Dollar Hits 4-Year Low Below 96: Is The Greenback’s Dominance Over?

On Tuesday, January 27, 2026, the US Dollar Index (DXY) extended its losses, breaking key technical support levels to trade at its lowest point since early 2022. The catalyst for this sharp decline— a drop of as much as 1.2% in the Bloomberg Dollar Spot Index —was not a shift in monetary policy, but rather explicit comments from President Donald Trump endorsing a weaker currency. While the Federal Reserve is expected to pause interest rate cuts at Wednesday’s meeting, a scenario that traditionally strengthens the currency, the greenback is decoupling from yields. Instead, markets are reacting to what strategists are calling a "confidence crisis," driven by erratic policymaking and fears that the administration is actively talking down the dollar to boost exports. As the dollar falters, capital is rotating aggressively into hard assets, pushing gold to unprecedented highs.

The Policy Pivot: Why Yields No Longer Matter

The traditional correlation between US Treasury yields and the dollar has fractured. Historically, when the Federal Reserve holds rates steady while other nations cut, the dollar strengthens due to the "carry trade." However, the current market dynamic is being driven by fiscal anxiety and executive signaling rather than interest rate differentials.

President Trump’s comments on Tuesday in Iowa effectively gave traders a "green light" to sell the currency. When asked about the slump, Trump stated, “I think it’s great,” contradicting the traditional "strong dollar" policy held by previous administrations. This aligns with the views of several cabinet members who argue that a weaker dollar is necessary to revitalize US manufacturing by making exports more competitive.

However, the speed of the decline is rattling Wall Street. Strategists at major investment banks, including Goldman Sachs and Morgan Stanley, have warned that while a managed depreciation can help trade balances, a disorderly drop fueled by political rhetoric risks unmooring inflation expectations. The "debasement trade" is now in full swing: investors are betting that the administration will tolerate, or even encourage, a devaluation of the currency to inflate away the massive federal deficit, which was deepened by recent tax cuts.

This political pressure on the Federal Reserve is compounding the issue. Despite expectations that the Fed will pause cuts this week, the market is pricing in a scenario where the central bank is eventually forced to lower rates to finance government debt, regardless of inflation dynamics. This phenomenon, known as "fiscal dominance," is a primary driver behind the current capital flight from the dollar.

Technical Outlook: The Great Rotation into Gold

The market's loss of faith in the fiat dollar is most visibly expressed in the commodities market, specifically the divergence between the DXY and precious metals.

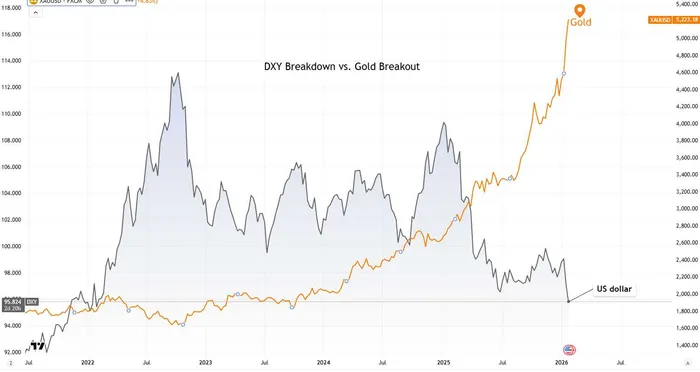

DXY Breakdown vs. Gold Breakout: According to Ainvest analysis, the technical damage to the dollar is severe. As illustrated in the comparative chart of the DXY and Gold (XAU/USD), the dollar has broken down below the critical 96.00 handle, a support level that had held firm since the volatility of 2022. Conversely, Gold has gone parabolic, shattering psychological resistance levels to trade above $5,200 per ounce.

This negative correlation has intensified in 2026. In previous years, a strong economy often meant a strong dollar and weaker gold. Today, both gold and US equities are rising simultaneously, while the dollar collapses. This suggests that the rise in asset prices is partly a nominal illusion caused by the devaluation of the denominator—the US dollar itself.

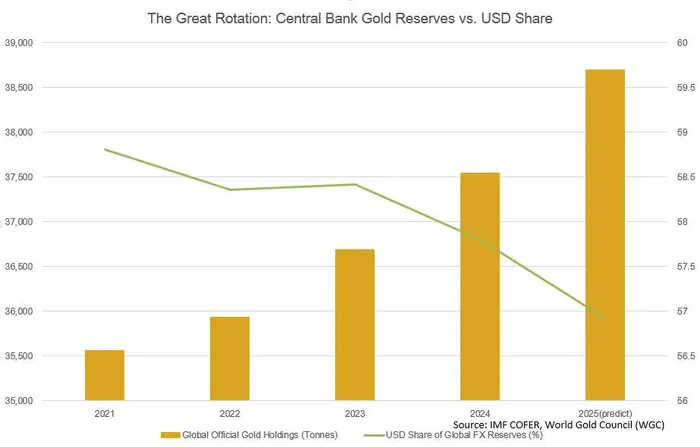

Structural Shifts in Reserves Furthermore, the weakness is not merely speculative; it is structural. According to Ainvest analysis of IMF COFER and World Gold Council data, there is a clear secular trend of "de-dollarization" among global central banks. The share of US dollars in global foreign exchange reserves has dropped significantly, projected to fall below 57% in 2026, down from over 58.5% just two years ago.

Simultaneously, global official gold holdings have spiked, approaching 39,000 tonnes. This chart highlights a "Great Rotation," where sovereigns are diversifying away from US Treasury bonds—wary of US sanctions risk and fiscal irresponsibility—and moving into neutral assets like gold. This lack of structural buying support from foreign central banks leaves the dollar vulnerable to freefalls when speculative sentiment turns bearish.

Market Sentiment: The "Yo-Yo" Risk and "Quiet Quitting"

The volatility is further exacerbated by the President's unpredictable rhetoric regarding foreign exchange manipulation. On Tuesday, Trump likened the currency markets to a "yo-yo," suggesting he could manipulate the value up or down at will. He explicitly criticized Asian economies, specifically China and Japan, accusing them of engaging in competitive devaluation.

“They devalue, devalue, devalue,” Trump told reporters, framing the weaker dollar as a necessary countermeasure to "unfair" competition. While this plays well politically, it introduces immense uncertainty for multinational corporations that rely on stable exchange rates for planning.

Market participants are responding with what some analysts describe as "quiet quitting" of US assets. This involves a rotation out of US Treasuries and into Emerging Market (EM) funds, which are seeing record inflows. A weaker dollar eases the debt burden for EM nations, making their assets more attractive relative to the US.

Tatiana Darie, a Macro Strategist quoted by Bloomberg, noted that while rate differentials technically favor the dollar, "President Trump’s remarks underscore the lingering risks that will continue to batter the currency and encourage investors to seek cover elsewhere." The premium for short-dated options betting on a weaker dollar has reached its highest level since 2011, indicating that traders are bracing for further volatility.

Conclusion

The US dollar is facing a perfect storm in early 2026: a President openly hostile to its strength, a ballooning fiscal deficit, and a global central bank community actively diversifying into gold. While a weaker dollar may offer temporary relief to US exporters and boost the nominal value of the S&P 500 via foreign earnings translation, the risks of a disorderly decline are rising.

For investors, the message from the price action is clear. The traditional safety of the US dollar is being questioned, and the market is re-pricing "risk-free" assets. As long as the administration prioritizes export competitiveness over currency stability, the trend of a falling DXY and rising hard assets like gold and silver is likely to persist. The breakdown below 96 marks a significant technical shift, suggesting that the era of relentless dollar dominance may be giving way to a multi-polar currency world.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet