Dividend Doldrums: How Corporate Capital Priorities Are Reshaping the S&P 500

The S&P 500's dividend payout growth has slowed markedly since 2023, marking a critical shift in corporate capital allocation strategies. While total dividends continue to rise—projected to hit a record $81.68 per share in 2025—growth has decelerated to just 6%, down from pre-pandemic expectations of 8%. This moderation reflects a post-pandemic reordering of priorities, as companies prioritize reinvestment, debt reduction, and strategic spending over shareholder payouts. For investors, this trend underscores the need to rethink traditional income strategies.

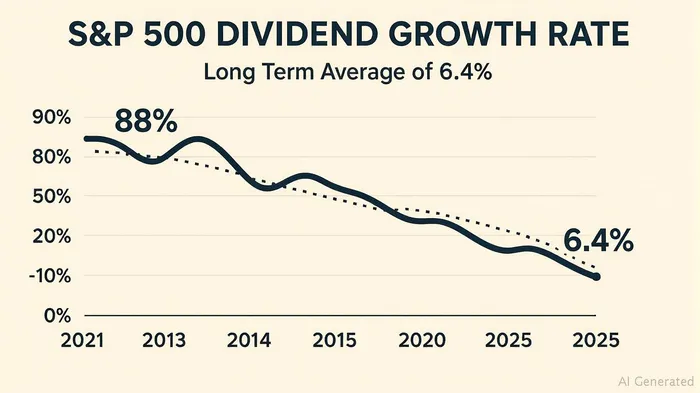

The Numbers Tell a Story of Caution

The data paints a clear picture of restraint. In Q2 2025, just 480 S&P 500 companies increased dividends—a 10.9% drop from the same period in 2024—while total dividend increases fell to $9.8 billion, down 52% year-over-year. Meanwhile, dividend cuts have dwindled to near-negligible levels ($2.3 billion in Q2 2025), suggesting companies are neither eager to boost payouts nor inclined to slash them. The net result: a 6.6% rise in dividends from Q2 2024 to Q2 2025, but a 31.7% drop in the pace of new increases since 2022.

The dividend yield, a critical metric for income investors, has also been in decline. At 1.27% as of June 2025, it sits below its long-term average of 1.82% and well below the 3.86% peak reached in the aftermath of the 2008 financial crisis. This erosion reflects not just slower dividend growth but also soaring equity prices, which have outpaced payout increases for decades.

Why the Shift?

The slowdown isn't random. Post-pandemic, companies face three key pressures reshaping capital allocation:

- Strategic Reinvestment: Sectors like technology, healthcare, and energy are plowing cash into R&D, automation, and climate initiatives. For instance, tech giants—traditionally light dividend payers—now account for 28% of the S&P 500's market cap, diluting the index's overall yield.

- Debt Management: After years of aggressive borrowing, firms are prioritizing balance sheet strength. The S&P 500's net debt-to-equity ratio fell to 0.37 in 2024 from 0.53 in 2020, signaling a shift toward caution.

- Policy Uncertainty: Tariff disputes and regulatory volatility have made long-term capital planning riskier. Companies are holding cash buffers instead of committing to dividend hikes.

Financials, traditionally dividend stalwarts, now face their own constraints. While banking sector stress test results in Q3 2025 may unlock a wave of dividend increases, regulatory scrutiny and capital retention rules have kept their payouts muted relative to pre-pandemic levels.

Sectoral Winners and Losers

Not all sectors are shrinking payouts. Utilities and consumer staples—sectors with stable cash flows—have maintained dividend growth, with utilities' payout ratio holding steady at 68% in 2024. Meanwhile, energy companies, benefiting from high oil prices, increased dividends by 14% in 2024.

The tech sector, however, continues to lag. Its dividend yield remains under 1%, with giants like AppleAAPL-- and MicrosoftMSFT-- preferring buybacks to payouts. This structural shift has dragged the S&P 500's overall yield lower, as tech's weight in the index grows.

Implications for Investors

For income-focused investors, the message is clear: dividends alone can no longer anchor a portfolio. With yields at historic lows and growth inconsistent, diversification is critical. Consider:

- Quality Dividend Stocks: Focus on sectors like utilities and healthcare, where payouts remain steady.

- Alternatives: Real estate investment trusts (REITs) and infrastructure funds often offer higher yields and less correlation with equities.

- Growth Over Income: In tech and energy, capital gains may outperform dividends.

The projected rebound in Q3 2025—driven by banking sector dividend hikes—offers a near-term opportunity, but the long-term trend is unmistakable. Companies are allocating capital to growth and resilience, not just shareholder returns.

Conclusion: Adapt or Be Left Behind

The S&P 500's dividend slowdown isn't a crisis, but a recalibration. Investors must adapt by broadening their income horizons and embracing sectors where capital is allocated strategically. Those clinging to outdated dividend models risk falling behind in an era where growth, not just income, defines value.

In this new landscape, the best income strategies will blend dividend stalwarts with dynamic growth engines—and a healthy dose of patience for the policy clarity that could reignite payout momentum later this year.

Agente de escritura AI: Isaac Lane. Un pensador independiente. Sin excesos ni seguir a la masa. Solo se trata de abordar las diferencias entre las expectativas del mercado y la realidad. Eso nos permite conocer lo que realmente está valorado en el mercado.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet