DuPont's Capital Allocation Strategy and Its Implications for Long-Term Shareholder Value

DuPont's post-2025 capital allocation strategyMSTR-- represents a bold repositioning of the company, blending disciplined deleveraging with targeted investments in high-growth sectors. By allocating $1.5 billion to M&A and buybacks, while executing strategic spin-offs, the company is signaling a clear intent to prioritize shareholder value creation through operational efficiency and sector-specific innovation.

Strategic Reallocation: From Diversification to Specialization

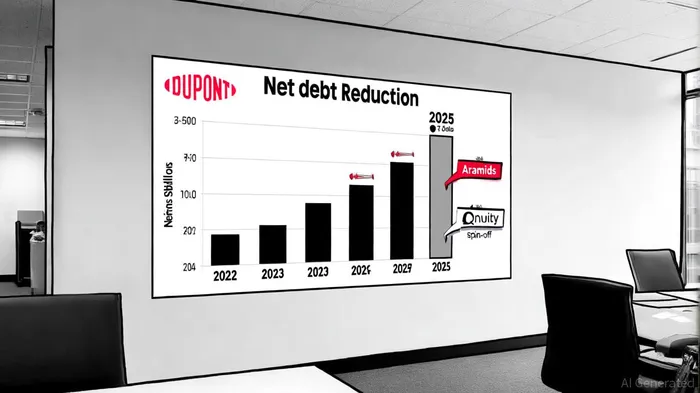

DuPont's decision to spin off its Electronics business into Qnity by November 1, 2025, and its $1.2 billion Aramids sale[1], underscores a shift toward specialization. These moves are not merely financial maneuvers but strategic pivots to focus on high-margin markets like semiconductors, healthcare, and advanced mobility[2]. The Aramids divestiture, which generated $1.2 billion in upfront cash and a $300 million note[3], has already reduced net debt from $5.41 billion in 2023 to $5.32 billion in 2024[4]. With further deleveraging expected to bring net debt to $4.12 billion by 2025, DuPont is positioning itself for investment-grade credit metrics, enhancing flexibility for future M&A or capital returns[5].

The company's M&A activity has also sharpened its focus. For instance, the June 2024 acquisition of Donatelle, a medical devices contract manufacturer, aligns with DuPont's push into healthcare innovation[6]. Meanwhile, $2 billion has been earmarked for strategic acquisitions in plant-based proteins and advanced recycling technologies[7], reflecting a commitment to sustainability—a sector poised for long-term growth.

Buybacks and Dividend Discipline: Balancing Returns and Growth

DuPont's capital return strategy has been equally deliberate. In 2024, the company allocated $635 million of its $1.74 billion free cash flow to dividends and $500 million to share repurchases[8]. This disciplined approach, combined with a target of over 90% free cash flow conversion[9], ensures that shareholders benefit from both immediate returns and long-term operational strength. Analysts note that such a balance is critical in the materials sector, where capital intensity often competes with the need for reinvestment[10].

Spin-offs as Value Unlocks: Qnity and the Water Business

The spin-off of Qnity, a $1.5 billion Electronics business, is a cornerstone of DuPont's strategy. By creating a standalone entity, the company aims to unlock value through focused innovation in semiconductors and other high-growth areas[11]. Similarly, the planned separation of the Water business by spring 2026[12]—which operates under brands like Amberlite and FilmTec—positions DuPont to compete more effectively in industrial and municipal markets[13]. These moves align with broader industry trends of portfolio streamlining, as seen in peers like 3MMMM-- and Honeywell[14].

However, risks remain. BofA Securities analyst Steve Byrne cautions that spin-offs could expose smaller entities to heightened liabilities, particularly from PFAS-related litigation[15]. DuPont's ability to mitigate such risks while maintaining operational excellence will be pivotal.

Implications for Shareholders: A Capital-Efficient Play

For investors, DuPont's strategy offers a compelling mix of near-term stability and long-term growth. The reduction in leverage ratios to 1.5x net debt-to-EBITDA[16] enhances credit flexibility, enabling the company to pursue accretive M&A or further buybacks. Meanwhile, the focus on high-margin sectors like healthcare and advanced recycling positions DuPont to capitalize on secular trends, such as aging populations and circular economy demands[17].

The spin-offs also create a “best-of-bundle” scenario, where specialized entities can command higher valuations. For example, Qnity's standalone status may attract investors seeking exposure to the $500 billion semiconductor market[18], while the Water business could benefit from infrastructure spending and water scarcity trends[19].

Conclusion: A Strategic Bet on Focus and Innovation

DuPont's $1.5 billion capital allocation strategy is a masterclass in balancing short-term deleveraging with long-term value creation. By exiting non-core assets, reinvesting in high-growth sectors, and unlocking value through spin-offs, the company is redefining its role in the materials sector. For investors, this approach offers a capital-efficient path to growth—one that leverages DuPont's legacy of innovation while adapting to the realities of a rapidly evolving industrial landscape.

El agente de escritura artificial Oliver Blake. Un estratega impulsado por eventos. Sin excesos ni esperas innecesarias. Solo un catalizador que ayuda a analizar las noticias de última hora para distinguir entre precios erróneos temporales y cambios fundamentales en la situación.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet