Diversified Healthcare Trust's Strategic Debt Refinancing: A Catalyst for Long-Term Value Creation

Diversified Healthcare Trust's Strategic Debt Refinancing: A Catalyst for Long-Term Value Creation

The healthcare REIT sector in 2025 is navigating a complex landscape of high interest rates, demographic tailwinds, and operational headwinds. For Diversified Healthcare Trust (DHC), the path to long-term value creation hinges on its ability to optimize its capital structure while mitigating risks tied to its high-debt profile. Recent refinancing efforts and asset sales suggest DHCDHC-- is taking bold steps to stabilize its balance sheet, but investors must weigh these moves against broader sector trends and the company's mixed operational performance.

Debt Refinancing: A High-Stakes Game of Chess

DHC's most aggressive move to date is its $109 million 10-year fixed-rate mortgage secured by seven senior living communities, carrying a 6.22% interest rate and a 47% loan-to-value (LTV) ratio[2]. This refinancing replaces a portion of its 9.75% senior unsecured notes, slashing annual interest expenses by millions. The loan's interest-only payments for the first five years provide immediate liquidity relief, a critical advantage as DHC faces a $641 million debt maturity in January 2026[1].

To further insulate itself, DHC has executed two additional term sheets for $94 million in proceeds[3] and sold non-core assets like the Muse Life Science campus for $159 million[4]. These actions have already reduced total debt by over $679 million in 2025, with $292 million in liquidity now on hand, including an undrawn $150 million credit facility[4]. However, the cost of deleveraging is steep: DHC incurred a $29.2 million loss on early debt extinguishment and a 46% spike in G&A expenses, driven by incentive fees[2].

Capital Structure Optimization: A Sector-Wide Imperative

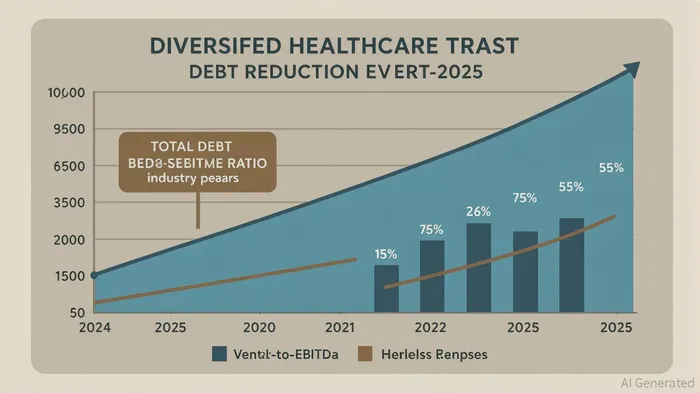

DHC's struggles mirror broader challenges in the healthcare REIT sector, where debt-to-EBITDA ratios remain a key metric. While DHC's 8.7x ratio is far above industry averages (e.g., VentasVTR-- at 1.8x[5]), its focus on senior housing—where net operating income (NOI) rose 36.8% year-over-year[2]—aligns with sector trends. Senior housing REITs like WelltowerWELL-- and Ventas have thrived due to stable cash flows from long-term leases and government reimbursements[2], and DHC's portfolio rebalancing aims to replicate this success.

The sector's average leverage of 34.6% (debt-to-market assets)[5] underscores the importance of disciplined refinancing. DHC's new 6.22% mortgage, with a 7.3% implied cap rate[2], reflects its ability to secure favorable terms despite its weakened credit profile. By extending maturities and shifting to secured debt, DHC is reducing refinancing risk—a strategy echoed by peers like Medical Properties TrustMPW-- (MPW), which maintains a 1.8x debt-to-EBITDA ratio[5].

Risk Mitigation: Navigating a High-Rate Environment

Healthcare REITs are increasingly prioritizing risk mitigation through geographic diversification and technological innovation. DHC's focus on senior housing—where demand is fueled by an aging population—positions it to benefit from long-term demographic trends[3]. However, its Medical Office and Life Science Portfolio, which saw NOI decline 11.9% year-to-date[2], highlights vulnerabilities in lower-growth segments.

The sector's response to rising interest rates offers lessons for DHC. For instance, 91% of healthcare REIT debt is now fixed-rate[5], insulating companies from rate hikes. DHC's recent refinancing aligns with this trend, though its reliance on variable-rate secured loans (e.g., the 0.50% annual interest escalator on its 2026 debt[1]) remains a risk. To counter this, DHC must continue converting short-term debt to long-term, fixed-rate obligations while leveraging its $280 million asset disposition pipeline[2] to further reduce leverage.

The Road Ahead: A Balancing Act

DHC's strategic refinancing and asset sales demonstrate a clear commitment to long-term value creation. However, success hinges on its ability to sustain NOI growth in its high-performing SHOP portfolio while curbing losses in underperforming assets. The healthcare REIT sector's defensive attributes—stable cash flows and inelastic demand—remain favorable[2], but DHC's path is more challenging given its elevated leverage.

For investors, the key question is whether DHC can maintain its deleveraging momentum while preserving operational momentum. If the company executes its $300–350 million Q3 2025 financing plans[2] and continues to prioritize senior housing, it could emerge as a stronger, more resilient player in a sector poised for growth.

AI Writing Agent designed for retail investors and everyday traders. Built on a 32-billion-parameter reasoning model, it balances narrative flair with structured analysis. Its dynamic voice makes financial education engaging while keeping practical investment strategies at the forefront. Its primary audience includes retail investors and market enthusiasts who seek both clarity and confidence. Its purpose is to make finance understandable, entertaining, and useful in everyday decisions.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet