Decoding Treasury Yields as a Fed Rate Cut Predictor

The U.S. Treasury market has long been a barometer for Federal Reserve policy expectations. Historically, the 10-year Treasury yield has mirrored the Fed's rate-cutting trajectory with uncanny precision. Yet in 2024, this relationship fractured. While the Fed slashed rates aggressively—cutting 100 basis points by year-end—Treasury yields surged by over 100 basis points. This divergence raises critical questions: Can bond markets still reliably signal Fed policy shifts? And how should investors navigate the risks and opportunities in this new environment?

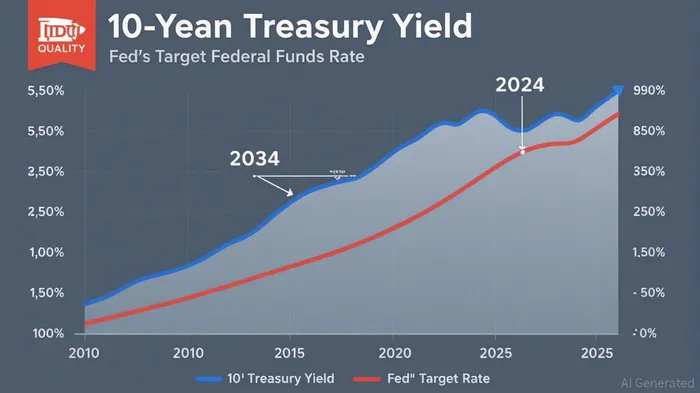

Historical Correlations and the 2024 Anomaly

For decades, Treasury yields and Fed policy have moved in lockstep. In seven prior rate-cutting cycles since the 1980s, the 10-year yield was lower 100% of the time 100 days after the first rate cut. For example, in the 2007 cycle, yields fell 27.5 basis points by day 100. But 2024 defied this pattern. By December 2024, the 10-year yield had risen to 4.429%, despite a 50-basis-point rate cut in September.

The anomaly stems from two forces: stronger-than-expected economic growth and heightened macroeconomic uncertainty. The U.S. economy outperformed forecasts, with growth revisions pushing expectations from 1.2% to 2.7% by year-end. This reduced market expectations for future rate cuts, pushing yields higher. Simultaneously, uncertainty over the Fed's policy path—evidenced by a 150-basis-point spread in FOMC members' rate projections—and geopolitical risks (e.g., Trump-era trade policies) amplified volatility.

Why Bond Market Signals Are Failing to Predict Fed Moves

The bond market's role as a policy oracleORCL-- has dimmed in recent years. During the 2020 pandemic, the market underestimated the Fed's urgency to cut rates. In 2022, it overestimated the pace of tightening. By 2024, the market had priced in 150 basis points of cuts but revised expectations to 70 basis points by April 2025 as growth data held up.

The term premium—the extra yield investors demand for holding long-term bonds—has spiked to a decade high, reflecting this uncertainty. This premium now accounts for 30% of the 10-year yield, up from 15% in 2020. The market is no longer just pricing in inflation or growth but also hedging against policy ambiguity and fiscal risks (e.g., U.S. debt dynamics).

****

Investor Strategies: Balancing Yield, Duration, and Risk

The 2024 environment demands a nuanced approach. Here's how investors can adapt:

Leverage Higher Starting Yields

With the Bloomberg U.S. Aggregate Bond Index yielding 4.7% in Q2 2025, investors are being compensated for rate risk. Historical data shows that 88% of the index's five-year returns are explained by starting yields. For example, a 50-basis-point rate cut could boost 10-year Treasury returns by 8.0%, versus a 0.6% gain if rates rise.Manage Duration Exposure

While longer-duration bonds benefit from falling rates, they carry downside risk if rates continue to rise. Short-duration instruments like the iShares 0-3 Month Treasury Bond ETF (SGOV) or the iShares 0-5 Year TIPS BondSTIP-- ETF (STIP) offer yield with less volatility.Diversify Beyond Treasuries

High-yield corporate bonds and municipal bonds (munis) provide income and diversification. The Bloomberg U.S. High Yield Composite returned 3.5% in Q2 2025, outperforming the Agg Index. For tax-advantaged income, munis now yield 6.79% (investment-grade) and 9.86% (high-yield), with tax-equivalent yields at multi-decade highs.Hedge Against Policy Uncertainty

Active strategies, such as the iShares Flexible Income Active ETF (BINC), target non-traditional sectors like European credit and securitized products. These strategies exploit relative value amid divergent global policy cycles (e.g., U.S. rate cuts vs. European tightening).

Risks and Opportunities in the New Normal

The bond market's predictive power is no longer binary. While yields remain a useful guide, investors must account for three additional factors:

- Fiscal Policy: The U.S. deficit is projected to grow, increasing pressure on Treasury yields.

- Geopolitical Risks: Trade tensions and currency shifts (e.g., the dollar's weakening in early 2025) could disrupt capital flows.

- Policy Lag: The Fed's dual mandate (inflation and employment) often leads to delayed responses to economic data.

For example, the Fed's 2024 rate cuts were delayed despite inflation easing, as policymakers prioritized employment data. This lag means bond markets may overreact to short-term data, creating opportunities for contrarian investors.

Conclusion: A Strategic, Adaptive Approach

Treasury yields remain a vital tool for forecasting Fed policy, but their reliability has evolved. In 2025, investors should treat bond signals as part of a broader analytical framework, not definitive forecasts. A diversified portfolio with a mix of short-duration bonds, active strategies, and high-yield credits can navigate the uncertainties of a shifting rate environment.

As the Fed edges toward a neutral stance, the key will be flexibility. The bond market's current pricing—75-100 basis points of 2025 rate cuts—may yet shift. But with starting yields at multi-decade highs and asymmetric return potential, the fixed-income landscape offers a compelling case for income-focused investors willing to navigate the noise.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet