The Disconnect Between Political Pressure and Market Realism: Why a 50-Basis-Point Rate Cut May Not Be in the Cards

The Federal Reserve faces a familiar dilemma: balancing political demands for rapid action with the realities of a complex economic landscape. As President Trump's administration pushes for aggressive rate cuts to offset the costs of its expansive tariff regime, investors and analysts are left to parse whether the Fed will yield to political pressure or adhere to its data-driven mandate. The July 2025 inflation report, which showed a 0.2% monthly rise in the Consumer Price Index (CPI) and a 3.1% annual core CPI, has intensified this debate. Yet a closer look at the data—and the Fed's recent communications—suggests that a 50-basis-point rate cut, while politically desirable, may not align with the central bank's cautious calculus.

The Political Push for Easing

President Trump's rhetoric has been unambiguous: he has criticized the Fed for “tightening too late” and demanded immediate rate cuts to reduce borrowing costs for his administration's infrastructure and tax-cut initiatives. Treasury Secretary Scott Bessent has echoed these calls, advocating for a 50-basis-point reduction in September and a total of 150–175 basis points of easing by year-end. Such a move would align with Trump's broader economic agenda, which includes offsetting the inflationary drag of tariffs on imported goods. However, the Fed's independence—long a cornerstone of its credibility—remains intact.

Chair Jerome Powell has repeatedly emphasized that the Fed's decisions are guided by economic fundamentals, not political expediency. In a July 30 statement, the Federal Open Market Committee (FOMC) reaffirmed its commitment to a “data-dependent approach,” noting that while inflation remains “somewhat elevated,” it is trending toward the 2% target. The committee also highlighted the risks of premature easing, particularly as tariffs could create temporary but unpredictable inflationary shocks.

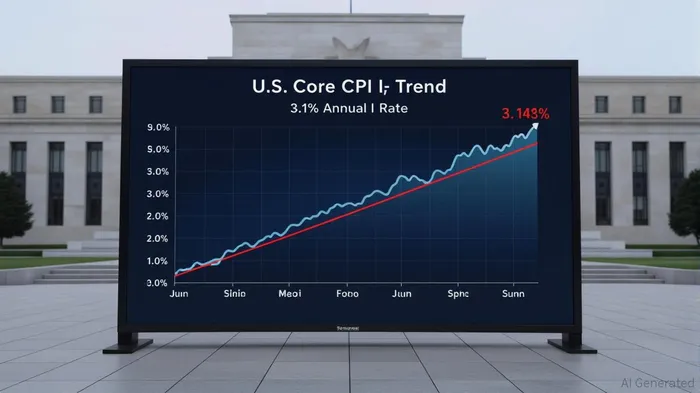

The Data-Driven Reality

The July inflation report, while not a disaster, was far from a green light for aggressive rate cuts. Core CPI, which excludes volatile food and energy, rose 0.3% for the month and 3.1% annually—the largest monthly increase since January. This uptick was driven by sticky service-sector inflation, particularly in shelter costs (up 0.2% for the second consecutive month) and medical care services (up 0.8%). While headline inflation has moderated to 2.7%, the core metric suggests that underlying inflationary pressures are not yet fully under control.

Moreover, the labor market, though showing signs of softness, remains resilient. The July jobs report added just 73,000 nonfarm payrolls, a sharp decline from earlier months, but the unemployment rate remains near historic lows. Powell and other FOMC members have warned that the labor market's “downside risks” are real but not yet severe enough to justify a large rate cut. As Governor Christopher Waller noted in a recent speech, “Tariffs may create a one-time price-level shock, but they are not a sustained inflationary threat. The Fed must look through these temporary effects.”

Market Pricing vs. Policy Prudence

Despite the Fed's cautious stance, financial markets have priced in a near-certainty of a 25-basis-point cut in September, with futures markets assigning a 96% probability to the move. Some analysts, including J.P. Morgan's Elyse Ausenbaugh, argue that the Fed is “behind the curve” and that a 50-basis-point cut would better align with the slowing economy. However, this view overlooks the Fed's dual mandate and the risks of overreacting to short-term data.

The Fed's balance sheet reduction program, which has slowed to a crawl, also complicates the case for aggressive easing. While the central bank has reduced its holdings of Treasury and mortgage-backed securities, its balance sheet remains significantly larger than pre-pandemic levels. A 50-basis-point cut could exacerbate financial market volatility, particularly if inflationary pressures resurge in the fourth quarter.

Why Investors Should Stay Grounded

For investors, the key takeaway is that political noise often overshadows economic fundamentals. While Trump's calls for rapid rate cuts may dominate headlines, the Fed's recent actions suggest a more measured approach. A 25-basis-point cut in September is likely, but a 50-basis-point move would require a significant deterioration in labor market data or a sharp spike in inflation.

Investors should also consider the broader implications of a 50-basis-point cut. A large rate reduction could fuel asset bubbles in equities and real estate, particularly if inflation expectations become unanchored. The S&P 500's recent flirtation with record highs, despite weak labor data, underscores the market's appetite for risk—a trend that could reverse if the Fed signals a more hawkish stance.

The Path Forward

The Fed's September meeting will be a critical test of its resolve. If the central bank sticks to its 25-basis-point plan, it will signal that it remains focused on long-term price stability rather than short-term political gains. Conversely, a 50-basis-point cut would validate market speculation and potentially undermine the Fed's credibility.

In the meantime, investors should focus on sectors that benefit from a measured policy environment. Defensive plays, such as utilities and consumer staples, may outperform in a low-growth, low-inflation scenario. Conversely, cyclical sectors like industrials and financials could face headwinds if the Fed delays further easing.

The disconnect between political pressure and market realism is a recurring theme in central banking. As the Fed navigates this tension, its commitment to data-driven policymaking will ultimately determine the trajectory of the economy—and the returns for investors.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet