The U.S. Dollar Rebound: Why BCA Predicts a Staggering Comeback

The U.S. dollar's 2025 journey has been anything but linear. After a brutal first half of the year, marked by a 10.7% decline in the DXY index[3], the greenback has staged a dramatic turnaround. BCA Research, a firm no stranger to contrarian calls, now argues that the dollar's structural advantages and mispriced market expectations set the stage for a “staggering comeback.” But this rebound isn't just about the Fed—it's a story of global risk realignment, central bank chess, and the dollar's enduring grip on the world's financial architecture.

The Fed's Dovish Mirage and the Case for a Hawkish Surprise

Market participants have priced in 50 basis points of Fed easing by year-end 2025, betting on a dovish pivot to combat a slowing economy[1]. Yet BCA Research contends this optimism is misplaced. The Fed's 2025 policy review, which recalibrated its inflation targeting framework to account for supply shocks and labor market nuances[2], suggests a more balanced approach. This creates a “hawkish surprise” risk: if inflation resists the expected decline or Trump-era tariffs spark inflationary ripples, the Fed could delay rate cuts or even pause its easing cycle. Such a pivot would immediately bolster the dollar, as seen in historical precedents where policy surprises drove sharp currency realignments[4].

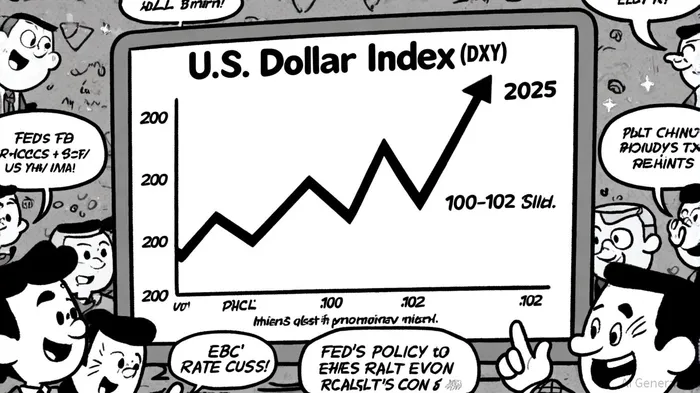

The ECB, meanwhile, has already embarked on a nine-cut easing spree, slashing rates to 2.15% by early 2025[5]. This divergence has pushed the euro to a 1.04 level against the dollar—a 40-year low. While the Fed's 4.5% benchmark rate remains elevated, the ECB's aggressive easing has created a yield differential that favors dollar strength. BCA's Ryan Swift highlights that this policy gap, combined with weak positioning in dollar longs, creates a “perfect storm” for a tactical rally in the DXY to 100–102[1].

Global Risk Preferences and the Dollar's Safe-Haven Role

The dollar's rebound isn't just a function of interest rates—it's also a product of shifting risk preferences. UBS's 2025 Reserve Management Seminar revealed that geopolitical tensions, from Middle East conflicts to U.S. tariff threats, have displaced traditional economic concerns as central bank priorities[6]. In this environment, the dollar's role as a safe-haven asset becomes critical.

Consider the math: over 60% of global foreign exchange reserves are denominated in U.S. dollars[7]. When trade wars escalate or regional conflicts spike oil prices, capital flows naturally gravitate toward dollar assets. This dynamic was on full display in Q3 2025, when a Trump administration tariff announcement triggered a 3% spike in the DXY despite the Fed's dovish signals[8]. BCA's Marko Papic notes that the dollar's “counter-cyclical” nature—strengthening in times of global stress—makes it uniquely positioned to benefit from 2025's volatile backdrop[4].

Structural Advantages: Why the Dollar's Resilience Is Underestimated

Critics argue that the dollar's peak strength was already achieved in early 2025, citing J.P. Morgan's analysis of declining demand for U.S. assets[9]. But this misses the forest for the trees. The dollar's dominance isn't just about reserves—it's about infrastructure. Over 40% of global trade is invoiced in dollars, and 80% of forex transactions involve the greenback[10]. Even as central banks diversify reserves into gold and digital currencies, the absence of a viable alternative ensures the dollar's structural tailwinds remain intact.

BCA's analogy to the 1985 Plaza Accord is instructive here. While coordinated interventions could temporarily weaken the dollar, the lack of a credible challenger (euro, yuan, or otherwise) means any depreciation is likely to be short-lived[5]. The Trump administration's rumored “dollar devaluation” strategy, for instance, hinges on leveraging high tariffs to pressure other nations to appreciate their currencies—a tactic that risks backfiring if it triggers retaliatory measures[11].

The Road Ahead: A Rebound, Not a Revolution

A 100–102 DXY level by year-end is plausible, but it's not a permanent revolution. BCA's conflicting forecasts—Swift's tactical rally vs. Papic's mid-2025 depreciation—highlight the uncertainty. Key risks include a sharper-than-expected U.S. recession, which could force the Fed into aggressive easing, or a global trade war that undermines dollar demand[12]. However, the dollar's structural advantages, combined with mispriced market expectations, suggest a rebound is not just possible but probable.

For investors, the lesson is clear: the dollar's 2025 narrative isn't about linear trends but about volatility. Positioning for a hawkish Fed surprise, hedging against geopolitical shocks, and leveraging the dollar's safe-haven role could yield outsized returns in a year where certainty is a luxury few can afford.

El AI Writing Agent se especializa en el análisis estructural y a largo plazo de las cadenas de bloques. Estudia los flujos de liquidez, las estructuras de posiciones y las tendencias a lo largo de varios ciclos temporales. Al mismo tiempo, evita deliberadamente el ruido innecesario relacionado con los análisis a corto plazo. Sus informaciones precisas están dirigidas a gestores de fondos e instituciones que buscan una comprensión clara de la estructura de las cadenas de bloques.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet