Decoding July 2025 Core PCE: Sector Opportunities in a Polarized Inflationary Climate

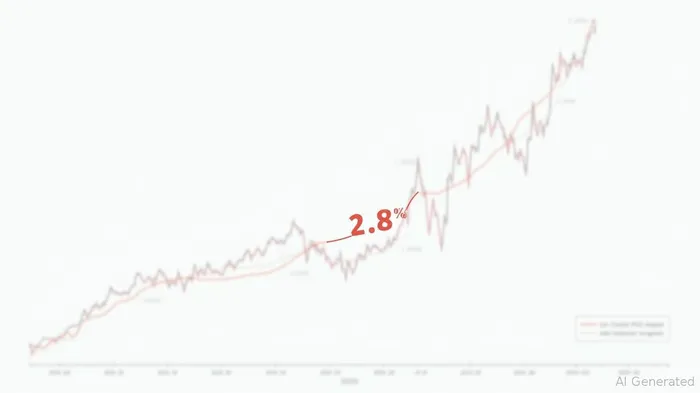

The July 2025 U.S. Core PCE Price Index release—a 0.3% monthly gain and 2.8% annual rise—reveals a nuanced inflationary landscape. While the data aligns with the Federal Reserve's long-term averages, it underscores a divergent inflationary pattern: tariffs are driving goods prices upward, while financial market dynamics are amplifying service-sector inflation. For investors, this polarization demands a granular, sector-specific approach to capitalize on winners and hedge against losers.

Tariffs and Manufacturing: A Tale of Two Industries

Import tariffs on furniture, automobiles, and other goods have created a wedge between input costs and profit margins. The furniture sector, for instance, faces a 4.2% year-over-year price surge, driven by tariffs and supply chain bottlenecks. Companies like Ashley Furniture (AFH) and Ethan Allen (ETHN) are passing costs to consumers, but their ability to sustain margins hinges on demand resilience.

Conversely, sectors benefiting from tariff-induced domestic production—such as industrial metals and logistics—present compelling opportunities. The Invesco Steel ETF (SLX), for example, could gain traction as manufacturers shift production to avoid tariffs. would provide insight into this dynamic.

Financial Market Rebounds: Asset Managers as Inflation Winners

The rebound in equity markets has elevated portfolio management fees, a key component of the PCE index. Asset managers like BlackRock (BLK) and Vanguard (VGT) are poised to see revenue growth as assets under management expand. This trend highlights a critical nuance: while traditional inflation metrics focus on goods, services tied to financial activity are now a significant driver. Investors should monitor BlackRock's quarterly fee revenue to gauge this tailwind.

Energy and Utilities: A Volatile Undercurrent

Energy and utilities remain exposed to regulatory shifts and oil price volatility. The sector's underperformance in a "higher for longer" rate environment is compounded by inflationary pressures on capital-intensive projects. For now, underweighting these sectors is prudent unless Q3 sees a clear policy pivot or commodity rebound.

Strategic ETFs and Hedging Tools

To navigate this polarized climate, investors should consider:

- iShares U.S. Home Construction ETF (ITB): Benefiting from inflation-linked demand for housing.

- Invesco Steel ETF (SLX): Capitalizing on domestic manufacturing shifts.

- Treasury Inflation-Protected Securities (TIPS): A hedge against persistent inflation.

could highlight its inflation resilience.

The Fed's Dilemma: Policy Caution Amid Divergent Pressures

The Fed's cautious stance—hinting at a September rate cut contingent on transitory pressures—suggests a "higher for longer" environment. This favors cash-generative industries (e.g., industrials) over high-yield sectors like real estate. Investors should watch Federal Reserve policy statements and sector-level PCE data for mid-2025 adjustments.

Conclusion: Precision Over Broad Bets

The July 2025 Core PCE data signals a departure from one-size-fits-all inflation narratives. Tariff-driven goods inflation and financial-sector service inflation require distinct strategies. By overweighting inflation-resistant sectors like asset management and domestic manufacturing, and hedging against energy and discretionary underperformance, investors can navigate this polarized environment with precision. The key to outperforming lies in data-driven sector rotation, not macroeconomic guesswork.

would further illuminate this divergence.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet