Decoding the U.S. 4-Week Treasury Bill Auction: Yield Shifts and Sector Rotation in a Changing Policy Landscape

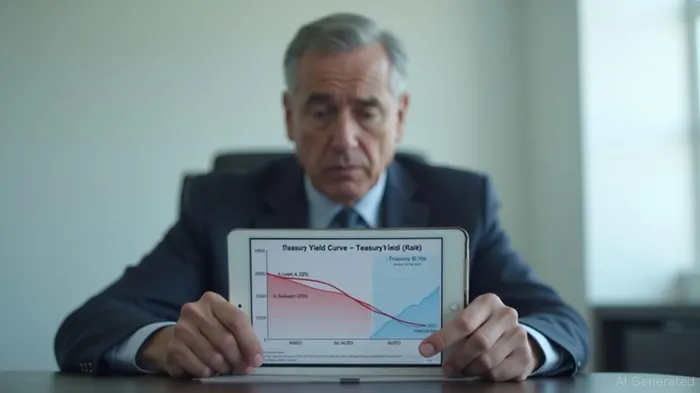

The U.S. 4-week Treasury Bill (T-Bill) auction has long served as a barometer for short-term interest rate expectations and a proxy for the Federal Reserve's monetary policy stance. As of August 20, 2025, the 4-week T-Bill yield stands at 4.33%, a marginal decline of 0.01 percentage points from the prior session but a 0.03-point increase over the past month. This subtle movement, however, masks a broader narrative: the yield remains 0.97 percentage points below its January 2024 peak of 6.13%, signaling a structural shift in market expectations for accommodative policy. For investors, understanding these dynamics is critical to navigating sector rotation strategies in an environment where central bank actions increasingly dictate capital flows.

Short-Term Yields as a Policy Signal

The 4-week T-Bill yield, positioned at the front end of the Treasury curve, is closely tied to the Federal Funds rate and reflects immediate liquidity conditions. The current yield of 4.33%—while elevated compared to the long-term average of 1.58%—is a far cry from the 6.13% highs seen in early 2024. This decline, despite a backdrop of persistent inflation, suggests that markets are pricing in a Fed pivot toward easing. Analysts project the yield to fall further to 4.27% by August 2026, aligning with expectations of rate cuts in the second half of 2025 and early 2026.

The Treasury's shift to a monotone convex spline methodology for yield curve calculations in December 2021 has also refined the accuracy of these signals. By smoothing out distortions in historical data, the updated methodology ensures that yield movements are more reflective of true market sentiment. For instance, the 0.97-point annual decline in the 4-week yield underscores a growing conviction that the Fed will prioritize growth over inflation in the near term—a stark contrast to the hawkish stance of 2023-2024.

Sector Rotation in a Lower-Yield Environment

As short-term rates trend downward, investors must recalibrate their sector allocations. Historically, falling Treasury yields have favored growth-oriented sectors such as technology and consumer discretionary, which thrive in low-cost borrowing environments. Conversely, financials—particularly banks—tend to underperform when yields contract, as net interest margins compress.

The current trajectory of the 4-week T-Bill yield suggests a potential rotation into sectors that benefit from accommodative monetary policy. For example, tech stocks, which have underperformed in the high-rate environment of 2024, could see renewed demand as discount rates decline. Similarly, utilities and real estate investment trusts (REITs) may gain traction, as lower yields reduce the opportunity cost of holding income-generating assets.

However, the path is not without risks. A premature Fed pivot could lead to a surge in inflation expectations, causing yields to rebound and triggering a sell-off in growth sectors. Investors should monitor the 4-week yield in conjunction with inflation data and Fed communication to time their rotations effectively.

Strategic Implications for Portfolio Managers

For active managers, the 4-week T-Bill yield offers a dual role: as a liquidity benchmark and a policy signal. Here are three actionable insights:

- Hedge Against Policy Uncertainty: Given the projected decline in short-term rates, consider overweighting sectors with high sensitivity to rate cuts (e.g., industrials, materials) while underweighting those vulnerable to rate hikes (e.g., financials).

- Leverage Duration Mismatches: The 4-week T-Bill's low duration makes it an ideal tool for managing portfolio liquidity. Pairing it with longer-dated Treasuries can create a yield curve strategy that benefits from steepening or flattening trends.

- Monitor Auction Dynamics: The Treasury's August 2025 auction results—once released—will provide granular data on demand for short-term debt. A surge in noncompetitive bids (which are capped at $5 million) could indicate heightened investor appetite for risk-free assets, signaling a potential shift in risk appetite.

Conclusion: Navigating the New Normal

The U.S. 4-week Treasury Bill auction is more than a routine government financing tool—it is a window into the evolving interplay between monetary policy and market sentiment. As yields trend lower, investors must adapt their strategies to capitalize on the shifting landscape. By aligning sector allocations with the trajectory of short-term rates and maintaining a close watch on Treasury auction dynamics, portfolios can position themselves to thrive in a world where policy signals reign supreme.

For now, the 4.33% yield serves as a cautionary note: while easing is on the horizon, the path to normalization remains fraught with volatility. Investors who act with discipline and foresight will be best positioned to navigate the twists and turns ahead.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet