield pressures, offer a safe haven if the Fed delays rate cuts.

Conclusion: Navigating the Crossroads

The August 2025 market is at a crossroads. Technical indicators hint at a fragile bullish trend, investor sentiment is optimistic but complacent, and macroeconomic forces are pulling in conflicting directions. History shows that markets often correct when these signals align. For now, the S&P 500 remains in a bullish channel, but a breakdown below key support levels—such as the 6,374.5 July 31st Point of Control—could trigger a deeper selloff.

Investors should treat this as a time to tighten stop-losses, rotate into hedges, and avoid overexposure to high-beta assets. The market may yet surprise to the upside, but the risks of a correction are no longer abstract—they're written in the data.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet