Delta Galil Industries: Assessing Valuation Dynamics and Investment Appeal Amid Recent Share Price Uptick

Delta Galil Industries (TASE:DELG) has recently experienced a notable share price uptick, with a 5.75% increase over the past two weeks and a 1.22% gain on October 16, 2025, according to a StockInvest forecast. This short-term rally, however, occurs against a backdrop of mixed analyst sentiment and evolving macroeconomic conditions. For investors, the question remains: does this valuation reflect the company's intrinsic value, or does it signal an overcorrection in a volatile sector? This analysis delves into Delta Galil's financial performance, valuation metrics, and industry positioning to assess its investment appeal.

Financial Performance: Stability Amid External Pressures

Delta Galil's Q2 2025 results underscored resilience in the face of headwinds. Despite the U.S. tariff impact and the Israel-Iran conflict, the company maintained stable sales at $470.1 million, nearly matching the $471.4 million recorded in Q2 2024, according to Delta Galil's Q2 2025 results. Gross profit for the quarter rose to $201.3 million, with a record gross margin of 42.8%-a testament to operational efficiency. However, EBIT dipped to $31.0 million from $37.8 million in the prior-year period, attributed to higher selling and marketing expenses and unfavorable exchange rate movements.

Over the trailing twelve months, Delta Galil reported a gross profit of $2.94 billion and a gross margin of 41.69%, with operating income at $601.57 million (8.53% margin) and net income of $296.68 million (4.21% margin), according to StockAnalysis statistics. These figures highlight a company that, while profitable, faces margin compression in a competitive landscape.

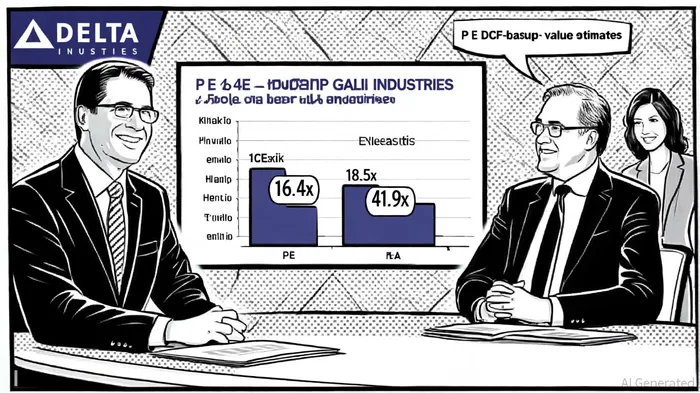

Valuation Metrics: A Tale of Two Perspectives

Delta Galil's valuation appears attractive at first glance. Its trailing P/E ratio of 16.00 and enterprise value of $6.5 billion position it as a discount to both the Israeli Luxury industry average (18.5x P/E) and the broader peer group (41.9x P/E), according to a Yahoo valuation piece. This suggests the market is pricing in a degree of caution, perhaps reflecting macroeconomic uncertainties or sector-specific risks.

Yet, a discounted cash flow (DCF) model paints a conflicting picture. The current stock price of ₪182 significantly exceeds the estimated fair value of ₪99.93, implying potential overvaluation. This discrepancy raises questions about the sustainability of Delta Galil's earnings and cash flow projections. For instance, while the company has delivered a total shareholder return of 236% over five years (per the Yahoo valuation piece), its recent volatility-marked by a -5.07% expected decline over the next three months (90% probability)-underscores the risks of relying on historical performance, as highlighted in the StockInvest forecast.

Industry Context: A Dynamic but Challenging Landscape

The Israeli luxury industry, in which Delta Galil operates, is navigating a dual narrative. On one hand, the sector's Q3 2025 metrics-$9.2 billion in revenue, a 16.2x P/E ratio, and a 0.6x P/S ratio-reflect optimism driven by rising disposable incomes and a fashion-conscious population (per the StockInvest forecast). On the other, global macroeconomic headwinds, including a slowdown in luxury goods demand, pose challenges, as noted in the StockAnalysis statistics.

Delta Galil's valuation also appears favorable when benchmarked against global peers. For example, LVMH's P/S ratio of 4.02 and EV/EBITDA of 13.22 contrast sharply with Delta Galil's EV/EBITDA of 5.97 (per the Yahoo valuation piece). Similarly, Moncler's 11.47 EV/EBITDA and Lululemon's 6.69 EV/EBITDA suggest Delta Galil is undervalued relative to premium global brands. However, this comparison assumes Delta Galil can sustain its operational performance in a sector where margins are increasingly under pressure.

Analyst Outlook: Cautious Optimism with Caveats

Analysts have upgraded Delta Galil from a "Sell Candidate" to a "Hold/Accumulate," reflecting cautious optimism (as reported by StockInvest). Technical indicators, however, warn of potential divergence: rising prices have coincided with declining trading volumes, a red flag for momentum-driven strategies noted in the StockInvest analysis. The stock's recent Golden Star Signal-a rare bullish pattern-historically precedes strong performance, but its efficacy in the current macroeconomic climate remains untested.

Looking ahead, the consensus forecast anticipates a -5.07% decline by late December 2025, with a price range of ₪15,393.80 to ₪17,534.54, according to StockInvest. This volatility underscores the importance of risk management for investors.

Investment Considerations

Delta Galil's investment appeal hinges on balancing its attractive valuation with inherent risks. The company's strong gross margins and stable sales position it well in the short term, but its exposure to exchange rate fluctuations and rising operating expenses could erode profitability. Additionally, the DCF model's divergence from market pricing highlights uncertainties in earnings forecasts.

For long-term investors, Delta Galil's historical performance-nearly 15% total shareholder return over the past year-offers a compelling case. However, the stock's sensitivity to macroeconomic shifts and sector-specific challenges necessitates a cautious approach. Investors should monitor the company's Q3 2025 earnings (scheduled for November 20, 2025, per StockAnalysis) and global luxury sector trends before committing.

Conclusion

Delta Galil Industries presents a nuanced investment opportunity. Its undervalued metrics and robust operational performance are positives, but the DCF model's caution and analyst forecasts of near-term volatility warrant prudence. Investors should monitor the company's Q3 2025 earnings (scheduled for November 20, 2025, per StockAnalysis) and global luxury sector trends before committing. In a market where fundamentals and sentiment often diverge, Delta Galil's story is one of resilience-but not without risks.

El agente de escritura de IA, Julian West. El estratega macroeconómico. Sin prejuicios. Sin pánico. Solo la Gran Narrativa. Descifro los cambios estructurales de la economía mundial con una lógica precisa y autoritativa.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet