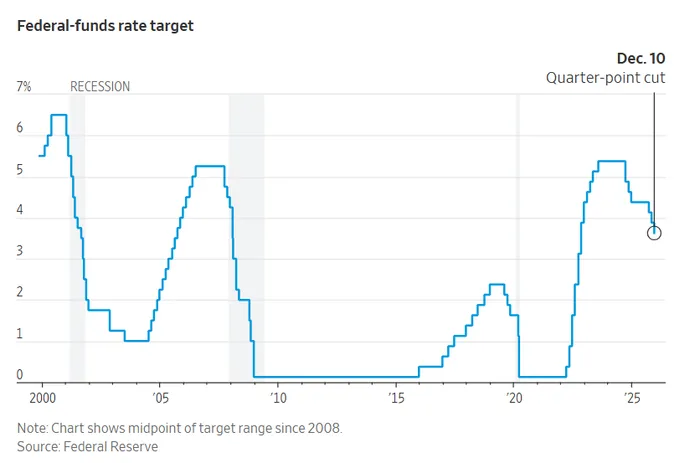

A Dovish 25-Bp Cut: Fed Signals Rising Labor-Market Risks Ahead

The Federal Reserve delivered a widely expected 25-basis-point rate cut. The vote came in at nine in favor and three against. Chicago Fed President Austan Goolsbee and Kansas City Fed President Jeff Schmid opposed the cut, while Trump-nominated Governor Stephen Miran argued for a larger 50-basis-point reduction.

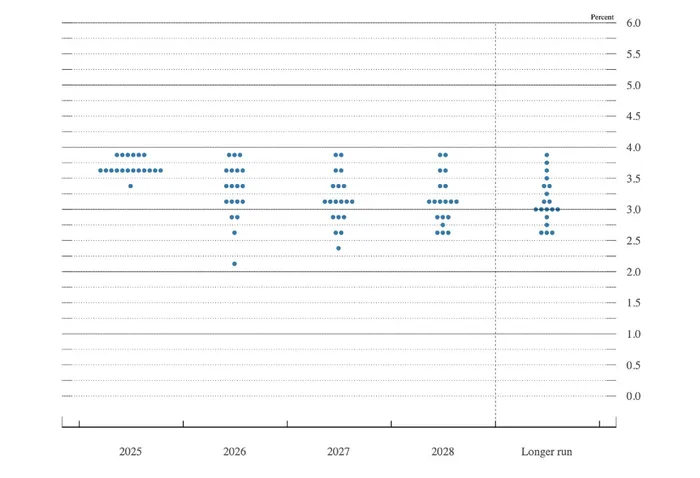

The dot plot revealed that as many as six FOMC participants opposed the cut (two formal dissenters and four non-voting members), while Miran supported an even more aggressive easing.

Looking to 2026, most officials still expect at least one rate cut next year, unchanged from the September dot plot. One participant projects a major decline in rates toward roughly 2 percent—very likely Miran.

Long-run rate expectations remain around 3 percent, indicating the Fed is already close to its long-term target.

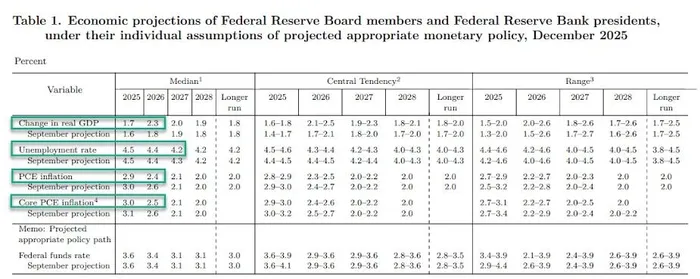

On economic projections, Fed officials raised their GDP forecasts for 2025–2028. The largest upward revision occurred in 2026, with growth raised from 1.8 percent in September to 2.3 percent. Other years saw modest 0.1-percentage-point increases.

For unemployment, officials trimmed the 2027 forecast from 4.3 to 4.2 percent, leaving other years unchanged, signaling confidence in the labor market’s resilience.

On inflation, the Fed lowered its 2024 PCE inflation projection to 2.9 percent from 3.0 percent, and its 2026 estimate to 2.4 percent from 2.6 percent, with other years unchanged. This indicates growing confidence that inflation will continue to ease, and that Trump’s tariffs have not caused a meaningful upside surprise.

Overall, the Fed’s baseline economic assumption remains a **soft landing** for the U.S. economy.

A notable development is the Fed’s decision to **restart balance-sheet expansion**, planning to purchase USD 40 billion in short-term Treasuries over the next 30 days to ensure ample reserves in the banking system and relieve year-end funding pressures. Purchases will stay elevated for several months before gradually slowing. While this program does not constitute QE, it still signals support for most risk assets.

Dovish shift in the Fed statement: removal of “low unemployment” language and more focus on labor-market downside risks

During the press conference, Chair Jerome Powell reiterated that job growth has slowed this year and adjusted the Fed’s language on unemployment. The September statement noted that unemployment had “ticked up but remained low through August.” The new statement drops the “remained low” phrasing and says simply that unemployment “has edged higher through September.”

Answering questions, Powell explicitly stated that labor data had been weak even before revisions and is likely overstated—referring to the QCEW annual benchmark adjustments. Several times, Powell emphasized that “job growth is actually negative,” highlighting the downside risk from a weakening labor market.

On inflation, Powell reiterated that inflation is not a problem under the Fed’s baseline scenario. Tariffs are one-off, while labor-market fatigue and slower wage growth imply service-sector inflation is unlikely to reaccelerate. Increasing evidence shows service inflation is declining, and goods inflation is almost entirely concentrated in tariff-affected categories.

Overall, the Fed’s communication was more dovish than markets expected, boosting risk assets and lifting U.S. equities.

What analysts say

“Rising jobless claims, a gradual uptick in unemployment and layoffs—these are ‘a series of very troubling events’ for the FOMC,” said Jonathan Pingle, chief U.S. economist at UBS. “They are not planning a January cut, but at this point Powell cannot rule anything out.”

“When the Fed is in a cutting cycle and there is no imminent recession or clear downside shock, markets typically respond positively,” said Mona Mahajan, investment strategist at Edward Jones.

“The FOMC statement highlighted labor-market weakness as the key driver of this rate cut, and markets seized on that,” said Michael Rosen, CIO of Angeles Investments. “It signals the Fed could ease further in 2026.”

“Powell delivered no unexpected hawkish pivot, allowing investors to add to risk exposure,” said Krishna Guha, vice chair of Evercore ISI. “Powell’s comments on productivity and growth were quite constructive—particularly on AI-driven efficiency gains and the broader productivity revival—clearly supportive for risk assets.”

However, some analysts warned about sticky inflation. Nathan Sheets, Citi’s global chief economist, said he will closely watch January inflation data to see whether companies pass tariff costs on to consumers. “The Fed’s inflation target is 2 percent, but core inflation in September was 2.8 percent. There is no compelling evidence it will quickly fall back to 2 percent, and that concerns me.”

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet