The Decline in U.S. Job Openings as a Leading Indicator of a Slowing Economy

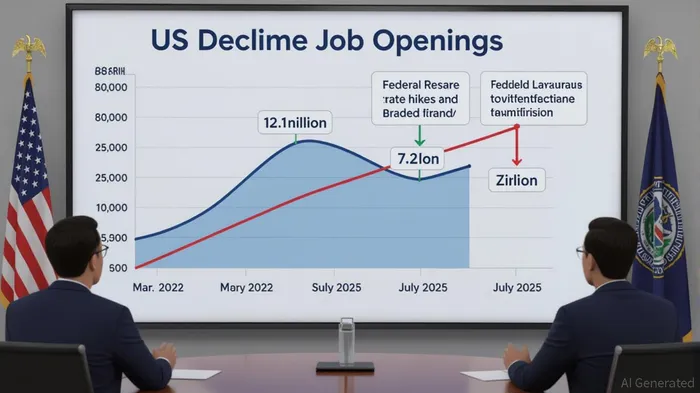

The U.S. labor market has entered a phase of cautious recalibration. As of July 2025, job openings stood at 7.2 million, a marginal decline from June's 7.4 million and a stark contrast to the 12.1 million peak in March 2022. This cooling trend, driven by 11 Federal Reserve rate hikes and lingering trade policy uncertainties, signals a broader economic slowdown. For investors, the implications are clear: sectors reliant on consumer demand are increasingly exposed to headwinds that could erode growth and profitability.

Labor Market Cooling and Consumer Demand

Job openings are a critical barometer of economic health. When employers reduce hiring, it often reflects diminished confidence in future demand. The July JOLTS data reveals a labor market that is neither contracting nor booming but rather stabilizing at a lower equilibrium. This shift is particularly concerning for industries where consumer spending is the lifeblood of growth.

Consider the healthcare and social assistance sector, which saw a 181,000 drop in job openings. While healthcare remains a labor-intensive field, the decline suggests a moderation in demand for services like home health care and long-term care facilities. Similarly, the arts, entertainment, and recreation sector—highly sensitive to discretionary spending—lost 62,000 openings. These sectors are not just losing jobs; they are losing momentum in a consumer-driven economy.

Sector-Specific Risks

The interplay between job openings and consumer demand is most evident in the retail and hospitality industries. With fewer Americans securing new jobs, wage growth has plateaued, and household budgets are tightening. This dynamic directly impacts companies like AmazonAMZN--, which reported layoffs in July 2025, and hotel chains such as MarriottMAR--, which rely on leisure travel.

The technology sector, while still buoyed by stock market optimism, faces a paradox. Firms like MetaMETA-- and AppleAAPL-- continue to innovate, but their labor market fundamentals are deteriorating. The 197,000 increase in quits in professional and business services highlights worker mobility, yet this does not offset the 130,000 drop in construction and logistics job openings. For investors, the disconnect between stock prices and labor data is a warning sign.

Strategic Reallocation for Investors

The Federal Reserve's rate hikes have created a dual challenge: higher borrowing costs for businesses and reduced purchasing power for consumers. Sectors like financials and industrials may benefit from rate cuts, but consumer discretionary and retail face a prolonged period of adjustment.

Investors should prioritize sectors with structural demand, such as healthcare and utilities, while hedging against overexposed areas. For example, companies in the S&P 500's Consumer Staples Index have shown resilience amid economic uncertainty, whereas the Consumer Discretionary Index has underperformed.

Conclusion

The decline in U.S. job openings is not merely a statistical anomaly—it is a leading indicator of a labor market that is adapting to a new economic reality. As employers tighten hiring and workers remain cautious about quitting, the ripple effects will be felt most acutely in sectors tied to discretionary spending. For investors, the path forward lies in rebalancing portfolios toward defensive sectors and avoiding overleveraged consumer-facing businesses. The labor market's cooling trend is a signal, not a crisis, but one that demands strategic foresight.

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet