Will December Deliver a Year-End Lift or Continue the Turbulence?

After a November defined by stomach-churning volatility and a Thanksgiving week rebound, investors are turning the calendar page with a mix of exhaustion and anticipation. The S&P 500 hovers near 6,800, having clawed back from mid-month lows, but the path to a record-breaking year-end close is paved with critical tests.

As CNBC recently asked, "Will December bring joy to round off the year?" The answer likely lies in a trifecta of catalysts: the Federal Reserve's final decision of 2025, the resilience of the AI trade, and the technical setup of a market where many investors are surprisingly under-positioned.

The Macro Pivot: All Eyes on December 9-10

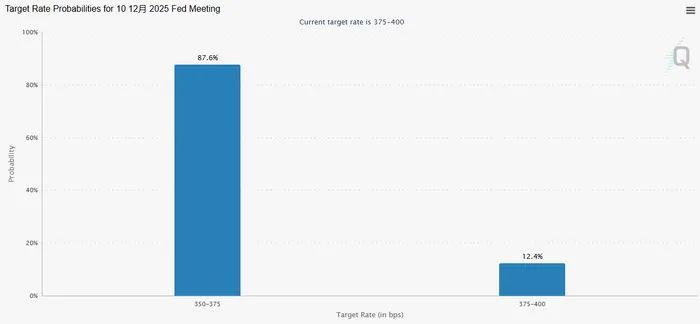

The immediate focus for the market is the Federal Open Market Committee (FOMC) meeting scheduled for December 9-10. Following favorable PCE inflation data released late last week—showing headline inflation moderating to 2.4%—futures markets are now pricing in an 85-90% chance of a rate cut.

However, the "Fed pivot" narrative is not without risk. While the market expects a cut, the real volatility driver will be Chair Jerome Powell's tone regarding 2026. Is this a "mid-cycle adjustment" to protect the labor market, or the beginning of an aggressive easing cycle?

The Bureau of Labor Statistics (BLS) has announced the postponement of the November Jobs Report, originally slated for this Friday, December 5.

Citing administrative delays, the release has been pushed to mid-month (tentatively expected post-FOMC). This is not just a calendar tweak; it is a macro-economic shock. For weeks, the "Goldilocks" narrative depended on this Friday's data showing cooling but resilient hiring. Now, that data point has vanished from the immediate horizon.

The AI Dilemma: Bubble or Bargain?

November's volatility was exacerbated by renewed jitters over AI valuations. Tech giants like Nvidia and Microsoft faced scrutiny as investors questioned the ROI of massive capex spending. Yet, as we enter December, the narrative is shifting back to growth.

Analysts at Bank of America recently noted that top-tier semiconductor stocks "have more room to run," citing strong demand visibility into 2026. The dip in November is being viewed by institutional bulls not as a bursting bubble, but as a necessary valuation reset. For the Santa Rally to materialize, the "Magnificent Seven" must stabilize. If Nvidia can reclaim its momentum early in the month, it often acts as a rising tide for the broader S&P 500.

Positioning: The "Pain Trade" is Higher

One of the most compelling arguments for a December rally is counter-intuitive: investors might not own enough stock.

As noted in a recent market memo, "December will begin with investors owning little stock," suggesting that institutional positioning is lighter than usual for this time of year. Many funds de-risked heavily during the November drawdown. If the market breaks resistance at 6,850, we could see a "chase" dynamic where under-allocated managers are forced to buy into the rally to salvage their year-end performance metrics.

This aligns with the historical Santa Claus Rally phenomenon. Seasonality data shows that December is traditionally one of the strongest months for equities, particularly in the second half. However, the gains often come after a tax-loss harvesting flush in the first week.

The Verdict

December 2025 is set up to be a binary month. If the Fed cuts rates and signals a soft landing, combined with light investor positioning, the S&P 500 could easily challenge the 7,000 level. However, if inflation data surprises to the upside or the Fed strikes a hawkish tone, the "Santa Rally" could be cancelled.

For now, the trend favors the bulls, but as November taught us, the market takes the stairs up and the elevator down. Buckle up.

Tianhao Xu is currently a financial content editor, focusing on fintech and market analysis. Previously, he worked as a full-time forex trader for several years, specializing in global currency trading and risk management. He holds a master’s degree in Financial Analysis.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

Comments

No comments yet