DocuSign Q3 Earnings: Strong Revenue Growth and Record Free Cash Flow Spur Muted Reaction in Shares

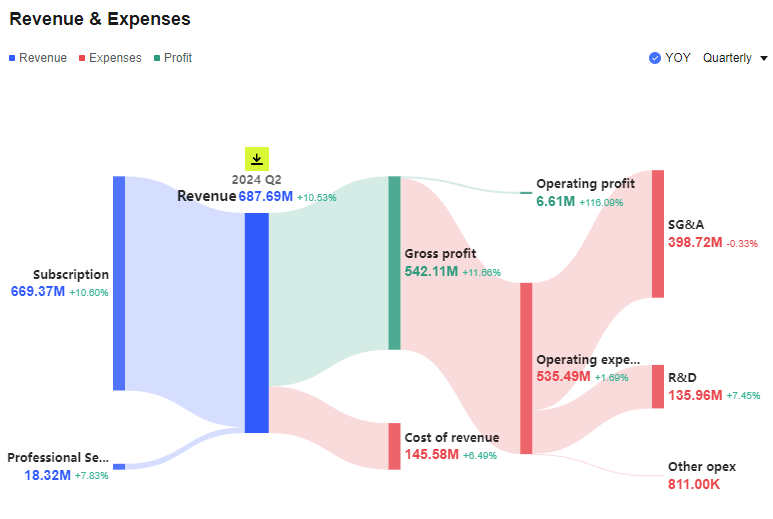

DocuSign Inc. (NASDAQ: DOCU) reported its Q3 FY2024 earnings, beating both earnings per share (EPS) and revenue estimates. The company's total revenue increased by 9% year-over-year to $700.4 million, with subscription revenue accounting for the bulk of the total revenue at $682.4 million, also up 9% YoY. However, professional services and other revenue decreased by 16% YoY to $18.1 million.

Non-GAAP net income per diluted share rose to $0.79, up from $0.57 in the same period last year, while GAAP net income per basic and diluted share was $0.19, a significant improvement from a loss of $0.15 per share in the same period last year. The company's free cash flow reached a record $240.3 million, compared to $36.1 million in the same period last year, reflecting strong operational efficiency.

DocuSign also achieved a record non-GAAP operating margin and announced several operational and strategic developments, including being named a Leader in the 2023 Magic Quadrant for Contract Life Cycle Manager report by Gartner for the fourth consecutive year. The company also expanded its global presence with the opening of an engineering center of excellence in India.

Looking ahead, DocuSign provided guidance for the quarter ending January 31, 2024, with total revenue expected to be between $696 million and $700 million, and billings projected to be between $758 million and $768 million. The company anticipates a non-GAAP gross margin of 81.0% to 82.0% and a non-GAAP operating margin of 22.5% to 23.5%. For the full fiscal year ending January 31, 2024, total revenue is expected to be between $2,746 million and $2,750 million, with a non-GAAP operating margin of 24.0% to 25.0%.

In conclusion, DocuSign continues to demonstrate its ability to grow revenue and improve operational efficiency. The company's focus on product innovation and market leadership is reflected in its solid financial performance and strategic initiatives. As DocuSign expands its offerings beyond e-signature into intelligent agreement management, it remains well-positioned to capitalize on the growing demand for digital transaction management solutions.

If there's anything wrong with this picture, it lies in the reaction: DOCU shares are lower (slightly) off the print. The initial kneejerk was to the upside. But that was quickly wiped away. One can imagine the conversations on stock forums among holders of DOCU shares: Why is this not higher after a report like that? Perhaps a round of upgrades tomorrow morning will do the trick. But it's usually best to not argue with the market.

Senior Analyst and trader with 20+ years experience with in-depth market coverage, economic trends, industry research, stock analysis, and investment ideas.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet