December CPI Reinforces a Choppy Downtrend in 2026 Inflation

Key Takeaways

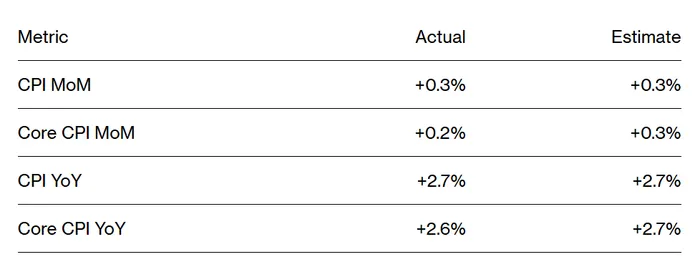

Headline CPI met expectations, while core CPI came in softer than forecast.

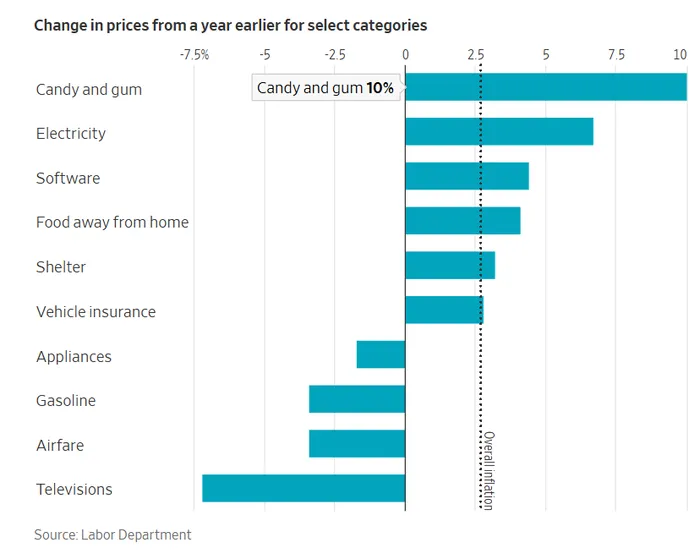

Energy-intensive services pushed some prices higher, while travel-related costs fell sharply.

Rent inflation slowed to its lowest pace since 2021.

Real wage growth remained positive, extending a two-and-a-half-year trend.

The Fed is unlikely to cut rates in January, with inflation expected to trend lower but remain volatile this year.

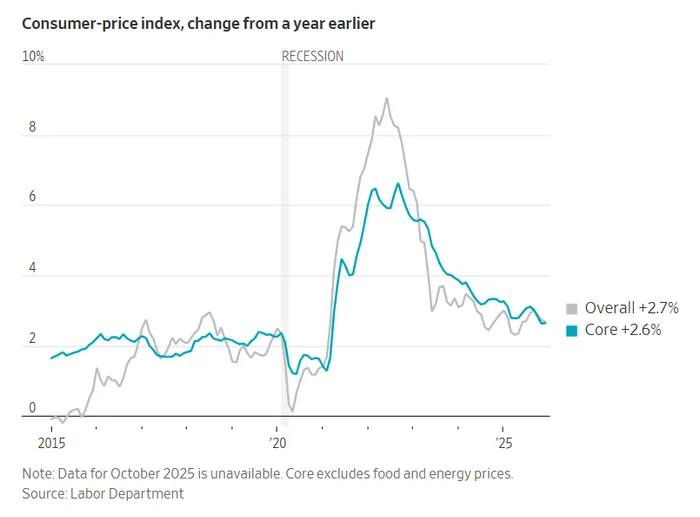

U.S. December CPI rose 2.7% year over year, in line with expectations. Core CPI, which excludes food and energy, increased 2.6% year over year, below the consensus forecast of 2.7%.

Looking at the components, candy prices surged sharply, while electricity prices jumped due to the high energy consumption of data centers. In contrast, gasoline, airfares, and other travel-related costs fell significantly.

New vehicle prices edged up 0.3% year over year and were flat on a month-over-month basis. Markets had previously expected automakers to raise prices on new models launched at the start of the year, but this did not materialize.

Housing rents increased 2.9% year over year, marking the smallest gain since October 2021. Prices for recreational services rose 1.2% month over month, while household insurance costs increased 1%, making them the main drivers of services inflation.

After adjusting for inflation, real average hourly earnings in the U.S. rose 1.1% year over year in December. Wage growth has exceeded price growth for the past two and a half years.

No January Rate Cut, Inflation Likely to Drift Lower in 2025

Following the CPI release, Wall Street analysts broadly agreed that the data would not prompt the Federal Reserve to cut rates in January. The coming days will feature a heavy schedule of FOMC officials’ public remarks, which warrant close attention.

Ian Lyngen of BMO said inflation has become a secondary concern, with the Fed now more focused on labor market conditions. He noted that the data were in line with expectations and would not alter the Fed’s decision to remain on hold in January.

ClearBridge Investments’ Head of Economic and Market Strategy, Jeff Schulze, commented that markets welcomed the December CPI as further evidence inflation is moving back toward the 2% target. However, he cautioned that uncertainty remains as companies may adjust prices at the start of the new year. Schulze added that the data are supportive for risk assets and increase the probability of the Fed delivering more aggressive-than-expected rate cuts in 2026.

Bloomberg’s U.S. economics team noted that many tariff-affected goods have seen price declines, with tariff pass-through peaking in October. They expect the Fed to cut rates by 100 basis points this year.

RSM Chief Economist Joseph Brusuelas said inflation in January and February remains a key focus, as many companies reset prices early in the year. He expects inflation to trend lower overall but with intermittent setbacks. Brusuelas also warned that Trump’s “One Big Beautiful Bill” (OBBB), which includes substantial tax cuts, along with continued heavy corporate investment in AI, could put upward pressure on inflation.

Finally, it is worth noting that the Trump administration has recently launched a criminal investigation into Fed Chair Jerome Powell. This could encourage FOMC officials to delay rate cuts, as markets may interpret easing as political capitulation, potentially undermining the Fed’s independence.

Senior Research Analyst at Ainvest, formerly with Tiger Brokers for two years. Over 10 years of U.S. stock trading experience and 8 years in Futures and Forex. Graduate of University of South Wales.

Latest Articles

Stay ahead of the market.

Get curated U.S. market news, insights and key dates delivered to your inbox.

AInvest

PRO

AInvest

PRO

Comments

No comments yet