Decoding the December 2025 Jobs Report: Implications for Equity and Bond Markets

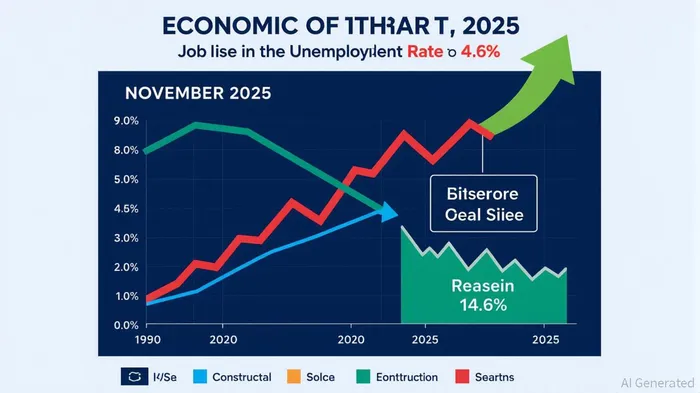

The December 2025 U.S. jobs report, effectively a proxy for November 2025 data, has delivered a mixed signal for investors. While nonfarm payrolls rose by 64,000 jobs-surpassing expectations of 45,000-the unemployment rate climbed to 4.6%,

marking a four-year high and underscoring fragility in the labor market. This duality of job growth and rising unemployment reflects a complex interplay of sectoral shifts, policy disruptions, and evolving Federal Reserve (Fed) dynamics. For asset allocators, the report demands a nuanced approach to macroeconomic signal timing, balancing optimism about resilient employment with caution over inflationary pressures and central bank policy pivots.

Labor Market Trends: Sectoral Shifts and Structural Headwinds

The November jobs report highlights divergent trends across sectors. Health care and construction added significant jobs, while federal government employment continued its steep decline,

losing 6,000 positions in November and 162,000 in October-a direct consequence of deferred resignations and a government shutdown. These disruptions not only distorted the October data but also

delayed the November report, complicating real-time market interpretation. Over the past 12 months, total nonfarm payrolls have shown minimal net change since April 2025,

suggesting a labor market in a state of "low hiring and low firing".

Average hourly earnings rose by 0.1% in November,

Average hourly earnings rose by 0.1% in November,

below the 0.3% forecast, signaling subdued wage inflation. This trend aligns with broader economic conditions where stringent immigration policies under President Donald Trump have

constrained labor supply, creating a mismatch between job availability and workforce participation. For equities, sectors like health care and construction may benefit from sustained demand, but investors must weigh these gains against the risk of prolonged wage stagnation, which could dampen consumer spending-a critical driver of U.S. economic growth.

Fed Policy and Market Dynamics: Navigating Rate Cuts and Inflation

The Fed's recent 25-basis-point rate cut,

bringing the federal funds rate to 3.50-3.75%, reflects its cautious stance amid these labor market uncertainties. While the central bank remains focused on inflation control,

the rising unemployment rate and weak wage growth have intensified calls for further rate reductions in 2026. Analysts project that the Fed will prioritize employment support over aggressive inflation suppression,

particularly as long-term growth projections remain modest.

Bond markets have already priced in this dovish outlook, with Treasury yields edging lower in anticipation of rate cuts. However, the upcoming release of the November Consumer Price Index (CPI) will be critical in determining whether inflationary pressures from tariffs and supply chain bottlenecks

force the Fed to delay further easing. For now, the 10-year Treasury yield has

stabilized near 3.8%, reflecting a delicate balance between rate-cut expectations and inflation risks.

Equity and Bond Allocation Strategies: Sector Rotation and Duration Management

The November jobs report suggests a strategic shift in asset allocation. Equities in sectors sensitive to lower interest rates-such as real estate, utilities, and healthcare-may outperform as rate cuts reduce borrowing costs and boost valuations

according to Reuters. Conversely, sectors reliant on consumer spending, like retail and hospitality, could face headwinds if wage growth remains stagnant

according to CNBC. Investors should also monitor the Fed's communication for clues about the pace of rate cuts, as prolonged uncertainty could exacerbate market volatility.

For bond investors, the key lies in duration management. Short- and intermediate-term bonds are likely to outperform in a rate-cutting environment, while long-duration assets face inflation risks. Treasury Inflation-Protected Securities (TIPS) could serve as a hedge against unexpected inflation,

particularly if the November CPI report reveals persistent price pressures.

Conclusion: A Call for Adaptive Allocation

The December 2025 jobs report underscores the importance of adaptive asset allocation in a macroeconomic landscape defined by mixed signals. While job growth in key sectors offers a floor for equity markets, rising unemployment and weak wage inflation necessitate a cautious approach to duration and sector exposure. Investors should prioritize flexibility, leveraging tactical rotations and hedging strategies to navigate the Fed's evolving policy path. As the December CPI data and subsequent Fed meetings unfold, the ability to decode macroeconomic signals will remain paramount for optimizing returns in both equity and bond markets.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet